Rebalance My Investment Portfolio: How, Why, and When

With all of the recent volatility in the stock market, I’ve been getting a lot of inquiries about rebalancing investment portfolios.

Other inquiries have read something along the lines of: “This is all crazy, should I sell everything?!!”

You almost assuredly shouldn’t “sell everything,” but when I wrote about the Canada-USA Trade War back at the start of February I said that the bad news had largely been baked into Canadian stock market prices. I also said that if you were already feeling quite stressed, it was a great time to reassess your overall risk profile – and then see if your asset allocation matched what your risk profile was willing to accept. That turned out to be a pretty good call.

Selling during a stock market panic is an awful idea – and it’s also depressingly common. In order to prevent that outcome, establishing your asset allocation strategy – and then sticking to it by rebalancing your investment portfolio periodically – is a common sense move.

This is perhaps most easily done by either using one or Canada’s robo advisors to manage your asset allocation for you (they automatically rebalance), or by opening a Canadian online brokerage and buying units of the best all in one ETFs on the Toronto Stock Exchange. That said, you can save a few bucks by rebalancing your own portfolio.

What is Portfolio Rebalancing?

At its core, rebalancing your portfolio is about realigning your investments with your original target allocation.

“Original target allocation” just means: The group of investments that you started with. It includes all the investments in your RRSP, TFSA, FHSA, RESP, non-registered accounts, etc.

That original target allocation should be representative of your risk tolerance. I actually created my own risk tolerance questionnaire as part of my DIY financial planning course: 4 Steps to a Worry-Free Retirement, but you can find less user-friendly ones all over the internet. I would greatly encourage you not to skip this step, as a lot of people don’t accurately understand their risk tolerance until it’s too late!

Ok, so let’s say you started off with a simple portfolio that was 60% stocks and 40% bonds. But after a couple of years of strong equity returns (or a bond market crash), that mix might be looking more like 75% stocks/25% bonds.

That’s a problem.

Even if you haven’t touched your portfolio, market movements alone can change your risk profile – which means you could be taking on way more risk than you originally signed up for. Rebalancing is the process of selling some assets that have grown beyond your target allocation and buying others that have fallen behind.

Usually we refer to rebalancing our investments in the context of stocks and bonds (aka: equities to fixed income). But it can also refer to the relationship between smaller parts of the portfolio – such as the mix of Canadian to US or international equities.

Are You Saving Enough for Retirement?

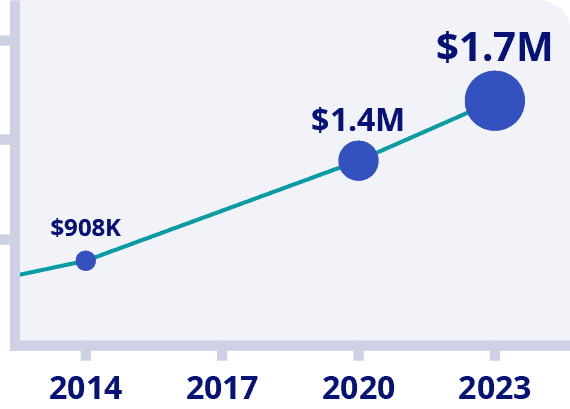

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Get $50 Discount With Promo Code MDJ50

*100% Money Back Guarantee

*Data Source: BMO Retirement Survey

Why is Rebalancing Important?

Rebalancing is important for three main reasons (which are somewhat interrelated).

1) Keeps Your Risk Profile Consistent

The biggest reason to rebalance is that your risk tolerance is unlikely to change dramatically year to year, but your portfolio will shift on its own if left unchecked.

“Letting your winners run” (as the business guys on TV say) can be tempting, but it’s basically drifting into a riskier portfolio without consciously choosing to take on that added risk. That might be fine for a given moment, but when the market inevitably corrects, it’ll feel like the rug just got pulled out from under you.

Rebalancing pulls you back to the risk level you originally signed up for – and makes sure your portfolio doesn’t quietly morph into something way off course.

2) Encourages a Disciplined, Rules-Based Approach

There are few things more dangerous to long-term investing success than emotion and overconfidence.

Rebalancing helps you limit the damage of each.

In fact, there’s a mountain of behavioural research out there showing that investors underperform their own investments simply because they tinker too much – especially when headlines get scary. You’re far more likely to succeed when your investing decisions are based on rules-based processes – not hunches.

Rebalancing is a systemic approach that stops you from chasing heat and bailing on cold sectors at the worst possible time.

3) It’s a Built-In “Buy Low, Sell High” Strategy

Rebalancing forces you to do what no one wants to do – sell the stuff that’s been doing well, and buy the stuff that’s been struggling. That can feel completely backwards in the moment.

But it works.

By trimming back your outperformers and adding to your laggards, you’re executing a strategy that’s mathematically proven to improve long-term risk-adjusted returns. That doesn’t mean you’ll always make more money. But it does mean you’re more likely to reduce volatility while keeping returns on target.

And that’s not just theoretical – there are studies from Vanguard, Morningstar, and others that show this clearly.

Mechanics of Asset Rebalancing

Let’s say you’ve built yourself a nice, balanced ETF portfolio using Canadian-listed funds. Maybe it looks something like this:

- 40% Stocks – Canada: Vanguard FTSE Canada All Cap Index ETF (VCN)

- 30% Stocks – USA: Vanguard S&P 500 Index ETF (VFV)

- 10% Stocks – International: iShares Core MSCI EAFE IMI Index ETF (XEF)

- 20% Bonds: BMO Aggregate Bond Index ETF (ZAG)

Here’s what that looks like in dollars:

| ETF | Ticker | Target Allocation | Dollar Value |

| Canada Stocks | VCN | 40% | $40,000 |

| US Stocks | VFV | 30% | $30,000 |

| International Stocks | XEF | 10% | $10,000 |

| Bonds | ZAG | 20% | $20,000 |

| Total | 100% | $100,000 |

Now let’s fast forward 12 months.

Over the past year:

- US stocks (VFV) had a big rally: +20%

- Canadian stocks (VCN) were flat: 0%

- International stocks (XEF) dipped slightly: -5%

- Bonds (ZAG) went sideways: 0%

Here’s what your portfolio looks like now:

| ETF | Ticker | Target Allocation | Dollar Value |

| Canada Stocks | VCN | 40% | $40,000 |

| US Stocks | VFV | 30% | $36,000 |

| International Stocks | XEF | 10% | $9,500 |

| Bonds | ZAG | 20% | $20,000 |

| Total | 100% | $105,500 |

Because we now have more money, our overall balances in each category will be higher than before after we rebalance. Here’s what we have to do to get back to our target asset allocation percentages.

| ETF | Current Value | Target Value | Action |

| VCN | $40,000 | $42,200 | Buy $2,200 |

| VFV | $36,000 | $31,650 | Sell $4,350 |

| XEF | $9,500 | $10,550 | Buy $1,050 |

| ZAG | $20,000 | $21,100 | Buy $1,100 |

Methods of Rebalancing

When it comes to rebalancing your investment portfolio, there’s no silver bullet. It’s really about choosing what process-based approach you feel most confident in adhering to over the long term.

Let’s take a look at the two most popular strategies: time-based rebalancing and threshold-based rebalancing, along with a hybrid option that some Canadian investors might prefer.

Time-Based Rebalancing

This method involves reviewing and rebalancing your portfolio at regular intervals (usually once a year, semi-annually, or quarterly).

On a set date (say, every January 1st or July 1st), you check your portfolio against your target allocations.

If your current asset mix has drifted significantly, you rebalance by selling some of the overweight assets and buying the underweight ones. Just like we did in the rebalancing example above.

Pros:

- Simple to implement – especially if you set a recurring calendar reminder.

- Avoids constant tinkering and emotional investing decisions.

- Easy to automate within a robo advisor or online brokerage that allows scheduled investing (Justwealth and Wealthsimple both do this well).

Cons:

- May trigger unnecessary trades when markets are relatively stable.

- Doesn’t respond in real-time to fast-moving markets.

Threshold-Based Rebalancing

Also called “tolerance-band” rebalancing, this approach triggers trades only when an asset class deviates a set amount from its target allocation – typically 5%.

You monitor your portfolio, and only rebalance when an asset class drifts beyond its acceptable band. For example, if your Canadian equity target is 40%, and your threshold is ±5%, then you rebalance if VCN falls below 35% or rises above 45%.

Pros:

- Reduces unnecessary trading and potential capital gains in taxable accounts.

- More responsive to real changes in market conditions and risk exposure.

- Has historically shown slightly better risk-adjusted returns compared to time-based rebalancing.

Cons:

- Requires more frequent monitoring or use of automated tools.

- May still result in frequent trading during volatile markets.

Hybrid Rebalancing: The Best of Both Worlds?

A blended approach is what many DIY Canadian investors end up using in practice – checking in once or twice a year, but only triggering trades when an asset class deviates beyond a certain threshold.

For example: You might review your portfolio every January and July. You would then only bother with rebalancing if something is off by more than 5%.

This strategy provides structure without being too hands-on – and may help reduce costs and taxes in the long run.

Rebalancing With New Contributions

Honestly, much of the time you never have to bother selling anything if you are still in the accumulation phase of your life. All you have to do is add your new money to the assets that have done the worst, and you can bring your overall portfolio back into balance without worrying about selling and triggering capital gains taxes.

Here’s an example.

Let’s say your investment strategy uses a classic three-ETF model portfolio, and your target allocation is VCN 30%, VFV 45%, and ZAG 25%. During the year our U.S. equity exposure is a bit heavy (thanks, Nvidia…), and your bond allocation has taken a hit due to rising interest rates. Now, our portfolio looks like this:

| ETF | Current Value | Current % | Target % | Difference |

| VCN | $31,000 | 31% | 30% | +1% |

| VFV | $50,000 | 50% | 45% | +5% |

| ZAG | $19,000 | 19% | 25% | -6% |

| Total | $100,000 | 100% | 100% |

If we had $10,000 to invest for the year, we wouldn’t have to worry about selling VFV and buying more VCN and ZAG. Instead, we calculate what 30% of $110,000 is (our new overall portfolio balance) and from there, we can say that we should have $33,000-worth of VCN in our portfolio. Consequently, if we use our new portfolio to buy $2,000 of VCN, and $8,000 worth of ZAG, that gives us a rebalanced portfolio that looks like this:

| ETF | Current Value |

| VCN | $33,000 |

| VFV | $50,000 |

| ZAG | $27,000 |

| Total | $110,000 |

In reality, this is how rebalancing is done for most investors in Canada, since the vast majority of us aren’t dealing with massive portfolios.

Rebalancing Individual Stocks

Unlike ETF portfolios that rebalance around broad market indexes (often buying thousands of companies in one fell swoop) a portfolio of individual equities (such as Canadian dividend stocks) requires you to manually track sector diversification, company-specific risks, and valuation skews over time.

The principle of having a target allocation, and then buying-more-of-whatever-did-the-worst is still the same. The difference is that it’s usually substantially more complicated because you’re dealing with 10-30+ stocks.

Here’s a Canadian stock rebalancing example in its most basic form. Note that I’m NOT advocating for a stock portfolio that is made up of only five Canadian stocks! (Even if they are stocks that appear on our Canadian Dividend Kings list.)

If this was our initial target allocation of $100,000:

| Stock | Sector | Target Allocation | Initial Investment |

| TD | Financials | 20% | $20,000 |

| ENB | Energy | 20% | $20,000 |

| BCE | Telecom | 20% | $20,000 |

| CNQ | Energy | 20% | $20,000 |

| CNR | Industrials | 20% | $20,000 |

| Total | 100% | $100,000 |

And then we had a year where oil prices were high and the telecoms weren’t as profitable, it might now look like this (note the 15% overall gain in our portfolio):

| Stock | Current Value | % Of Portfolio |

| TD | $21,500 | 19.1% |

| ENB | $28,000 | 24.9% |

| BCE | $15,000 | 13.3% |

| CNQ | $26,000 | 23.1% |

| CNR | $24,500 | 21.8% |

| Total | $115,000 | 100% |

If we had no new money to invest, we’d have to sell some Enbridge, CNR, and CNQ to buy some more shares of TD and BCE. It would like this:

| Stock | Current Value | Target Value | Rebalancing Action |

| TD | $21,500 | $23,000 | Buy $1,500 |

| ENB | $28,000 | $23,000 | Sell $5,000 |

| BCE | $15,000 | $23,000 | Buy $8,000 |

| CNQ | $26,000 | $23,000 | Sell $3,000 |

| CNR | $24,500 | $23,000 | Sell $1,500 |

Tax Implications of Rebalancing In Canada

One of the biggest reasons investors hesitate to rebalance their portfolios – especially outside of registered accounts – is taxes. And they’re right to be cautious. Making moves for the sake of “perfect allocation” without understanding the capital gains hit you might take could lead to a costly surprise come tax time.

The good news is that this really only applies to the part of your portfolio that is non-sheltered from the tax man in a non-registered account. Within your RRSP, TFSA, RESP, FHSA, you can rebalance without worrying about tax implications.

But non-registered accounts are different. When you sell an asset (stock, ETF, mutual fund, etc.) in a non-registered account, you may realize a capital gain (or loss). Canadian rules for taxing capital gains are:

- Only 50% of the capital gain is taxable.

- The gain is calculated as the difference between the sale price and your adjusted cost base (ACB), minus any transaction costs.

So, if you bought $10,000 worth of CNQ and sold it later for $12,000, you’ve got a $2,000 capital gain. Half of that ($1,000) gets added to your taxable income for the year.

You’ll still come out ahead in most cases (because gains are good!), but if you’re expecting a big income bump that year, it can cause some nasty tax drag – or even mess with your OAS eligibility if you’re in retirement. Check out our article on taxes on capital gains and dividends for more information.

Note that if you rebalance using only new additions to your portfolio, you can avoid these tax implications for rebalancing.

Rebalancing Canadian Investments Q/A

Final Thoughts On Rebalancing An Investment Portfolio

Rebalancing isn’t about chasing returns – it’s about staying disciplined and making sure your investments still reflect your goals and risk tolerance. Whether you’re using ETFs, individual stocks, or a mix of both, setting up a simple system for rebalancing can help take emotion out of the equation and keep your long-term plan on track.

If you’re comfortable managing your own portfolio, the mechanics of rebalancing are straightforward. But if you’d rather not dive into the math – or if your finances have a lot of moving parts – this is exactly where a Canadian financial advisor can really shine.

They can help you create a rebalancing strategy that’s tax-efficient, easy to maintain, and customized to your life.

At the end of the day, the most important takeaway here isn’t when or how often you rebalance – it’s that you actually execute your strategy over the long-term (your whole life)!

Best 2026 Broker Promo

Up To $2,000 Cash Back + Unlimited Free Trades

Open an account with Qtrade and get the best broker promo in Canada: $100 when you invest $1,000!

The offer is time limited - get it by clicking below.

Must deposit/transfer at least $1,000 in assets within 60 days. Applies to new clients who open a new Qtrade account by July 31, 2026. Qtrade promo 2026: CLICK FOR MORE DETAILS.

In the “Rebalancing With New Contributions” section, the second table doesn’t add up. The total should be $110,000. This isn’t a big error or anything but probably worth correcting as it may lead to confusion for some readers.

Got it – nice catch Phil!