Is Rogers Stock A Good Buy in 2026?

If you’re considering investing in Rogers stock in 2026, it is important to understand the company’s performance, dividend growth, as well as its recent merger with Shaw. Staying informed about Rogers’ recent advancements and industry developments is crucial in determining whether it is a wise investment choice in 2026. This also allows you as an investor to compare it with its fellow Canadian telecommunication competitors, BCE and Telus.

If you’re looking to diversify your portfolio with more dividend stocks, we recommend exploring our article on Top Canadian Dividend Stocks. This valuable resource offers insights into reputable Canadian companies known for their consistent dividend growth, including those in the telecommunications sector like Rogers. The telecom giant has established a reputation for its consistent dividend payments over the years, making it an appealing option for investors seeking stable income.

Want To Buy Rogers Shares? Price, Performance & Analysis

- RCI.A.TO Stock Price: 52.35

- Dividend Yield: 3.83%

- Price-to-Earnings (P/E) Ratio: 17.70

- 5yr Earnings Per Share Growth: -4.49%

- 5yr Dividend Growth: 0.82%

- Payout Ratio: 60.12%

Our Rogers Stock Analysis

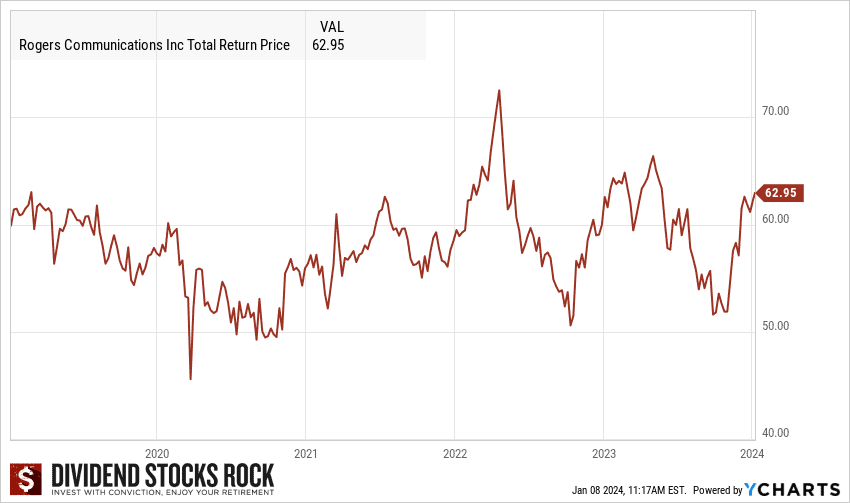

- Despite the merger announcement, the stock has gone down slightly.

- It is currently still well below the pre-covid price level, indicating a potential buying opportunity.

- Dividend yield is moderate at 3.3%, Canadian competitors are higher.

- Holds diversified investments in wireless, cable, media, and sports.

Rogers appears to be an appropriately valued stock at its current share price of $60. Although it is still below the pre-COVID price level, this could present a potential buying opportunity for investors.

Our analysis indicates that Rogers is an attractive option for long-term investment as the company retains a prominent position in the market. Rogers also is committed to dividend payouts (although maybe not as committed to growing those payouts as their competitors at BCE and Telus but a consistent income nonetheless).

Check out our guide on the Best Long-Term Investments in Canada if you are looking to invest long term in Canada.

How Can I Buy Rogers Shares Right Now?

To purchase Rogers shares, you can use any of the available Canadian online brokerage services. At MDJ, we prioritize guiding our readers in selecting discount brokerages that align with their needs. Our list of Top Online Brokerages in Canada is regularly updated to provide our readers with the best recommendations and current promotional offer codes.

Once you have successfully registered for an online brokerage account, buying Rogers shares is a simple process. Use the search bar to find the ticker symbol “RCI.A” or “RCI.B” and determine the number of shares you wish to purchase.

For instance, if you plan to invest $450 in Rogers shares and the current stock price is $45, you would enter “10” and select the “market limit” option. The online brokerage platform will present you with a confirmation prompt: “Do you want to buy 10 shares of RCI.A/RCI.B at $45 each, totaling $45?”

Once you confirm the order, the online broker will handle the necessary transactions. Congratulations! You are now a shareholder of one of the leading telecommunications companies in Canada.

Best 2026 Broker Promo

Up To $2,000 Cash Back + Unlimited Free Trades

Open an account with Qtrade and get the best broker promo in Canada: $100 when you invest $1,000!

The offer is time limited - get it by clicking below.

Must deposit/transfer at least $1,000 in assets within 60 days. Applies to new clients who open a new Qtrade account by July 31, 2026. Qtrade promo 2026: CLICK FOR MORE DETAILS.

Rogers Stock Past Performance

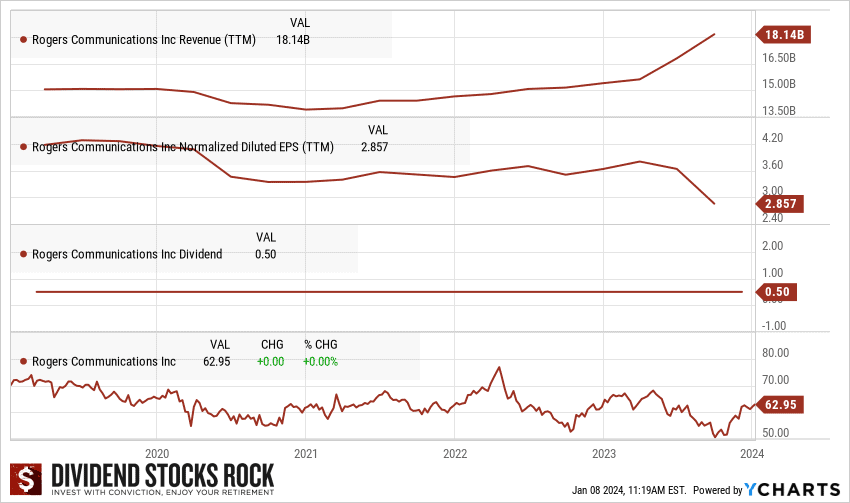

Over the past four years, Rogers Communications has paid out consistent dividends, even when its revenues and earnings did not align with those payout levels, and was falling at times. This demonstrates two important aspects:

First, Rogers is committed to rewarding its shareholders with dividends, regardless of its current earnings potential.

Second, it highlights the company’s dominance in the telecommunications sector, given its long history of free cash flow.

Rogers faced a decline in earnings in 2020, primarily due to the impact of the pandemic and prevailing market conditions during that period. However, the company has since displayed signs of recovery and is poised for future revenue growth, as depicted in the provided chart.

More recently, Rogers Communications announced voluntary departure packages for select employees as part of the integration process following its acquisition of Shaw Communications. This proactive step highlights Rogers’ commitment to addressing workforce challenges and implementing strategies to reduce cost, without completely destroying worker morale.

As an investor, these developments instill confidence in Rogers’ management team and their ability to navigate evolving conditions. This positions the company favorably for potential continued dividend payments.

As a long-term investor, I prioritize investments that offer both growing dividends and steady capital gains. Rogers, unfortunately, has not demonstrated a significant dividend growth rate in recent years, as the company’s dividends have remained consistent.

However, this consistency can be viewed as a positive sign, indicating that Rogers’ management is prioritizing stability and maintaining a reliable dividend payout, while at the same time pulling the funds together to be proactive in the acquisition space.

While dividend growth may not be as pronounced as in other companies, Rogers’ focus on maintaining consistent dividends can still be appealing to income-oriented investors seeking reliable income streams. Additionally, the company’s potential for steady capital gains should not be overlooked, as Rogers operates in the telecommunications sector, which continues to experience growth and offers opportunities for long-term value appreciation.

As an avid dividend investor, I highly recommend consulting the Dividend Stocks Rock (DSR) Guide. Whenever I am looking for a comprehensive analysis and comparison of dividend stocks this resource offers valuable insights and allows me to make informed decisions about my investments.

Rogers Stock Forecast

Rogers Communications reported a net income of $378 million in the first quarter of 2023, representing an increase compared to the same quarter last year. This positive trend makes Rogers stock an attractive choice for investors looking for long-term opportunities in the telecommunications industry. One key factor contributing to Rogers’ appeal is its position as the leading player within the Canadian telecom sector, known for its profitable oligopoly structure.

In comparison, Bell is another major player in the Canadian telecommunications industry, offering similar services and competing for market share. Both Rogers and Bell have a significant presence and a large customer base in the country. One of the key factors to consider when choosing between the two companies is their respective market shares. As of now, Rogers holds a slight edge with a market share of 31.6%, while Bell follows closely with its own substantial share.

When comparing Bell (BCE) and Rogers Communications, both companies offer a range of services, including media outlets and interests in professional sports teams. The company provides a quarterly dividend with a yield of around 3% and has shifted its focus to longer-term strategic objectives, investing in growth initiatives and reducing debt. Additionally, Rogers has pursued a $20 billion deal to acquire Shaw Communications, which is expected to bring significant cost synergies and long-term growth potential.

On the other hand, BCE (Bell) also operates a considerable media arm, and its longstanding track record of paying dividends makes it appealing for income and defensive investors. With a high dividend yield of 6.8%, BCE offers one of the highest-paying dividends on the market.

The company saw robust growth in wireless and retail internet activations this year, with retail internet net activations reaching a 16-year high earlier this year. Despite trading down nearly 5% over the trailing 12-month period, BCE’s current valuation could be considered favorable for long-term investors.

For more wide moat stocks like Bell and Rogers, check out our guide on the Best Wide Moat Stocks in Canada.

In conclusion, the choice between Bell and Rogers depends on the investor’s preference for income potential (BCE’s high dividend yield) or growth prospects (Rogers’ strategic initiatives and potential merger with Shaw Communications). Both companies offer similar services and dividends and could be valuable additions to a well-diversified portfolio.

If you’re interested in exploring more investment opportunities within the Canadian telecommunications sector, I recommend referring to our guide on the Best Telecommunications Stocks in Canada. This guide offers valuable analysis of the sector and highlights key players in the industry, providing insights to help inform your investment decisions.

Upon completion of the merger between Shaw and Rogers, shareholders of Rogers can benefit from a sector with even fewer competitors. This consolidation allows Rogers to leverage its existing customer base and solidify its market presence. Currently, the market is divided almost equally among the three major players, with Rogers holding a slight edge in terms of market share at 31.6%.

For Rogers shareholders, this translates to a more stable pricing environment, which can result in improved margins and profitability. With high barriers to entry, and no appetite on the part of the Canadian government to allow foreign competitors, these improved profit margins shouldn’t suffer from much consumer pressure.

If you prefer a passive investing approach and want to mitigate risk by investing in ETFs rather than choosing individual stocks, we suggest looking at our list of the Best ETFs in Canada for 2026. These ETF options offer diversified exposure to various sectors and asset classes, allowing you to benefit from broader market performance and potentially reduce risk in your investment portfolio.