Maxed out RRSP and TFSA – Now What?

I recently received an email from a reader with a bright financial future. They have a maxed out TFSA and has recently maxed out her RRSP as well. Here’s a snippet of the email below (edited for brevity).

First of all, thank you for sharing your wisdom and financial journey. I love reading your blog and I learn so much from it!

I was wondering if you could give some advice on where to put my money after maxing out my RRSP and TFSA contributions. I saw on MDJ that you like Canadian all-in-one ETFs, but in a taxable account, and with so many options out there, I’m getting quite overwhelmed.

I’ve also always done our taxes, and it has just basically been the T4s plus the basic deductions and RRSP contributions. I’m worried that after maxing out RRSPs and TFSAs, and now using a non-registered account, it will be a disaster come tax time. Would welcome any insight you have on this.

The first thing we should do for our anonymous emailer is applaud their very solid savings habits. When I wrote an online course about saving and investing for Canadian retirement, I found that while there was no official record of how many Canadians had maxed out RRSPs, plus maxed out TFSAs, I would estimate around 2% of all Canadians have maxed out both their RRSP and TFSA contributions. That’s accounting for maxing out past RRSP and TFSA contributions, as well as the additional room for the current tax year.

I get to that number by looking at recent CRA data that shows 8.9% of all TFSA holders max out their contribution room. Since only about half of all eligible Canadians have any TFSA at all, that means somewhere between 4% and 5% of all eligible Canadians have maxed out TFSAs.

When we look at maxed out RRSPs, there is even less overall data. We know that with the invention of the TFSA in 2009, overall RRSP contribution rates went down, as savers now had more options. Considering how much more RRSP contribution room Canadians have relative to TFSA room – and how many more years they’ve had to carry forward contribution space, I’d be willing to bet somewhere around 1-2% of Canadian adults have maxed out both their RRSP and TFSA.

So, our anonymous saver is in very elite company here, and if you haven’t maxed out your RRSP and TFSA then there is no reason to panic. That said, it should also be noted that without knowing more details such as if they have a defined benefit pension plan, her spousal situation, her income, housing situation, and future financial goals, it’s difficult to give specific advice.

Are You Saving Enough for Retirement?

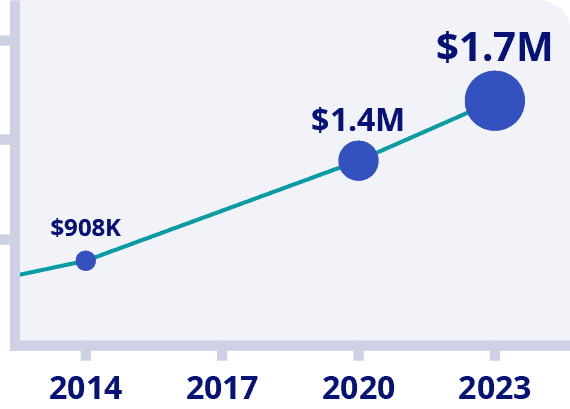

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Get $50 Discount With Promo Code MDJ50

*100% Money Back Guarantee

*Data Source: BMO Retirement Survey

What to Do After You Max Out RRSP and TFSA Accounts

Given that we don’t know all of our reader’s specifics, here’s a few common ideas (ranked in order of what would most likely help the average Canadian in average tax circumstances).

- If you are still eligible, definitely an FHSA should be your first priority!

- RESP contributions (What’s better than keeping investments under the tax-free umbrella – plus getting free money from the government for doing so?)

- Pay down your mortgage (if you have mortgage debt, paying it down offers a tax-free return, as opposed to investing outside of a registered account).

- Investing within your corporation (if you have one).

- Opening a non-registered investments account (I wrote an article about tax efficient ETFs for your non-registered portfolio).

- Donating to charity (you get a tax break and help people – after all, you’re doing pretty solidly if you and your spouse are both able to max out your TFSA and RRSP).

The Basics of RRSPs and TFSA and Taxation

For people new to investing, RRSP’s and TFSAs are a type of account, not an investment type. You buy investments to put in these accounts. These accounts allow investments to grow tax-free which means the investments do not need to be reported when you file for your taxes.

There are still major differences between the two accounts. RRSP deposits give you a tax deduction, but you will be taxed at your marginal rate when you withdraw. The main strategy around using an RRSP is to maximize your deposits when/if you are a high earner/highest tax bracket, and withdraw when you are in a lower tax bracket during retirement.

TFSA’s, on the other hand, do not give you a tax deduction on your deposits, but the account will let you withdraw from the account without reporting the income (ie. tax-free withdrawals). This can come as a big tax advantage for those with defined benefit pension or other retirees with higher base income. If the whole idea of TFSAs is a bit new to you, find out more about TFSAs here.

Should I Max Out TFSA or RRSP First?

I’ve written a long article on the specifics of the TFSA vs RRSP decision, but long story short – for most people – it honestly won’t matter much. If you’re earning more in your working years than you will be in retirement, then prioritize the RRSP.

Keep Your Tax Shelter Going

Back to the point of the article, RRSP’s and TFSA’s can be powerful wealth generators as it eliminates a big investment drag – taxes! The best move for most investors is to maximize tax-sheltered accounts before investing within non-registered, or taxable, accounts.

What if both the RRSP and TFSA are maxed out like in the reader’s case? It looks like the reader has done a great job with her savings to maximize her RRSP and her TFSA and looking to possibly invest the surplus cash flow. Judging by the email, they are also interested in keeping taxes as simple as possible.

To do that, I would suggest a couple of options before even considering investing within a non-registered/taxable account. To keep things as tax efficient as possible, I would look at other efficient ways to spend excess cash flow.

To start, an obvious one, pay down debt. If there is an existing mortgage or other debt, it would make sense at this point to take the extra cash flow to pay it down. Even though interest rates are relatively low right now, it’s a guaranteed after-tax return, and rates will likely be higher during renewal time. After all, one big milestone to achieve before retirement is to be 100% debt free.

Another option to consider if the reader has children is a registered education savings plan (RESP). This is another type of account that allows investments to grow tax-free. While there is no tax-refund for deposits, taxes are paid by the student (which should be low) when the funds are withdrawn for post-secondary education.

If all debt is paid off, and the RESP is maxed out and you still have extra cash flow – then it’s time to look at non-registered investments. That’s a big topic in itself, so let’s dig in a little.

Are You Saving Enough for Retirement?

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Get $50 Discount With Promo Code MDJ50

*100% Money Back Guarantee

*Data Source: BMO Retirement Survey

Portfolio Allocation

Let’s dig into the good stuff – investing! I like to configure my accounts as one big portfolio to help minimize taxation. If you are like the reader with both RRSP and TFSA maxed out and looking to invest, you may need to re-arrange your investments to fit the “one big portfolio”.

I use the following setup for maximum tax efficiency (see this article for more detail on setting up a tax-efficient portfolio):

Here is an example of an index investor with a simple portfolio that may consist of globally diversified index funds/ETFs, bonds, and cash.

RRSP:

- Fixed Income/Bonds/GIC’s

- Foreign Equities

- Income Trusts

- REITs

- Canadian Equities

TFSA

- Fixed Income/Bonds/GIC’s

- Income Trusts

- REITs

- Canadian Equities

- Foreign Equity (withholding tax on dividends will apply)*

Non-Registered:

- Canadian Equities (only if tax-sheltered accounts maxed out)

As you can see, it may make sense to pull all Canadian equities out of your tax-sheltered accounts and place in the new non-registered/taxable account due to the tax efficiency of Canadian dividends. You can read more about the tax efficiency of Canadian dividends here.

Fixed income and international dividends are taxed at 100% of your marginal rate (inefficient) which is why it makes sense to keep them tax sheltered.

Investment Ideas

I think that portfolios should be diversified across multiple geographic markets, and the easiest way to do this is via index ETFs.

If you are new to ETFs, I’ve been talking a lot about the all-in-one ETFs lately as the easiest way for an investor to set up a low-cost diversified portfolio.

It gets a little trickier to use all-in-one ETFs with the “one big portfolio” concept, preferably, you’d break it up into 3 ETFs instead. For example:

- TFSA: Bond Index (VAB), Canadian REITs (VRE) and/or other high yielding Canadian equities. If you have minimal RRSP space due to a defined benefit pension, you can put your ex-Canada holdings here as well.

- RRSP: US equity, International equity, and emerging markets (XAW)

- Non-Registered: Canadian Equity (XIC or VCN)

Another option, if you like to research and follow stocks on a regular basis, is to buy Canadian dividend stocks for your non-registered portfolio while using ETFs for your ex-Canada (ie. outside Canada) exposure. At least that’s what I do for the most part.

Here is a little more info on dividend investing:

- Top 22 dividend growth stocks in Canada

- How to build a dividend growth portfolio

- My favorite discount brokers

- Knowing when to buy dividend stocks

Using Horizon’s ETFs

For ultimate tax efficiency for the non-registered Canadian equity allocation, the reader read my article on the Horizon’s ETFs who have created index ETFs that pay 0% in distributions or dividends. Instead, you will only be taxed with capital gains tax when you sell down the road. The dividends are still there but used to compound instead of being paid out. Great deal right?

It was good while it lasted, but the last federal budget has indicated that the party is over. It hasn’t been determined how they will tax those “swap” ETFs, but there will be changes. Likely enough to make them not as attractive, which is why I would say to avoid these ETFs until there is more clarity.

Is Maxing Out My RRSP Enough for Retirement?

Maxing out your RRSP is probably enough for retirement – if you manage your RRSP to RRIF conversion correctly, and factor in your CPP and OAS payments as well.

Truthfully it’s difficult to answer this question without knowing more variables about your specific situation such as how much was your max RRSP each year you were working? Unlike the TFSA, the more you earned (up to a certain level) the more RRSP contribution room you would have received while working. You also have to strategically plan out your RRSP withdrawal strategy.

To know for sure whether your maxed out RRSP is enough for retirement – or whether your maxed out TFSA is enough for that matter – I recommend two paths.

1) I have created a self-paced online course for Canadians aged 35-70 looking to plan their own retirement. It’s called 4 Steps to a Worry-Free Retirement and it’s very user-friendly. I will personally answer any questions you have as you complete the course.

2) If you are looking for a more one-on-one solution, and want to work with Canada’s best financial advisory team, then I recommend checking out Objective Financial Planners by clicking here. Jason Heath is the founder of the company and he is routinely featured in Canada’s major news publications.

He is widely-trusted by thousands of Canadians as a fee-only, and advice-only planner. In other words, unlike most planners in Canada, Jason will never recommend a mutual fund with annual fees that pays him a kickback. Instead, you’ll get simple, easy-to-understand quote for the services you need.

2026 RRSP and TFSA Updates

It’s worth mentioning that RRSP and TFSA contribution limits get adjusted every year. They’re adjusted over time, largely based on inflation and income growth. That means higher limits tend to go up quicker after periods where prices (and wages) have moved higher.

That’s exactly what we’ve seen over the past few years.

For 2026, the TFSA contribution limit remains $7,000. That means we’ve now had three straight years at the $7,000 level, following the jump from $6,500 back in 2023. If you were 18-or-older in 2009 and have never contributed, your total TFSA contribution room rises to $109,000 in 2026.

That’s a lot of tax-free space!

On the RRSP side, the maximum contribution limit for 2026 increases to $33,810, or 18% of your earned income, whichever is less. That’s another step up from recent years, and it reflects how RRSP limits tend to ratchet higher over time as incomes rise.

Of course, your personal RRSP room can be higher or lower depending on past contributions and any pension adjustments, which is why checking your CRA account or Notice of Assessment is always the safest move. Back in 2012 Statistics Canada determined Canadians had about $633 billion in unused RRSP contribution room available to them. Fourteen years later, I bet that number has more than doubled.

The key thing to remember with both plans is that unused room carries forward indefinitely. If you didn’t have the cash flow to contribute in your 20s or 30s (which describes most people), that room doesn’t disappear. It stacks up.

FHSA vs RRSP and TFSA

There aren’t a lot of Canadians out there who would be in the fortunate position of having maxed out their TFSA and RRSP – but are still looking to buy their first home.

That said, if this describes you, then maxing out your FHSA is an absolute no-brainer. Even if you don’t intend to eventually buy a house, the FHSA account is like a backdoor RRSP contribution. It’s key to understand that even if you don’t have any more RRSP contribution room, you can eventually roll your FHSA cash into an RRSP anyway! It’s like a magical RRSP contribution room just fell from the sky.

Here’s what the First Home Savings Account offers Canadians:

- Ability to shelter up to $40,000 (lifetime max) from the tax man.

- You have an annual $8,000 contribution limit.

- You can combine your limit with a partner’s limit to save up to $80,000 when buying a home in Canada for the first time.

- Best of both worlds: You get the RRSP tax refund, plus the TFSA “no taxes on the way out” combination!

- Your money can be invested within the account – earning more down payment cash for you as you add to it and progress on the house-buying journey..

- You get 15 years from when you first open your FHSA to when you have to use it – or else it gets rolled into your RRSP.

When you combine the immediate tax break that is similar to an RRSP, with the ability to pull cash out to buy a home tax-free (like a TFSA), you get an unbeatable combination. Check out my First Home Savings Account (FHSA) article for more details on this unique account that the government opened up in 2023.

Maxed Out TFSA and RRSP FAQ

Final Thoughts

Very few Canadians ever reach the point where both they are able to max out their TFSA and RRSP for a given year – nevermind fully maxed out lifetime contribution limits!

It’s not because they don’t understand the benefits, but because life has a way of competing for cash flow. Housing costs, kids, job changes, market nerves, higher inflation, and long stretches where saving feels optional rather than urgent all contribute to meagre savings ability.

So if you do find yourself in that position, it’s worth pausing for a moment. It usually means you’ve combined time, consistency, and restraint – not perfect timing or clever tricks. You’ve taken advantage of Canada’s most generous tax shelters year after year, and you’ve given compounding room to do its thing. That alone puts you well ahead of the median Canadian household. If you aren’t yet one of this fortunate few, then remember that there is always room to catch up!

Once registered accounts are full, the low-hanging tax fruit has been picked so to speak. It’s not about figuring out other ways to reduce your tax bill and shelter as much of your investment’s potential as possible.

The bigger takeaway is this: maxing out your TFSA and RRSP isn’t the finish line. It’s a sign that your system is working. From there, progress looks less dramatic, more personalized, and a lot more boring than most financial headlines suggest.

If you see the end of your career approaching, then you might be switching from a TFSA/RRSP accumulation mindset to more of a decumulation strategy. You can really save a lot of money by planning your RRSP meltdown correctly, and saving your TFSA to use as your break-in-case-of-emergency asset. I explain it all here in the online course I created called: 4 Steps to a Worry-Free Retirement.

How is ZSDB or ZDB for the fixed income portion of taxable accounts?

What if you’re new to non-registered investments (ie, have money to invest in a non-registered account) but don’t want to add additional Canadian equity exposure since you feel like you’ve got enough exposure to Canada within existing RRSPs/TFSA portfolios?

I would just look at a non-Canadian ETF Marilyne. Maybe VXC?

Is the statement from your article (below) indicating that it would beneficial tax-wise to move individual Cdn stocks in-kind from TFSA (or RRSP) to non-registered accounts? That way one could benefit from the tax advantages of Cdn dividend paying stocks? Although I’m thinking moving things out of RRSP account would have tax consequences.

As you can see, it may make sense to pull all Canadian equities out of your tax-sheltered accounts and place in the new non-registered/taxable account due to the tax efficiency of Canadian dividends

You have only a few more days to withdraw from your TFSA this year so the contribution room resets in 2026.

But not sure why you would do this. The TFSA’s tax shelter is optimal for equity growth. You will never pay any tax on the capital gains or dividends.

Have you ever reviewed or considered the value of creating a retirement compensation arrangement?

what is the best way to invest US dollars if RRSP and TFSA are maxed out?

You’d likely want to look into a USD non-registered account with your brokerage Lila.

If renting, also consider maxing out ($8k per year) on a First Home Savings Account for tax-free investment growth – one for you and one for spousal partner.

Actually, maxing out RRSP is not necessary a good thing. I am carrying a large contribution room from my younger days and find it handy that I can now get almost 50% tax deduction. Needless to say that my contributions now exceed the annual max due to carried room.

My plan is to still carry some room towards retirement. My company recently offered a buyout. Those without RRSP room have to pay 53% to CRA.

I put into my RDSP, I am disabled and have the Disability Tax Credit.

Absolutely a solid use of the account Jason. Good on you.

I didn’t see anything regarding swap ETFs in the latest federal budget. Do you have a reference/info you can share?

Thankfully there are no new changes for this year Chris. There was just rumblings (it seems there always are off and on) that they’ll target these type of ETFs.

Regarding the non-registered accounts investments in foreign stocks, can you provide more details or write an article about different type of taxation? Ex: stocks without dividend, stocks with dividends, CDRs with or without dividends (CIBC CDRs), ETFs following USA/S&P500 market…

Informative, thanks! Is it best to open separate accounts or joint accounts with your spouse? I imagine there are tax implications either way.

Hi Trev, for RRSPs and TFSAs, you can only open individual accounts. However, you can assign benficiaries to each of those accounts. More info here:

https://milliondollarjourney.com/what-happens-to-your-rrsp-and-tfsa-after-you-die.htm

Thanks FT. I should’ve clarified, for non-registered accounts, is it best to open separate accounts or joint accounts with your spouse? I’ve heard the non-registered can be a joint account.

Hi Trev, yes open a joint account for a non-registered account. One big benefit is that if one of you pass away, the other assumes ownership. However, if you plan on the lower-income spouse declaring the dividends/capital gains for tax purposes, make sure you show a clear paper trail showing that the lower-income spouse contributed the money to the account.