Investing In Canadian Wide Moat Stocks

As I’ve moved into semi-retirement, my investing priorities have changed a bit. I still want equities-backed growth, because retirees who ignore stocks entirely are basically asking inflation to slowly chew through their purchasing power. But I’m much less interested in owning volatile companies that might have a really high ceiling – and also might see their competitive advantage reduced to nothing with the next software update.

At this stage, I want the equity side of my portfolio built around businesses that have already proven they can survive a few rough cycles. Think banks, railways, utilities, and other companies with real competitive advantages. They might not make for the most exciting stock tips newsletter, but they tend to have the kind of pricing power, recurring demand, and balance sheet strength that allows me to sleep well at night.

The way I think about it is pretty simple: I’m not trying to win by finding the next tiny stock that goes up 10x. I’m trying to win by owning fewer companies that blow up, cut their dividend, or slowly turn into permanent disappointments. Avoiding the big losers can be just as important as finding the big winners, especially when you’re no longer in the aggressive accumulation stage of life.

That focus naturally pushed me toward researching Canadian moat stocks. There is a lot of overlap here with top Canadian dividend stocks, because the best dividend growers often have the same underlying traits I’m looking for: Durable profits, shareholder-friendly management, and a high barrier to entry that detracts new market entrants. This set of traits is generally referred to as an economic “moat” due to its protective characteristics.

Our preferred research tool for this type of dividend investing is Dividend Stock Rocks (DSR). It’s run by financial advisor Mike Heroux, and focuses on dividend stock analysis, portfolio tracking, and improving long-term portfolio quality. You can read our full DSR review, or sign up and get 33% off by clicking the button below.

Finding Quality Moat Stocks in Canada

Canada is unique in that there are many very good dividend-paying companies that operate in an oligopoly situation. There is little competition and they are often protected by government regulators to boot. This is essentially the definition of a “moat stock”.

Here is a simple explanation of what moat stocks are courtesy of investopedia.

“A wide economic moat is a type of sustainable competitive advantage possessed by a business that makes it difficult for rivals to wear down its market share. The term economic moat was made popular by the investor Warren Buffett and is derived from the water-filled moats that surrounded medieval castles.”

Essentially, when someone says they are interested in investing in moat stocks, they are looking for companies that have a durable competitive advantage over the long term. While a technology company might very well get disrupted by another newer technology company, it’s much harder to supplant Enbridge’s pipeline, or CNR’s railway!

My Canadian moat analysis mostly centres around Canadian pipeline stocks, Canadian bank stocks, Canadian Telco stocks, Canadian utility stocks, Canadian Railway stocks, and (even though it only partially falls under the “moat” category) I also wrote about investing in Canadian energy stocks.

Some market analysts would also include Canadian grocers under the “moat stocks” subheading. In this post on Canadian retail stocks I suggested that you could certainly build your retail stock component around the grocers that dominate the Canadians landscape.

Taking Dividend Investing to the Next Level

Dividend Stocks Rocks (DSR), is a highly recommended newsletter and product if you want to take your dividend investing to the next level . It has been managed by my fellow blogger Mike from the Dividend Guy Blog since 2013.![]()

DSR is not just a weekly newsletter with stock picks. It’s a program that will help you manage your portfolio and improve your results. You can first read our detailed DSR review, or sign up now by clicking the button below.

The Canadian Wide Moat 7

Personally, for my RRSP portfolio (and the core Canadian equity component) I hold a concentrated portfolio of dividend moat/wide moat stocks. I do shade in some Canadian energy, and other commodities for inflation protection.

Here are the holdings for my personal Wide Moat 7.

Banks: Royal Bank of Canada, National Bank, and Toronto-Dominion Bank

Telecommunications: Telus

Pipelines: Enbridge and TC Energy

Railways: CNR

| Canadian Moat Stock | Current P/E | Current Dividend Yield | Last 5 Years Share Price Performance |

| RBC Bank | 16.94 | 2.66% | 104% |

| National Bank | 19.82 | 2.41% | 127% |

| TD Bank | 11.89 | 2.95% | 69% |

| Telus | 23.49 | 9.64% | -34% |

| Enbridge | 23.06 | 5.20% | 56% |

| TC Energy | 27.76 | 3.96% | 45% |

| CNR | 19.93 | 2.42% | 18% |

The averages from this table are:

| Canadian Moat Portfolio | Current P/E | Current Dividend Yield | Last 5 Years Share Price Performance |

| Wide Moat Average | 20.48 | 4.18% | 55% |

I landed on this portfolio as I had held these stocks for quite some time. I realized that my core moat of big dividend-paying companies were my best performing group. I am a big fan of investing using Canada’s best ETFs, don’t get me wrong, but I decided to mix that with this conservative, long-term conservative focus on Canadian dividend moat stocks that had a durable competitive advantage.

I did not purchase these stocks only based on the generous and growing dividends, but that is a welcome by-product of investing in very profitable companies that are able to grow earnings and free cash flow over time. The dividends come along for the ride. We can thank the moats (and the protected Canadian market) for that benefit

Total Returns for My List of Canadian Wide Moat Stocks

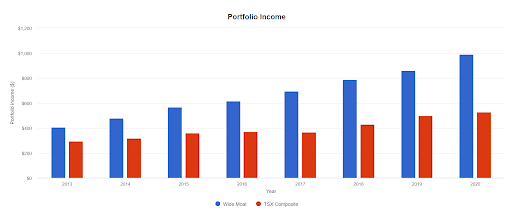

While the dividends are wonderful (we’ll get to that next), in the end it will come down to the total returns. How much income can I create by way of dividends and selling shares? That is, total return. While dividends feel good, retirement funding success comes down to the total return and the risk level.

The total 5-year share price return for my Canadian Wide Moat stocks were 55% – which is about a 9.2% annualized (again, not taking dividends into consideration). That sounds pretty good until you realize that a basic Canadian index fund of the TSX 60 would have given you a 5-year return of 77% (12.1% annualized).

That being said, my wide moat stocks held up better during the period just before the current 5-year track record (during the pandemic), and one of their main features is a lack of volatility. On this score account, they trounce the Shopifys of the world which go up and down pretty quickly.

Obviously Telus’ performance drags down the portfolio substantially. This is an interesting case where the government helped Quebecor build a bridge over the investment moat, and introduced a new competitor to the “Big 3” which had substantial pricing power before that. Combined with higher interest rates and a lack of ability to charge a premium for expensive 5G services, and Telus has underperformed even while pumping out a substantial dividend.

My wide moat portfolio did do better when we take dividends into account as the average dividend yield of about 4.2% was substantially higher than the 2.85% that the Canadian index averaged of the same period. Once we include dividends, we see that the 5-year total return for the moat stocks was about 90% (13.6% annualized) and the TSX index was about 104% (15.3% annualized). The good news is that those are some absolutely fantastic numbers by any measure!

We see that the Wide Moat stocks have slightly trailed Vanguard VDY and the TSX Composite over the last 10 years. The high dividend stocks were outperforming for quite some time. But it should be no surprise that the high dividend space came under great pressure when inflation was unleashed and the Bank of Canada went on the most aggressive rate hike cycle in decades.

Higher yielding stocks can underperform in these conditions as they often carry higher debts (increased debt servicing costs) and they then compete with high interest savings accounts and the best GICs in Canada. Money leaves the space for those other risk-free options.

Best 2026 Canadian Bank Offer:

2.75% Everyday Interest Rate

Open an account with EQ Bank & get the best interest rates in Canada: 1% + 1.75% interest rate if you direct deposit your pay.

The best daily interest rates in Canada* and great rates for GICs - up to 4.00% guaranteed in your registered account. Get it by clicking the button below:

* Rates are subject to change ** Applies to both New and Existing clients who open a new account. ***EQ Bank Review: more details

Other Canadian Companies With Large Moats

I’ll be the first to acknowledge that there is certainly considerable concentration risk in a portfolio of 7 stocks. And that’s why I suggest Million Dollar Journey readers look to those aforementioned sectors if they choose to embrace the Canadian Dividend Wide Moat Investing approach and widen their portfolio a bit.

You might add:

Grocers (they also offer pharma exposure): Metro, Loblaws, and Empire

Railways: CP Rail

Utilities: Fortis, Canadian Utilities, Emera

As a unique add-on to these moat portfolio options, you might consider Nutrien and Cameco. These companies operate in very niche oligopoly-esque sectors (potash and uranium production) and both have long-term durable competitive advantage.

Personally, If I were going to expand my Canadian Wide Moat 7 into a Wide Moat 10, I would not simply add more banks, pipelines, or telecom stocks. That would defeat the whole purpose. The current list already has plenty of exposure to Canada’s classic oligopoly sectors, so the next three additions should ideally bring something different to the table.

The three stocks I’d put at the top of my watchlist are Canadian Pacific Kansas City, Waste Connections, and Fortis. They are not all identical businesses, and they are not “cheap” in terms of their current valuations. But they each have pretty deep moats in my opinion.

Canadian Pacific Kansas City is probably the most obvious candidate. I already own CNR in the Wide Moat 7, so adding CPKC would mean doubling down on railways. I get why that might feel a bit repetitive, but railways are one of the clearest economic moats in Canada. You cannot wake up tomorrow, raise a few billion dollars, and casually build a competing national rail network. Truthfully, the idea of building a railway of any size in our country is astoundingly odds. CPKC also has a unique North American angle after combining Canadian Pacific and Kansas City Southern, giving it a single-line rail network across Canada, the United States, and Mexico.

Waste Connections is another business that fits the moat profile extremely well. Garbage collection is not glamorous, which is part of the appeal. It is essential, recurring, heavily local, and difficult to disrupt. The real moat is not just “people keep making garbage” (although, sadly, that appears to be one of humanity’s more reliable trends). The moat comes from route density, local contracts, landfill ownership, regulation, and the fact that most communities are not exactly lining up to approve new landfill sites.

Fortis is the more conservative addition. It is a regulated utility, not a fast-growth compounder, and no one is going to confuse it with the next great technology stock. But for this type of portfolio, that is not a dealbreaker. Fortis brings regulated earnings, a long dividend-growth history, and a business model built around electricity and gas infrastructure that people use in good economies and bad.

At the end of the day, Canadian moat stocks are not about finding the most exciting companies on the TSX. They are about owning businesses that are difficult to compete with, provide essential services, generate reliable cash flow, and have a long history of rewarding shareholders. My updated Wide Moat Portfolio is still very Canadian, so I would not pretend it is a substitute for a properly diversified global ETF portfolio.

The recent comparison against the average returns of the Canadian stock market is also a useful dose of humility. Quality stocks do not automatically beat the index over every time period, and a few weak performers can drag down even a carefully chosen basket. Remember, the goal is to own high-quality businesses that you can comfortably hold through the inevitable ugly stretches while still collecting a healthy stream of dividends along the way.

Canadian Moat Stocks FAQ

Better Total Returns and Even Better Risk-Adjusted Returns

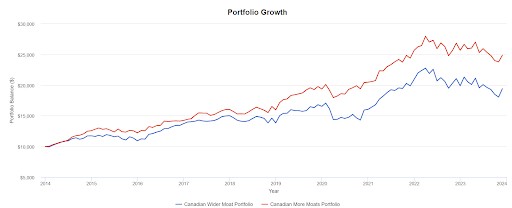

I’ve long suggested to readers that they consider the wider moat route. To be brutally honest, I wish I had eaten my own cooking a little earlier in the game on that one.

When I run the math, I find that there are better returns that have been offered with less volatility. That makes sense, as there are more sub-sectors to help with volatility and drawdowns in corrections. And while there are smaller dividends in the rails and grocers, there has been more dividend growth.

Certainly we give up some dividend yield by going the wider moat route, but the total returns would allow you to create even greater income in retirement by the combination of dividends and share harvesting.

And keep in mind that in retirement we would have to manage the sequence of returns risk. Here’s the performance of the “More Moats Portfolio” after we add in those grocers, railways and utilities. Perhaps I should have written, here’s the ‘outperformance’. It is substantial.

The More Moats also outperformed VDY and the TSX Composite. And the portfolio offers less volatility. Who doesn’t want greater returns with less risk?

Of course, this is a good time to add that past performance does not guarantee future returns. I like investing in Canadian moat stocks in our home market due to the strong oligopoly structures in place. It’s not great for consumers, but it’s tough to beat for risk-adjusted shareholder returns.

Is there a list of us stocks that would mirror this Canadian list of stocks?

Great article Dale, I hold your same 7 stocks and I love the total return on them yet i haven’t had the gut to pull the trigger on the low yield ones like CN or MRU , I know total return is the goal but I’m to addicted watching those juicy divis landing in my account monthly :)

For someone who doesn’t really want to spend the effort of maintaining a portfolio of individual stocks, is there an ETF that uses this approach?