Investing in Canadian Bank Stocks 2026

As we look at the possibilities for investing in Canadian bank stocks in 2026, it’s important to realize just what an incredible year we’re coming off of in 2025.

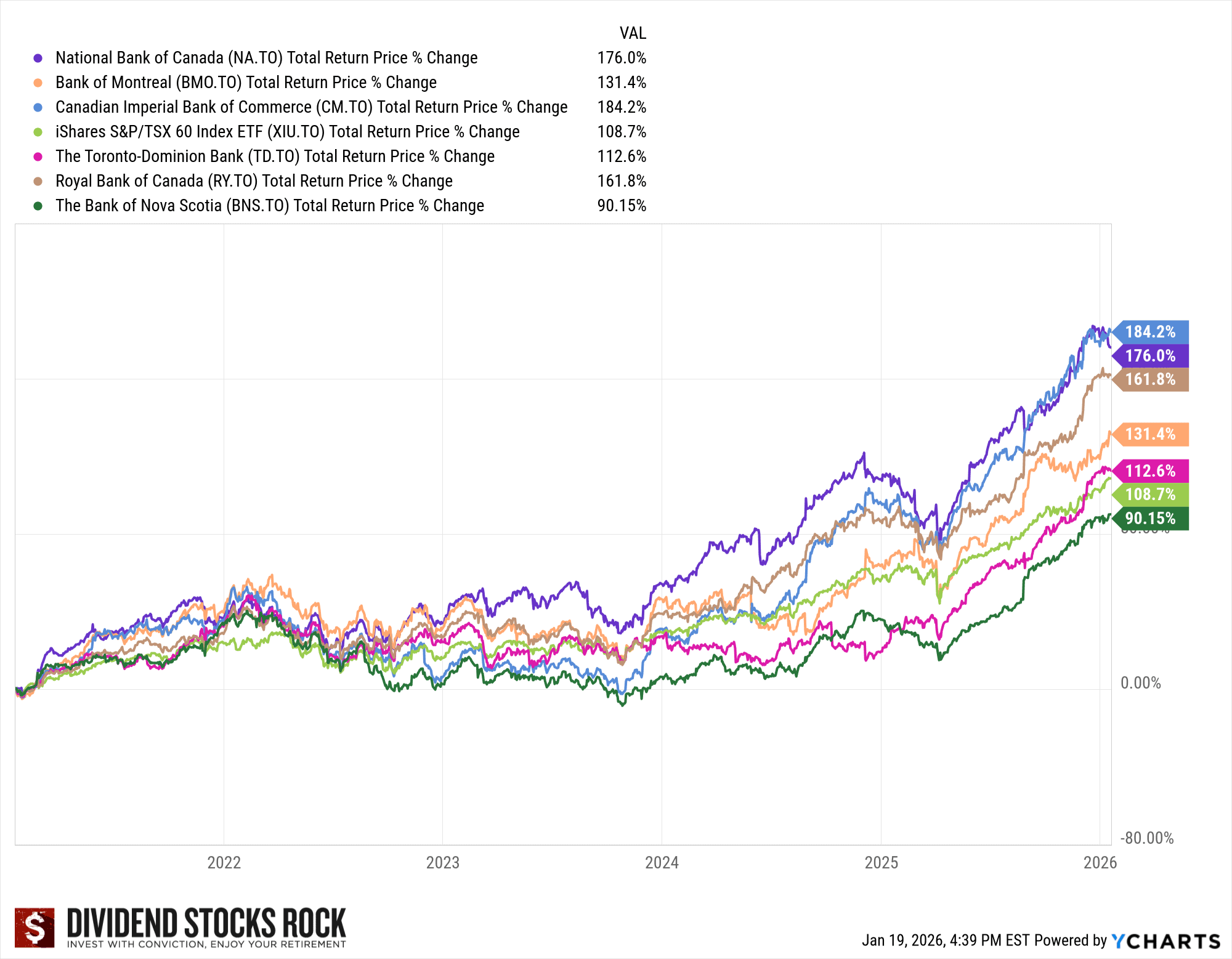

As you can see in the chart below, TD was the runaway winner, but all six Canadian banks rewarded shareholders handsomely. They were some of the best performers on our Best Canadian Dividend Stocks list.

Mike Heroux created the chart above, and his newsletter is one that is personally at the top of my “must read” list. Click below to get on Mike’s free newsletter list and find out more about his exclusive Dividend Stocks Rock platform.

Here’s what I wrote about Canadian bank stocks when I wrote my predictions at this time last year:

In 2024 we went two for three with our Canadian bank stock recommendations. National Bank and RBC have been my two most recommended stocks in this sector for the past five years, and both did excellent. RBC finished the year up 38%, with National Bank not far behind at 35%. Both banks significantly outperformed the TSX60 index on the year

I will admit that I feel a bit burned by missing out on CIBC’s scorching 53% gain in 2024 – but to be honest, I didn’t see that one coming. After years of underperformance, and just generally feeling like the least-loved of the big bank brands, CIBC clearly did something right. A lot of that earnings momentum though came from PCLs not being as bad as they had expected – and that’s a trick that can only be done once, as there is no underlying business growth behind that number.

Now… I’m not quite as proud of my third pick – but I still think the long-term investment thesis makes sense when it comes to TD Bank. In case you weren’t aware, TD’s earnings report got overshadowed by the massive amount of money that they had to set aside to pay a penalty in the US. Long story short, TD is being investigated for laundering hundreds of millions of dollars for drug cartels.

Not a great look.

TD sold some of the Charles Schwab shares they had in the pantry from their TD Ameritrade brokerage merger back in 2020 in order to come up with the $4 billion they figure they will need to pay the penalty. (The 2nd biggest penalty ever levied in North American banking.)

Now – all of that said – do you know any Canadians who have stopped banking with TD because of this activity?

I don’t. Not one. Nobody has talked about moving their mortgage or switching lines of credit. Heck, other than investors, I don’t know a single Canadian that’s even aware of this news story.

Consequently, I think TD’s Canadian operations will remain quite profitable.

I’m pretty proud of that call, as patient TD investors benefitted massively last year to the tune of a 70% total return!

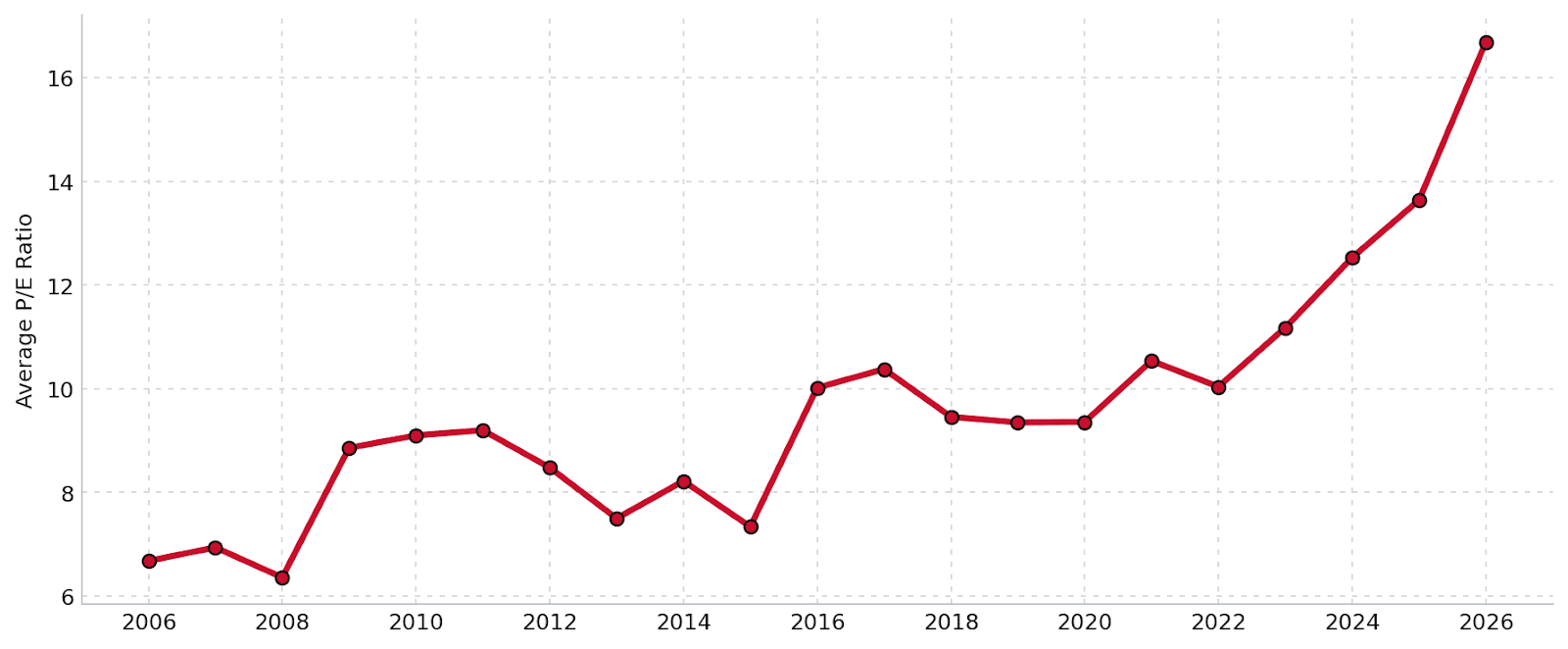

As we look ahead to 2026, I have to admit I’m about as lukewarm as I’ve been on Canadian bank stocks in a while. They continue to be quality companies, but I’m getting a bit concerned about valuations. If we take RBC as an example below, we can see that its valuation is substantially higher than it has been at any point in the last twenty years. Theoretically, for RBC’s prospects to be this good, we’d have to assume that RBC is going to massively raise profits going forward.

I don’t know about you, but the Canadian economy doesn’t exactly scream massive growth at the moment. Will RBC continue to make a lot of money?

Certainly.

But will it rapidly increase the already-massive-but-stable stream of profits it currently enjoys? I’m not so sure about that.

I’d personally just take the average of the Canadian banks this year, since I don’t see an angle for a standout performer. I still like National Bank’s room for growth, but I’m concerned about the recent political upheaval in Quebec affecting the stock. Any real sign of Quebec separation is going to really impact this company’s value.

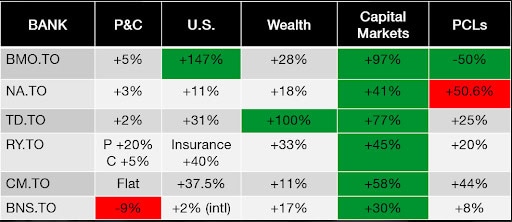

You can see below that while Wealth Management and Capital Markets had an excellent 4th quarter in 2025, classic banking activities aren’t doing great. The good news is that payout ratios remain quite low, so it’s quite unlikely these banks will have to cut their dividends, even if worst-case scenarios start to materialize.

Owners of Canadian bank stocks know that the big banks operate in a very protective oligopoly here in Canada, and consequently, their wide moat allows them to pass along price increases very efficiently – thus protecting profit margins.

Canadian Banks vs. The Best Dividend Stocks in Canada

Here’s a snapshot of how Canadian bank stocks compare to big companies in other sectors. For more information, read our best Canadian dividend stocks article, or our list of dividend kings in Canada.

Name | Dividend Yield | 5yr Revenue Growth | 5yr EPS Growth | 5yr Dividend Growth | Payout Ratio |

Scotiabank | 4.29% | 3.12% | -0.46% | 3.91% | 73.94% |

CIBC | 3.36% | 8.37% | 12.60% | 6.39% | 45.00% |

TD Bank | 3.31% | 9.11% | 12.20% | 6.01% | 36.19% |

Bank of Montreal | 3.49% | 7.15% | 6.84% | 8.99% | 55.97% |

Royal Bank | 2.82% | 6.40% | 10.32% | 7.49% | 42.79% |

National Bank | 2.99% | 9.96% | 10.53% | 10.79% | 45.77% |

?????? (Hidden, click for access) | ??????? (Hidden, click for access) | ?.??% | ?.??% | ?.??% | ???.??% |

2025 Canadian Bank Stock Earnings

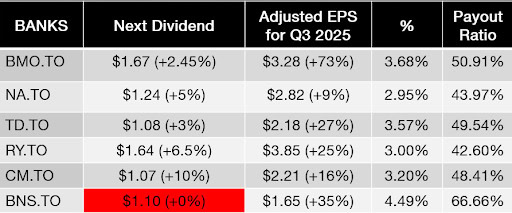

The final quarter of 2025 was excellent for the banks, and they saw their earnings per share up massively from a year prior. They all continued to increase their dividends and their usual rate.

Now it’s important to understand that the Provision For Credit Losses (PCLs) strategy (which is a bit of an accounting game) is driving earnings alongside overall stock market growth (making for huge capital markets revenue).

Overall, I think that Canadian bank stocks are going to be flat in 2026. They could certainly surprise me, but I just think asking more from these stocks after the massive run up they had in 2025 is a tough ask.

If you want to dive into the nitty-gritty details of the most recent bank stock earnings reports, you should check out Mike Heroux’s video below. You can also snag an automatic promo offer code for Mike’s Dividend Stocks Rock platform (exclusive to Million Dollar Journey readers) by clicking the link underneath the video.

National Bank and Canada Western Bank Merger

The other big news in the Canadian banking sector this past quarter was the major expansion by National Bank via an acquisition of Canadian Western Bank (CWB) the eighth-largest bank in Canada. The TLDR is that National Bank is going to buy CWB’s assets for $4.7 billion.

Most notably, that means that National Banks gained 65,000 clients overnight, and 39 branches in a part of the country that NB didn’t have any footprint in. The goal will of course be to market some of National Bank’s existing services to CWB’s client list.

While gaining more market share in the Canadian banking oligopoly is nearly always a winning proposition, National Bank did have to pay a pretty penny for the deal. Before the acquisition was announced CWB’s shares were valued at just under $25 each, and they will be “purchased” at $52.24. Any time you can make a 110% gain on your investment, that’s a pretty good deal!

As a result of the high price tag (which was mostly financed by issuing new shares, as well as securing financing from the Quebec pension fund) National Banks share values did take a brief hit before heading higher and setting new all-time highs this past quarter. In the big picture, National Bank appears to be firmly planting their flag in the “we are going to become a full-fledged cross-country competitor to the other big banks” as opposed to their previous Quebec-centric business model.

Canadian Banks are Not SVB or Credit Suisse

Investing can be scary sometimes.

When investing involves banks, there is often an exponentially greater emotional response because often it’s not only your stock exposure at risk – but your chequing account, maybe business account, etc.

Consequently, when phrases like “bank runs” start to be uttered, it can be tempting to run for the exits. Of course, if companies are fundamentally sound, buying in at low valuations is exactly how you beat the market. Anyone can invest with conviction when all the news is good, but it’s the ability to separate the noise from the reality when things aren’t so rosy that generally determines long-term outperformance.

If you Google “Credit Suisse” you’ll see that the bank has had a lot of problems over the last ten years. Frankly, it has been involved with a lot of really bad people/entities – one might even say “shady” endeavors – and it doesn’t shock me that they look the most shaky out of the large “world systemic banks”. But even Credit Suisse appears “to big to fail” now with the Swiss Government stepping in and back-stopping liquidity worries.

When it comes to SVB, it’s a really interesting case study from a geeky economics/business point of view, but what it really boils down to is a ridiculous risk management decision for that particular bank. It was an awful decision to have essentially put all of their “safe assets” – or “tier one liquidity” as we like to say in Canada – in long-term US Treasuries when we were about to enter a raising interest rate environment. When you consider a huge percentage of their depositors (startups and tech companies) are also very sensitive to interest rate hikes, you have the makings of a perfect storm.

Neither of these two banks has much to do with the Canadian banks we’re discussing here. You might say that on the fringes, BMO and TD investors might have some small worries when it comes to recent American acquisitions, but given the strength of the US labour market, as well as the new guarantee by both the Fed and the Biden Government, I wouldn’t worry all that much.

BMO’s Bank of the West acquisition would be the closest connection to the recent headlines, just due to geographical proximity to SVB, as well as having slightly elevated numbers of non-insured deposits vs the major US banks. That said, the US government just implicitly guaranteed all bank deposits, so I’d say that systemic risk is now off the table.

As a major TD investor (added to my position amidst the chaos on Monday – so didn’t get it at the bottom, but I’m happy with my discount) it certainly wouldn’t break my heart to see the $13.4 billion acquisition of First Horizon Corp go quietly into the night. Perhaps at the very least, TD can use this regional banking weakness to renegotiate more advantageous acquisition terms.

On a purely fundamental level, I think it’s worth pointing out that quarterly earnings results from a few weeks revealed that the Canadian banks continue to make a lot of money, and that the major reason that earnings per share numbers weren’t through the roof was something called “PCL”.

PCL is actually pretty important as it stands for Provision for Credit Loss. That money the Canadian banks are setting aside is the exact reason that I’m not nervous about them in terms of their long-term sustainability. A little pain in the short term due to decreased quarterly earnings, is more than worth the heartburn some American bank investors felt this week.

To recap, RBC, CIBC, TD, and National Bank, all substantially beat their quarterly consensus earnings predictions. BMO and Scotiabank both had solid-if-unspectacular quarters as well. The Big 6 all remain very liquid and very well capitalized.

I haven’t noticed any rush within Canada to pull money out – and with FDIC insurance, why would you? That being the case, I don’t see any reason to believe that investing in Canadian bank stocks is any more risky in the long-term than it was a month ago.

Investing in The Big Canadian Banks – Overview

Royal Bank of Canada (RBC)

RBC is the reigning king of Canadian banking. Royal Bank of Canada is a Canadian multinational financial services company and the largest bank in Canada by market capitalization. The bank serves over 16 million clients in Canada, the U.S. and 27 other countries.

They are one of North America’s most diversified financial services companies, and provide personal and commercial banking, wealth management, insurance, investor services and capital markets products and services on a global basis.

In summary, they are a dividend/earnings beast with so many ways to make money.

TD Bank (TD)

TD is also a very well-diversified bank that concentrates on Canadian and U.S. retail banking and wealth management. In fact, TD has more branches in the U.S., compared to Canada. That said, they generate more revenue and earnings in Canada. That speaks to the very profitable oligopoly situation in Canada.

TD Bank Group offers a full range of financial products and services to more than 26 million customers worldwide. TD also ranks among the world’s leading online financial services firms, with more than 15 million active online and mobile customers.

U.S. financial giant Charles Scwab (SCHW) purchased TD Ameritrade in 2019, giving TD a 13.5% stake in Schwab. Consequently, with TD you’re getting some very nice U.S. exposure.

Scotiabank (BNS)

Scotiabank is the most International of the Canadian banks. Scotiabank serves more than 26 million clients in Canada, and offers a range of products and services in the U.S., Latin America (excluding Mexico), and in select markets in Europe, Asia and Australia. They have a very robust global and capital markets division that includes lending, deposit, cash management and trade finance solutions and retail automotive financing operations.

While there is great potential in developing markets, they have not always executed with precision in these foreign markets and have generally lagged behind the leaders in recent years.

Scotiabank also owns Tangerine, Canada’s leading online bank.

Bank of Montreal (BMO)

BMO might be considered the most forward-thinking of Canada’s big banks when it comes to introducing cost-cutting options in recent years.

BMO serves more than 12 million customers, with 8 million via Canada operations. They operate in three divisions – personal and commercial banking, capital markets and BMO wealth management. BMO has been aggressively expanding its U.S. footprint through a series of operations.

In Canada they are well positioned as the leading bank with respect to ETF assets under management. They are in second place in Canada, only behind BlackRock, but BMO is gaining ground and closing that gap. They also offer advice-Direct, a digital investment advice and portfolio management platform.

Canadian Imperial Bank of Commerce (CM)

CIBC can often be classified as the also-ran among the big 5 Canadian banks. They have made some missteps and have lagged the other banks with respect to diversifying outside of Canada.

In 2019, Barry Schwartz, chief investment officer of Baskin Wealth Management, offered “They seem to be swinging past the fastballs and missing the easy layups that the other banks get right.” That said, analysts appear to be warming to CIBC’s recent efforts.

CIBC serves 10 million customers and operates Canadian personal and commercial banking, plus wealth management. In the U.S. they offer commercial banking and wealth management. They also have a capital markets division.

Dividend investors love CIBC’s commitment to paying shareholders consistently and just because they aren’t the leading name, doesn’t mean they can’t hold leading value at a certain price point!

National Bank of Canada (NA)

National Bank is a regional bank (Quebec) that has been successfully diversifying. National is a very well-run bank, and has been the top-performing big Canadian bank for 20 years or more. It is the favourite value of Dividend Stocks Rock – our most trusted source for dividend growth information.

National generates 50% of its revenues in Quebec, which it then uses to fund additional growth projects outside of Quebec’s borders. Wealth management is growing at 15% annual over the last 10 years. The bank is also active in the U.S. and emerging markets.

The fact is that National Bank is a bit smaller and more nimble (compared to the big 5) and more responsive as they seek acquisitions. This could lead to outsized gains versus its large market cap banking brethren.

Where to Buy Canadian Bank Stocks

This stocks can be bought through any broker – all you have to do is open an account, add funds and pick the specific stock you want to buy. For more information you read our comparison of the best online brokers in Canada.

Best 2026 Broker Promo

Up To $2,000 Cash Back + Unlimited Free Trades

Open an account with Qtrade and get the best broker promo in Canada: $100 when you invest $1,000!

The offer is time limited - get it by clicking below.

Must deposit/transfer at least $1,000 in assets within 60 days. Applies to new clients who open a new Qtrade account by July 31, 2026. Qtrade promo 2026: CLICK FOR MORE DETAILS.

Canadian Bank Stocks: Cheap or Overvalued?

When I made that TD call back in January, I didn’t expect it to pop +33% in the first 7 months of 2025.

That said, given the excellent performance of Canadian Bank Stocks the last couple of years, there is just no way we can call them “cheap” in any conventional sense. Even if earnings go up from here, the current valuations of these companies look pretty darn pricey.

I prefer when you can buy bank stocks at 10x earnings, not the current 14-15x. For what it’s worth, the 3-yr average P/E is about 12x.

Now, it’s not like Canada’s labour market is crumbling. Forecasts for a prolonged downturn have moderated since the peak of tariff chaos. The banks are setting aside more provisions for credit losses (PCLs) than usual, anticipating a rise in delinquencies. That kind of caution goes a long way in earning investor trust.

Housing apocalypse talk is overblown. Most Canadians either own their home outright or locked in cheap, long-term mortgages. Insolvency rates are actually still below 2019 levels.

For dividend-focused, long-term investors (especially those betting on Canada’s resilience in the face of tariff threats) these banks offer strong yield, solid fundamentals, and a familiar playbook.

I’ve already trimmed some holdings to lock in gains – but I’m not hitting eject. These financial giants are still profitable, still regulated, and still a central piece of many Canadians’ long-term portfolios.

Investing in Canadian Banks: FAQ

Canadian Bank Stock Dividends For the Government?

The federal Liberal government is looking to hit the financials coming and going. First off, they are looking to increase the corporate income tax rate from 15% to 18% on all earnings above $1 billion. It is estimated that collectively it will cost the big banks about $1billion in profits each year.

Also, the big Canadian banks and insurers will be paying a Canada Recovery Dividend. The two programs are slated to begin in 2022-2023 and will run over a four-year period. The rate or amount of the Canada Recovery Dividend will be negotiated over the coming months.

Analysts do not see this as a major hit to the very profitable banks and insurance companies. The taxes are likely already priced into the stocks, as bank analysts already know what’s coming down to the pipe.

It may be best to focus more on the long term growth prospects and those growing dividends that will end up in your pocket.

Investing in Canadian Banks for 2026 – Ignore the Noise

As you can see from the chart above, there are great reasons to love and trust Canadian bank stocks for the long term.

The stability of Canadian bank dividends helps all investors moderate their “animal spirits” when it comes to panic selling, and their track record when it comes to allocating capital for expenditures is second-to-none. This moderate tone will serve bank investors well 2026, as news headlines declare that the sky is falling due to tariffs, recessions, etc.

With all the negative news in 2024 (and I think it will get worse in 2026), the current entry prices for Canadian bank stocks seem pretty fair compared to most.

The unique regional background of National Bank, combined with its smaller market cap relative to its “Big 6” bank cousins, gives the company the most solid prospects for growth out of the Canadian banks.

RBC has simply proven year in and year out to be worthy of their “best in class” status. The sheer scale and diversity of their revenues continue to make them one of the safest stocks in the world from my point of view.

Small online-only EQ Bank might also be worthy of consideration, as it has seen substantial growth over the last few years. It’s now on our radar from an investment perspective (it has long been on my personal radar as a longtime customer).

At the end of the day, nothing that has happened in the last ten years has done anything to shake my faith in Canadian bank stocks. They operate in a protected oligopical environment, benefit from massive barriers to entry, are well run, and profit off of Canadians’ collective indifference to fees and costs.

With Canada’s working population being juiced by aggressive immigration policies, the only real question is which Canadian bank stocks will reward their shareholders with outsized returns (instead of merely solid earnings growth). For other investment options, read our best Canadian dividend stocks page, or our list of Canada’s dividend kings and aristocrats.

Best 2026 Broker Promo

Up To $2,000 Cash Back + Unlimited Free Trades

Open an account with Qtrade and get the best broker promo in Canada: $100 when you invest $1,000!

The offer is time limited - get it by clicking below.

Must deposit/transfer at least $1,000 in assets within 60 days. Applies to new clients who open a new Qtrade account by July 31, 2026. Qtrade promo 2026: CLICK FOR MORE DETAILS.

My favorite etf to invest in a selection of banks is HCAL. Its long term returns speak for itself…

Refresh my memory please, did MDJ have a link to an article where the investor was 100% dividend driven, investing only in the banks, insurance, communications & energy?

Was just checking in on this post. It was suggested that banks deliver 17% from that yield level historically. We’re above 14% already. Wow.

More to come if the fears of inflation and rising rates hang around.

Dale

Banking stocks (not just Canadian) seem like a great bet due to their depressed prices and just the heady rise in tech stocks making them out of favour.

A 4% divi yield? what isn’t to love about that.

Thanks for the OSFI tip restricting dividend increases for the banks. I did not know that.