Canadian Undervalued Stocks 2026

Undervalued stocks in Canada are usually identified as having a market value that is for one reason or another below their “true value.” The idea is that if you as an investor are able to identify these undervalued stocks while their purchase price is still low, then, someday in the future, when the rest of the world catches on, you’ll make money as you watch the share price rise.

It’s basically a how-to for “buy low, sell high.”

Of course it’s easier said than done. If stocks are undervalued and their purchase price is low, there is almost always a reason behind that. You might disagree with that reason (hence you placing a higher value on the company) but you’ll notice that in undervalued list below there are some “beat up” valuations due to the media focusing on a particular angle.

With the Canadian stock market having a monster 2025 (up 32% if you include dividends!) and now treading water in 2026, it is getting harder and harder to find undervalued Canadian stocks. That said, I’m not sure US tech or international stocks that are fresh off a monster year of their own are great places to look either.

We had to remove several of our 2025 undervalued stocks list like Barrick Gold and Cenovus because they had simply had went up too much over the past year. (Great news for people that took our advice, but they just don’t belong on the current undervalued list any longer.)

Key metrics and catalysts are given for each of my top undervalued stock picks below. (Figures are approximate; P/E and yields from latest reports.)

All of the info suggested here is based on Dividend Stocks Rock advanced tools and analysis. Check out our full Dividend Stocks Rock review for more information.

5 Best Canadian Undervalued Stocks

When looking for the best undervalued stocks, you’re looking for established companies with a long history. Ideally, they are companies with steady year-over-year growth, as well as decent dividend payouts. In Canada, banks and oil and energy stocks do just that, which is why they are our top picks for undervalued stocks.

TELUS Corporation (TSX: T)

Telus is the wireless/internet provider with a fast-growing health-tech arm. Telus currently trades about 20% lower than its intrinsic value according to Canadian stock analyst Mike Heroux. While the company has to focus on paying down its sizable debt from capex spending, it has more than 18 million customers across the country!

At about $17, Telus’ dividend yields nearly 10%. It recently endured price war noise and high capex, but those factors should ease over time. Growth in Telus Health services and 5G expansion, plus any future spectrum windfall, could boost margins. For income investors, its high yield and stable legacy service base provide a cushion as multiples re-rate.

Yes, debt and interest rates are valid concerns. But Telus (and the other three Canadian telecom giants) appear to have some interesting strategies for unlocking asset value and paying down debt sooner rather than later.

So far, while there is nervousness about the fact that Telus is paying out more than 100% of free cash flow, there is also pretty compelling evidence that the dividend could continue to be paid at current levels (although certainly only minor – if any – dividend raises). Personally I think criticisms of this company are so baked in at this point, that the pendulum has swung too far!

Rogers (TSX: RCI.B)

Rogers is another Canadian telecom giant that keeps showing up on undervalued stock screens right now. While Telus tends to get more attention from dividend investors, Rogers may actually be the cleaner value play at the moment. The company still looks to be trading at a meaningful discount to fair value, and unlike some of its peers, its dividend appears to be on much firmer footing due to a more conservative dividend payout policy.

This is also not some speculative turnaround story. Rogers has more than 12 million wireless subscribers and millions of internet customers across Canada, giving it one of the largest communications platforms in the country. That customer base gives the company a very solid recurring revenue stream, even if the overall telecom environment remains highly competitive. The Shaw acquisition continues to generate more revenue, and increased cost-cutting over the long-term will likely prove to be a winner for Rogers.

With capital spending expected to ease somewhat after the heavy network investment of the last few years, there is a reasonable case that Rogers will have more room to strengthen its balance sheet and gradually improve investor sentiment. Rogers’ ownership of professional sports teams continues to look like a good idea as that sector skyrockets in value every time a new team goes on the auction block. The 5-yr earnings-per-share growth of 32% is nothing to shake a stick at!

Like Telus, debt is still the big concern here. Rogers took on a lot of leverage building out its network and acquiring Shaw. But management has clearly been focused on deleveraging, and there are a few possible avenues to unlock asset value over time as well.

Personally, I think the market has become so negative on Canadian telecom stocks in general that Rogers now looks like one of the more interesting contrarian picks in the country. If competition settles down even a little, and free cash flow keeps improving, there is a pretty solid case that the stock has been pushed too far to the downside.

Thomson Reuters (TSX: TRI)

It has been a long time since TRI was on any undervalued stocks list, which is part of what makes it interesting right now. It’s not every day that you see a company with a pretty big investment moat that is down 50% over the last 12 months!

This is a high-quality business built around legal, tax, accounting, compliance, plus media software and information services. In other words, it is not some cyclical stock that only looks cheap because commodity prices fell for a few months. It is a very durable business that appears to have been dragged down by broader concerns about growth and AI disruption.

What I like here is that the core business still looks very solid. Thomson Reuters generates a large amount of recurring revenue, has a long history of dividend growth, and serves professional customers who are not exactly eager to rip out mission-critical tools just to save a few bucks. That sort of customer stickiness matters a lot when markets get nervous and investors start throwing around catastrophic terms like “SAAS-pocalypse.”

The obvious concern is artificial intelligence. A lot of the recent negativity around the stock seems to come from the idea that AI could weaken parts of Thomson Reuters’ moat over time. That is something worth watching, but I think the market may be leaning a bit too hard into that fear. Thomson Reuters is not sitting on the sidelines here. It is investing in AI tools of its own and has the balance sheet and scale to adapt as the industry changes.

Personally, I think this looks like one of those classic cases where a very good company has gotten cheaper because investors are suddenly obsessed with what might go wrong five years from now. If those concerns prove even a little overblown, there is a very high chance the stock has been marked down too far.

Nutrien Ltd. (TSX: NTR)

Despite the fact it’s up over 30% over the last year, I still think Nutrien is significantly undervalued. Nutrien is the world’s largest fertilizer company (potash, nitrogen, phosphate). Nutrien’s earnings come from crop nutrients, a necessity for global food production. That basic truth is important at the moment, because we can’t get a lot of fertilizer out of the Middle East at the moment, and even the best case scenarios aren’t great in the short- and medium-terms.

If all the wars in the world were to suddenly end, the population quit growing, and temperatures quit going up – then Nutrien would be in trouble. Russian and Belarussian potash would enter the market in greater quantities, and we’d just need less fertilizer overall. I simply think there is a very low chance of all that happening when you look at the geopolitical climate right now!

The ag sector has been under pressure (soft commodity prices), depressing Nutrien’s stock. If farming profits and crop prices recover, Nutrien’s earnings and cash flow could surprise on the upside. In the meantime, a 3% dividend and potential merger synergies (cost-cutting) make this fertilizer leader a value play for long-term food demand. A P/E ratio of 16x is just too low for this stock relative to what other stocks are currently priced at.

Canadian National Railway (TSX: CNR)

CNR is Canada’s largest railroad, and perhaps the poster boy for Canadian Wide Moat Stocks. They’re quite clearly not building more railways anytime soon. The current P/E ratio of around 20x is significantly lower than the 30x that it hit back in 2021. Freight volumes have been choppy (dry bulk, energy), which helps explain the softness. General headlines of tariffs and recessions have tamped down expectations for both of the Canadian railways.

CN benefits from intercontinental trade, intermodal (ports to U.S. markets) and pricing power. Infrastructure spending (including rail) and rebounding commodities (oil, grain) should lift volumes and pricing. Over 5–10 years, CN’s unique network and growing ecommerce-related cargo are likely to drive earnings higher, closing the valuation gap.

That said, US tariffs are a big drag on Canada-US cross border trade, and depending what gets hammered out in the new CUSMA agreement this summer, the new reality could sting the share price in the short term.

Best Stocks to Buy for Under $1

Look – we get asked all the time about the best penny stocks in Canada or the best Canadian stocks to buy for under a dollar.

But the honest truth is that trying to figure out that volatile world is a nightmare. The metrics are incredibly difficult to project into the future and often the companies do not offer any long-term competitive advantage (unlike undervalued Canadian bank stocks or energy stocks).

Before you look at buying stocks under $1, I’d ask you to do a little reading on the risk levels associated with these companies. Personally, I don’t own any of these companies in my portfolio, so I wouldn’t be comfortable recommending them to others.

However, if you are still interested in cheap stocks, check out our thoughts on the Best Penny Stocks in Canada.

A third factor that I consider before adding to a position is the use of basic technical analysis, more specifically, using the long-term moving average.

How Do I Determine Canadian Undervalued Stocks?

Ok onto why you are here, how do I determine when Canadian dividend stocks are undervalued? I tend to use a combination of methods and here are the three that I use most often.

Relative P/E Ratios

A common metric for determining when stocks are undervalued is the Price to Earnings ratio, otherwise known as the P/E ratio. In this ratio, the stock price is divided by its annual earnings to come up with a number. The lower the number, the “cheaper” the stock.

The one thing about this ratio is that it can be deceiving in that “earnings” can be manipulated with creative accounting. As well, some industries often report relatively low “earnings” but have strong cash flow (like real estate investment trusts). Another variable, sometimes the market rewards growth companies with a higher P/E.

As you can see, P/E ratio can be subjective and not a great single measure of value, but I often use the P/E ratio as a comparison and starting point when researching strong companies within the same sector.

Average 5-year Yield

Another way that you can see if a company is trading at below their historic levels is to compare its current yield to its 5-year average yield. Remember that dividend yields go up as the stock price goes down.

So if the current yield is higher than the 5-year average (ie. attractive), then it may be a good starting point for your research on why it’s trading lower, and if you expect the fundamental business to continue growing going forward. If everything appears normal and it seems that the market is just being temperamental, then it may be time to start/add to that position.

For example, as of this post, Canadian Tire is trading with a yield of 4.35% and their 5-year average yield is 4.20%. This indicates that it may be a good time to add to (or initiate) your position depending on if you like their business prospects going forward. With a 14-year dividend growth streak at a low payout ratio of only 44%, you can see why I think it might be undervalued.

Payout Ratio

A payout ratio is the percentage of earnings a company pays its shareholders, usually in the form of dividends.

One way payout ratio is calculated is by dividing the dividends by net income:

Dividends/Net Income = Dividend Payout Ratio

A healthy payout ratio isn’t too low or too high. A high percentage means the company is paying out a considerable amount of their earnings, which means their cash flow will be tight. A low payout ratio could mean the company is in a growth phase and needs to reinvest profits to grow its operations.

Generally speaking, when it comes to building up a dividend portfolio, you’ll be looking for an ideal payout ratio of 30-50% as it shows the company is considering its investors, and wants to reward them, while maintaining growth of the company.

It’s important to point out that pipeline companies are an exception to this ideal ratio. Let’s take Enbridge (ENB) for example, with its 140% payout rate. At first glance, this might seem highly unsustainable, and therefore risky.

The reason is because companies like Enbridge calculate the payout ratio based on distributable cash flow, so the actual payout ratio is closer to 60-70%. This still might seem high, but it’s a strong company with a long track record of solid dividend payouts, so it’s still a safe bet.

Technical Analysis – Using Moving Averages

A third factor that I consider before adding to a position is the use of basic technical analysis, more specifically, using the long-term moving average.

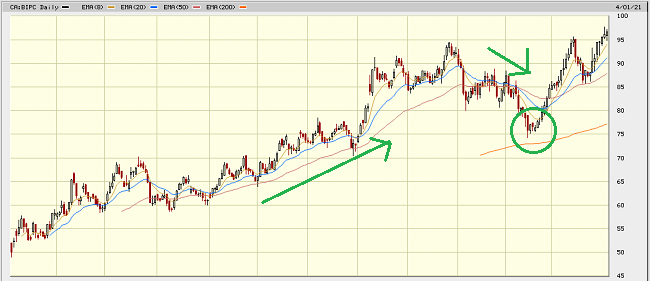

Personally, I tend to add to positions when they are on an uptrend but have pulled back to their long-term moving average, like the 200 day simple moving average (SMA).

In the example below, I had a position in BIPC but noticed after a strong uptrend (first arrow) that it was selling off and it pulled back (second arrow) close to the 200 day moving average. I like the future prospects of BIPC and added to my position in the circle area.

Advanced Tools and Portfolio Management

Here at MDJ we fully endorse Dividend Stocks Rock. Headed by our friend Mike, they have an extremely impressive, proven track record when it comes to maximizing divided performance. With DSR, you’ll not only get access to some powerful tools that will immediately improve the way you manage your portfolio, but also direct advice and feedback from some of Canada’s leading experts when it comes to dividend investing.

Combined with our exclusive discount setup and the fact they offer a 60 days money back guarantee – there is currently no better choice on the market. You can read our detailed detailed DSR review, or sign up using the button below.

My Dividend Portfolio

If your goal is to use stocks to help reach financial independence, buying strong Canadian companies when they look undervalued can be a very sensible place to start. Dividend stocks in particular can do a lot of heavy lifting over time. They give you a chance to benefit from long-term capital appreciation while also building an income stream that can eventually help cover real-life expenses.

As many of you know, I use a dividend investing strategy for the Canadian portion of my portfolio. The basic idea is pretty simple. I focus on large, established companies that pay dependable dividends and have a long history of increasing those payouts over time.

I started building that portfolio back around 2008, and over the years it has grown to the point where it can cover our recurring annual expenses. That is a big reason why I put so much weight on income dependability and long-term business quality when looking at Canadian stocks.

Here are my current top 10 positions that I have built up over the last 25 years of investing:

- TD Bank (TD)

- Enbridge (ENB)

- Canadian National Railway (CNR)

- TC Energy Corp (TRP)

- Telus (T)

- Fortis (FTS)

- Power Corp (POW)

- Emera (EMA)

- Royal Bank (RY)

- CIBC (CM)

These top 10 positions vary a bit over time as their values go up and down. However, while their value goes up and down, these top 10 tend to pay dependable dividends that tend to increase over time. As I plan on living off dividends in the near future, income dependability is a high priority.

If you are just starting out, check out my post on how to build a dividend portfolio. The post shows that I tend to pick the leaders in each sector that pays a dividend and own them forever.

Here are some market leaders and a starting point for your research:

- Telecom – BCE (BCE), Telus (T), Rogers (RCI.B)

- Pipelines – Enbridge (ENB), TransCanada Corp (TRP).

- Banks – Any of the big banks: Royal Bank (RY), Toronto Dominion Bank (TD), Scotia Bank (BNS), Bank of Montreal (BMO), CIBC (CM); Insurance: Manulife (MFC), Great-West Life (GWO), Sunlife (SLF).

- Resources and Materials – Suncor (SU), Canadian Natural (CNQ), Teck Resources (Teck.b)

- Utilities – Fortis (FTS), Canadian Utilities (CU), Emera (EMA), Brookfield Infrastructure Partners (BIP.UN/BIPC), Algonquin (AQN).

- Health Care – Canada is weak in this sector in terms of dividend stocks.

- Retail – Empire (EMP.A), Loblaws (L), Canadian Tire (CTC), Dollarama (DOL)

- Industrials – Canadian Pacific Railway (CP), Canadian National Railway (CNR), Finning International (FTT), Waste Connections (WCN)

- Technology – Enghouse (ENGH), CSU

- Real Estate – Riocan (REI.UN), CHP.UN, CAR.UN

When building a dividend portfolio, I believe that it’s important to simply initiate a position and keep adding to it as it becomes undervalued and/or when new savings become available to invest.

To learn more about the Best Canadian Dividend Stocks, check out our full article where we give you all the details on how you can build a passive income portfolio too.

Final Thoughts

Choosing the best Canadian undervalued stocks takes a bit of understanding beyond what you need to know for a more straightforward buy and hold type of purchase. However, once you know the basics, it’s pretty straightforward.

It’s really about looking for companies with a strong performance history and digging into a few key metrics to help you make your pick. Companies that are well established and have a decent growth record are going to be a good bet when it comes to buying undervalued stocks. Another key to helping you maximize returns on undervalued stocks is buying when the selling price dips, knowing it is likely to rebound and grow in the future.

An added bonus of these stocks is that you’ll get dividend payouts, so you can use your returns at the time of payout rather than decades. This is a big bonus for those looking to add money to their wallets without extra work.

Interested in learning more about the best dividend stocks in Canada? Head over to our Canadian Dividend Kings List and our Dogs of the TSX Dividend Stock Picks.

I’m curious how the Nutrien outlook changes when you consider the new Jensen mine in Saskatchewan (being built by BHP). It is scheduled to start production in 2027 and is expected to become one of the world’s largest potash mines.

To my way of thinking Neil, the extra supply into the market is still not even close to the broader demand story caused by increasing population and a warmer climate.

Nice list. Thanks for sharing. I keep adding NS and TD. I am also a fan of MFC and keep adding on red days. So far so good! It has higher yield than other big banks.

I also own ENB, CNQ, and TRP. I don’t feel I want to buy CU anymore. I am more into renewable energy and prefer RNW, BEP.UN over Oil companies. What do you think about the renewable energy companies?

And for health, I started buying 2 ETFs covering mostly US health companies. FHI.B (Yield 8.64% and HIG 6.04%). Yes, we lack good health stocks dividend or growth locally.