Net Worth Update March 2014 (+0.71%)

Welcome to the Million Dollar Journey March 2014 Net Worth Update. For those of you new to Million Dollar Journey, a monthly net worth update is typically posted near the end of the month (or beginning of the next) to track the progress of my journey to one million in net worth, hopefully by the time I’m 35 years old (end of 2014 – yes this year!). If you would like to follow my journey, you can get my updates sent directly to your email, via twitter (where I have been more active lately) and/or you can sign up for the MDJ Newsletter.

While the bulls took over the stock market in February, the markets took a bit of a break in March but did not remain far off all time highs. As of March 31 (before open), including dividend, the S&P500 squeaked out a 0.9% gain (via SPY). The TSX (via XIU.TO) and the MSCI EAFE (via XIN.TO) also moved up with a 1.35% and 1.03% gain respectively (including dividends).

How did my portfolio do this month? As I’ve been cleaning up my RRSP to contain mostly US and foreign equities, it is starting to track the US market a bit better where our combined RRSPs returned +0.95% (mostly US stocks and international). Our leveraged Canadian dividend portfolio organically gained 1.64% (ie. no cash transfers into the account) and managed to keep ahead of the Canadian index by a slight margin. The corporate investment account sat in cash this month and will remain so until I find some value opportunities.

In the big picture, for the March 2014 update we are up 0.71% for the month and 16.35% for the year thus far. We are up to $1,188,385 in assets for a total of $962k in total net worth. With the deadline looming, there is about $38k left to go until the big $1,000,000 financial milestone!

On to the net worth numbers:

Assets: $1,188,385 (+0.68%)

- Cash: $4,500 (+0.00%)

- Savings: $20,000 (+0.00%)

- Registered/Retirement Investment Accounts (RRSP): $180,700 (+0.95%)

- Tax Free Savings Accounts (TFSA): $64,000 (+0.79%)

- Defined Benefit Pension: $48,400 (+0.62%)

- Non-Registered Investment Accounts: $197,000 (+1.55%)

- Smith Manoeuvre Investment Account: $155,000 (+1.64%)

- Corporate Investment Account: $200,000 (+0.00%)

- Principal Residence: $318,785 (+0.00%) (purchase price adjusted for inflation annually)

Liabilities: $225,850 (+0.56%)

- Principal Residence Mortgage (readvanceable): $0 (0.00%) (Paid off in 2010!)

- Investment LOC balance: $118,300 (+0.25%)

- Future Tax Liability: $107,550 (+0.89%)

Total Net Worth: ~$962,535 (+0.71%)

- Started 2014 with Net Worth: $827,300

- Year to Date Gain/Loss: +16.35%

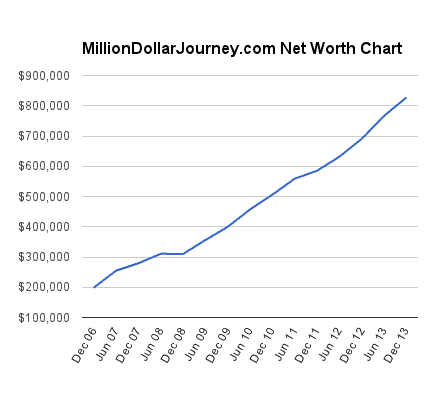

Readers suggested to chart my net worth progress over time. Below are the net worth values since Dec 2006 with data points taken semi annually.

- December 2006: $198,500

- June 2007: $254,695

- December 2007: $279,300

- June 2008: $310,483

- December 2008: $309,950 (rough second half)

- June 2009: $355,850

- December 2009: $399,600

- June 2010: $456,910

- December 2010: $505,800

- June 2011: $558,713

- December 2011: $585,228

- June 2012: $631,400

- December 2012: $690,400

- June 2013: $766,300

- December 2013: $827,300

Some quick notes and explanations to net worth questions I get often:

The Cash

The $4,500 cash are held in chequing accounts to meet the minimum balance so that we pay no fees (accounting for regular bill payments – ie. our credit card bill). Yes, we do hold no fee accounts also, but I find value in having an account with a full service bank as the relationship with a banker has proven useful.

Savings

Our savings accounts are held with PC Financial and ING Direct. We usually hold a fair bit of cash in case “something” comes up. The “something” can be anything that requires cash such as an investment opportunity that requires quick cash or maybe an emergency car/home repair. We also need cash to cover any future tax liabilities.

Where Does the Savings Come From?

We don’t live a lavish lifestyle (how we save money), and we do not carry a mortgage or any other bad debt. The only debt we have is an investment loan (which pays for itself), so we end up pocketing a majority of our earnings. Our earnings come from salaries, private business income (via dividends to shareholders), and eligible dividends from publicly traded companies.

Real Estate

Our real estate holdings consist of a primary residence and REITs plus a rental property. The value of the principal residence remains valued at the purchase price (+inflation) despite significant appreciation in the local real estate market.

Pension

The pension amount listed above is the value of both of our defined benefit pension plans. I basically take the semi annual statement and add the contribution amounts (not including employer matching) on a monthly basis. The commuted value of the pensions are not included in the statements as they are difficult to estimate.

Updated 2013 – My wife has recently changed her job position which has resulted in switching from a defined benefit plan to a defined contribution plan. This amount will be added to the RRSP totals going forward.

Stock Broker Accounts

Another common question is which discount broker do I use? We actually have accounts with multiple institutions. I’m hoping to reduce the number of accounts that we hold in the near future. Here is a review of some of the more popular online stock brokers.

Great job on your journey to $1mil! It looks like you are on pace to reach your Million Dollar Journey sometime this year. Congrats in advance!

Also, congrats on paying of the mortgage in 2010. Have you notice the difference in your ability to build your assets since paying of your mortgage? That is definitely one of the higher priorities for our family.

It’s a very good topic. Most people simply don’t factor in all the when comes to buying and selling their house. I had friends who said they made … on their house after selling their home which they owned for 7 years. But their not factoring in all the costs you mentioned plus renovations etc.

@FT

Thanks for your reply. All my RRSP outside my company contribution is in USD too. I did take advantage of the dollar at parity. I am about to transfer $50K from my other RRSP to my dividend account and I am not sure about buying US due to the dollar value …

Well done on the progress! I though I was catching up to you last year but you just took off and left me in the dust. I just reached $800K net worth this month.

Did you buy all your US investments before the drop in CDN dollar?

What is your TFSA invested in? I would expect it to be higher for covering both spouses.

@Passive, congrats on hitting the $800k milestone! In terms of USD, I do not really pay much attention to the FX rate, I just buy when valuations are attractive. Although, I must say that I’ve build most of my USD portfolio with the FX rate nearish par. The TFSA unfortunately sat in cash up until recently where we added some REITs. As REITS are still depressed, I suspect that the balances will remain low. Slow and steady!

@Francois, FT wrote “Tax Free Savings Accounts ” , so I understand that he’s talking about 2 TFSAs, his and his spouse

Yes, the TFSA balance is for two TFSAs.

I’m amazed at the value of your TSFA. Given that the maximum you could put in is $31,500 as of 2014 you more than double it ! Mine is at $36,000, but I could only top it up this year with $16,000 deposit in January. To reach $64,000 in 5 year by contributing $5000 per year is quite a feat I’d say. Did you do it with dividend stock as well or you hit the jackpot on a few stocks ?

@FT, very interesting post! I’ve never calculated total net worth of our household, but estimated it now and it’s very closed to yours :)

And when in end of 1999 we imigrated to Canada, we had with us about 120K, so even trend is similar :)

Couple of months after we came to Canada we bought house for 232K, paid 95K downpayment and in 6 years paid out all mortgage using Prime minus

LOC.

The biggest difference between us….we don’t use LOC for Investments, actually don’t use it at all after paid out mortgage and our CASH portion is significantly higher… Let me ask what is your age?

P.S. Almost all our cash until recent was also in ING in children saving account who paid 2$ interest. Last month they reduced it to 1.5% and we moved all cash to Peoples Trust who pays on HISA 1.8% , on 1 year GIC 2.2% and TFSA 3%

Thanks for the kind feedback Arun. All the best in your journey!

Hi FT,

You inspired me to start my journey to financial freedom. I am in the very early stage. My goal is to hit million dollar net worth in 10 years. My net worth increased by 10.32% last month. Glad to see those gains in numbers. I am not calculating any tax or other expenses at this moment. I am still in learning the learning process.

Arun.

@TM, Thanks for the kind feedback. The tax liability for the RRSP is basically a tax percentage of the current value. For specific numbers:

“Another big change to the net worth statement is that I have included my corporate investment account and added future tax liabilities. The future tax liabilities include future taxes owing for our RRSP (30% of total), leveraged dividend portfolio (20% of capital gain), and the corporate investment account (23% of total). I took the middle of the road approach for the tax rates used as I typically minimize taxes owing as much as possible. For example, I only withdraw as much from the corporate account in the form of dividends so that no personal tax is owing (after all personal tax deductions).

For the leveraged dividend portfolio, I do not plan on ever selling, but you never know what the future may bring. If I do sell, then capital gains tax is owed. Finally, for the RRSP, my plan is to withdraw from the RRSP accounts during years when income are very low, thus a low resulting tax rate.”

What is the next step? After hitting the million dollar net worth milestone, I’ll continue working on building passive income towards financial freedom.