Canada’s Best Energy Dividend Stocks 2026

Given the March 2026 volatility in energy markets, Canada’s best energy stocks are certainly seeing a renewal in investor interest! You’ll find one of them on our Best Canadian Dividend Stocks list, and a few on our Dogs of the TSX list, but sadly they are not in our Canadian Dividend Kings 2026 picks. (Though they could certainly be there by the end of the year if $100 oil becomes a thing).

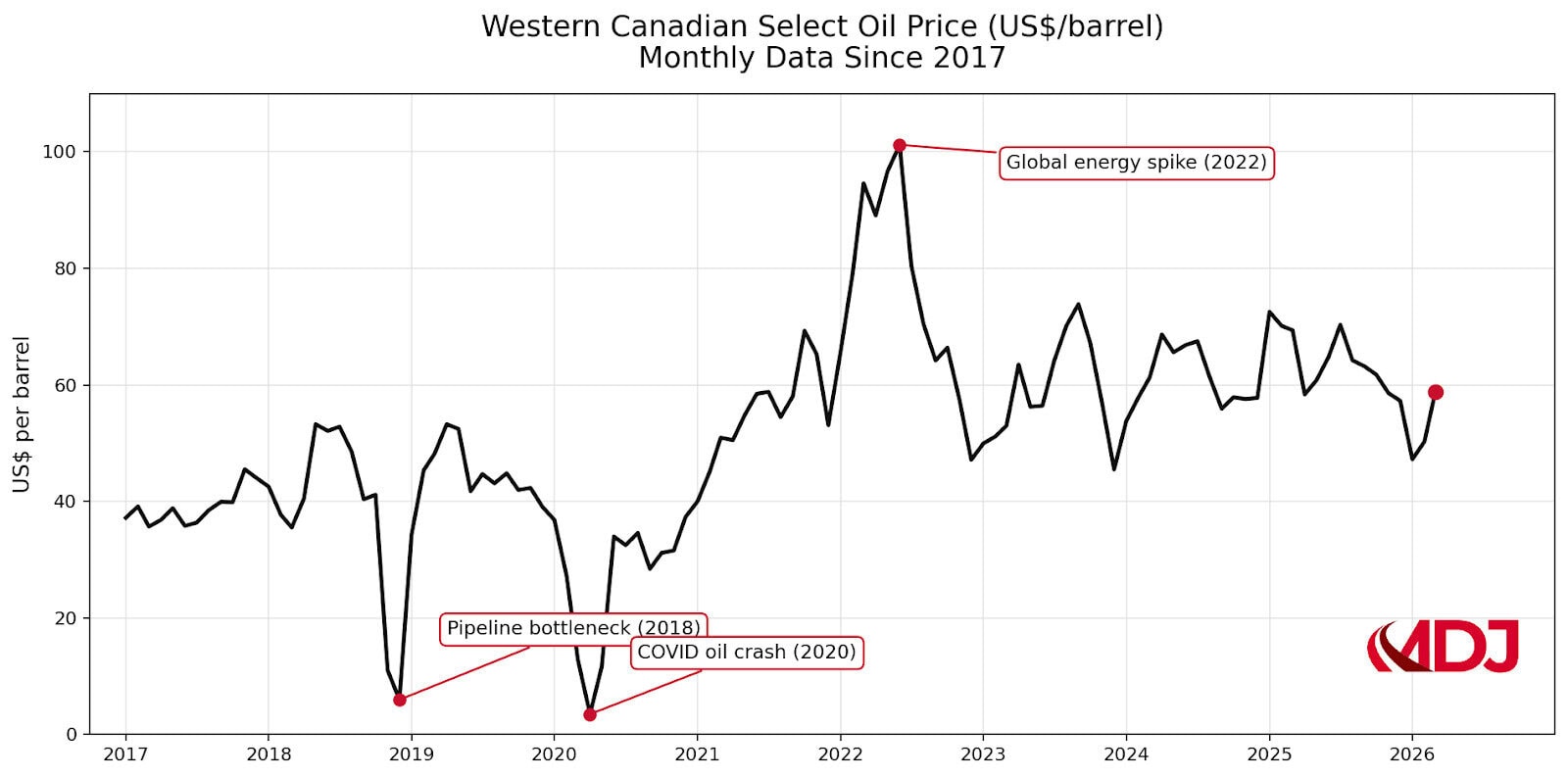

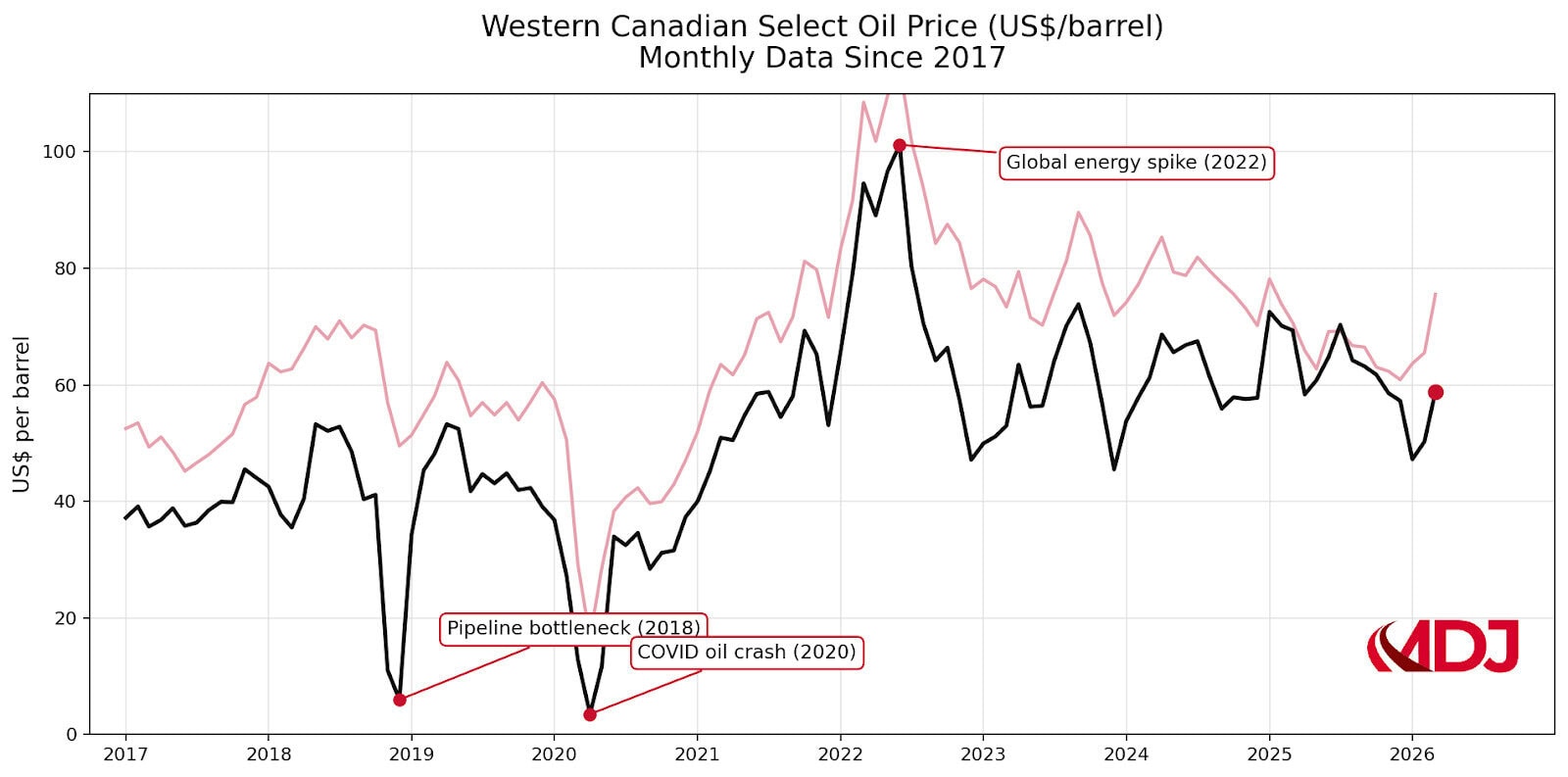

Canadian oil and gas stocks are always boring (until – as recent events in the Middle East have proved – they’re not). To get a full understanding of the big picture of these companies’ ability to gush dividends over the long-term, let’s take a look at the last few years in the charts below.

You’ll notice that leading up to Covid, there wasn’t exactly a big demand for world oil. Things then spiked as the post-Covid world economy (and thirst for oil) rocketed upwards, before eventually settling into an equilibrium the last couple of years. These charts also help put two things in context:

1) Just how high could the price of oil get?

2) How much are Canadians actually getting paid for their oil? It’s important to note that this isn’t the same as the world’s oil prices because we have historically sold at a discount due to our dependence on US refining. This gap in what we get vs what the world is offering has been significantly lessened by the opening of the Transmountain Pipeline.

Going into 2026 the prevailing wisdom was that $60 per barrel pricing was the base case and that energy dividends would be just fine in this environment. Canadian oil companies have gotten much more efficient with managing their cash flow over the last ten years, and consequently they can generate profits with lower revenues. They aren’t spending like crazy to explore new areas or paying premiums to start new operations.

That’s great news for Canadian dividend lovers who aren’t really that concerned with big capital gains. Of course, now that very little oil is getting out of the Straight of Hormuz, there is a much more profitable scenario on the table for at least some part of 2026. Depending on how much oil refining and transportation assets are hit by Iranian drones/missiles these companies will enjoy thicker profit margins.

Good luck predicting what direction a war in the Middle East is going to take (and it should go without saying that the human trauma here is the much more important aspect of the conflict), but as we “go to press” here it doesn’t appear that an end is in sight any time soon.

Canada’s Largest Energy Stocks Comparison

Ticker | Company | Price | Market Cap | P/E | Dividend Yield |

ENB.TO |

Enbridge

| 73.63 | 161.21B | 22.84 | 5.25% |

TRP.TO |

TC Energy

| 87.24 | 91.19B | 25.22 | 4.01% |

CNQ.TO |

Canadian Natural Resources

| 61.96 | 125.58B | 19.06 | 3.90% |

SU.TO |

Suncor

| 78.74 | 92.83B | 16.12 | 3.07% |

IMO.TO |

Imperial Oil

| 162.61 | 78.95B | 25.29 | 2.13% |

CVE.TO |

Cenovus Energy

| 31.84 | 58.47B | 14.54 | 2.57% |

PPL.TO |

Pembina Pipeline

| 60.58 | 35.30B | 22.81 | 4.67% |

(Hidden, click for access) | ?????? (Hidden, click for access) | ?????? (Hidden, click for access) | ?? | ??.?? | ?.??% |

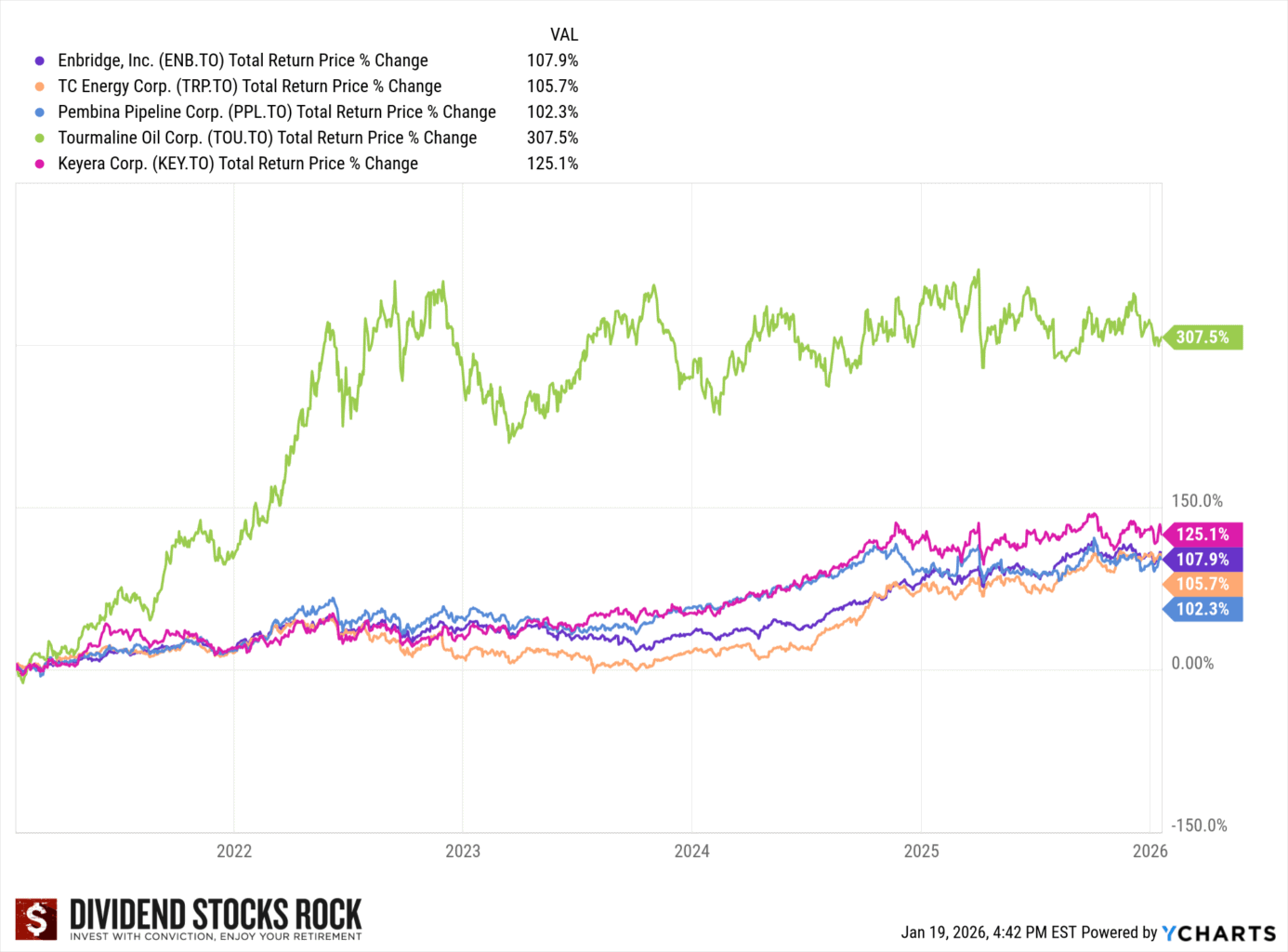

As you can tell from the chart above, if you’re a risk averse dividend investor, Canadian pipeline stocks are a much more stable bet (although potentially with much less of an upside) over the medium- and long-term.

Mike Heroux – the man behind DSR – is a CFA and has been studying Canada’s dividend players for several decades. His free webinars on the value of the mid-stream pipeline companies (they’re not building any more of them) versus the mercurial nature of the oil companies themselves really makes sense. You can read our full Dividend Stock Rocks review here.

The Long Term Strength of Energy Stock Dividends

The story on energy stocks has evolved, in that our green desires do not match the energy reality. Today there are reasonable fears of an energy crunch that could turn into an energy crisis. The renewable energy transition will take a decade or two.

In the meantime we have increasing demand for oil and gas and greatly decreased CAPEX – there’s little desire to look for more oil and gas. In fact, it’s politically unfashionable to suggest that we need more oil and gas, or to spend the time and money necessary to find and produce more oil and gas.

That sets up a secular and positive trend for traditional oil and gas. It is an unfortunate reality.

The story goes back to the most basic economic principle – supply and demand.

On the bullish side, Eric Nuttall, portfolio manager at NinePoint Partners suggests it is a generational investment opportunity. Eric often reminds us that the free cash flow that many of these companies produce is beyond generous, it is ridiculous. They can quickly pay down debt, buy back shares and return more value to shareholders by way of generous dividend increases.

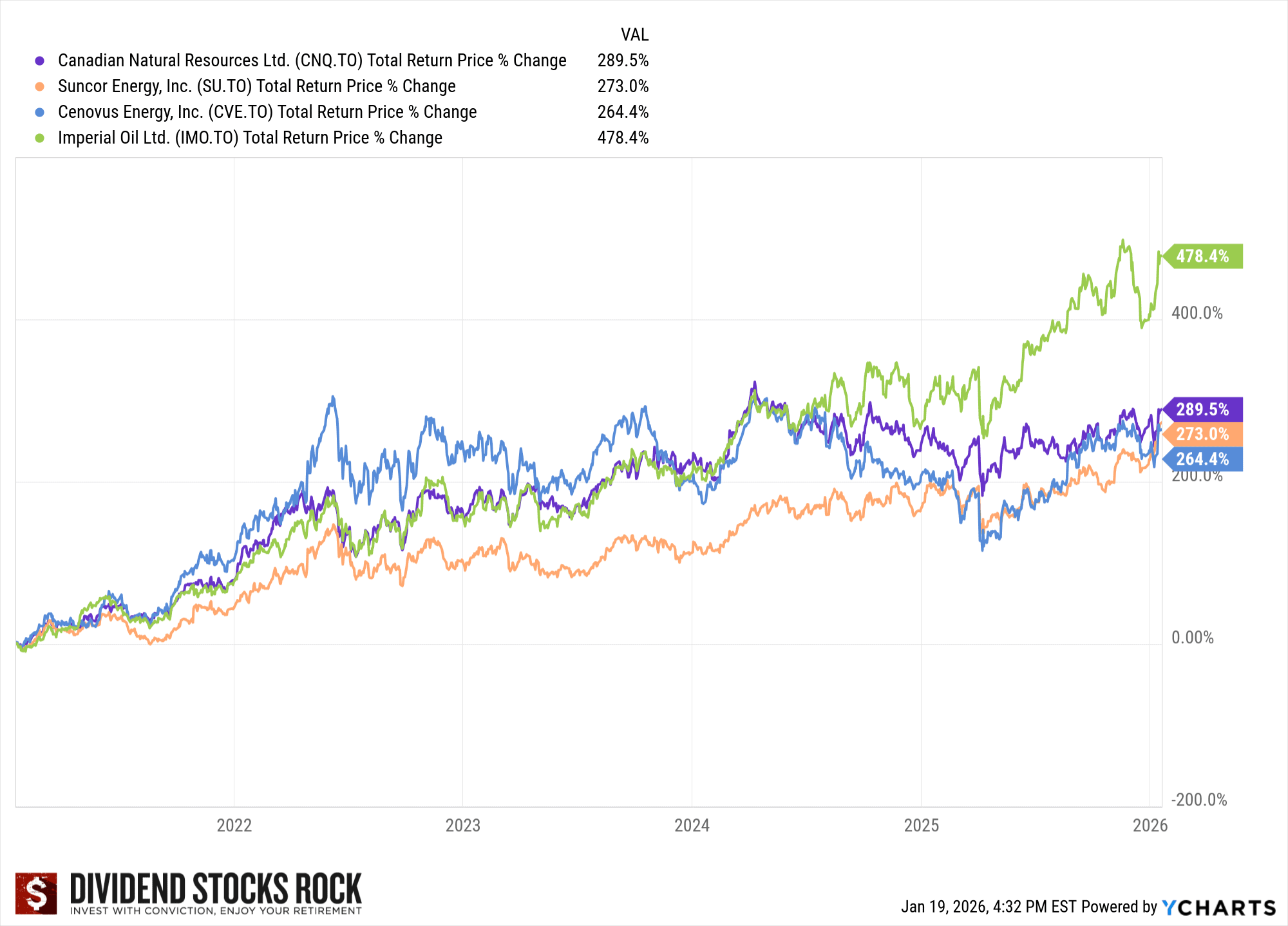

From the time of my original Best Energy Stocks in Canada post, you would have seen some generous (and growing) income. That said, you would also have total returns of 270% leaving the TSX Composite in the dust.

Investing In Canada’s Big 4 Energy Stocks (Suncor, Canadian Natural Resources, Cenovus, Imperial Oil)

If you want a quick reminder of how cyclical commodity markets can be, you don’t need to look much further than Canadian energy stocks. While you weren’t a big winner if you were a shareholder from 2015 to 2020, the last five years have been quite rewarding. To give some context, over the last five years, the TSX 60 index delivered a total return of roughly 110%. That’s a very solid run for a developed market index.

But Canada’s four largest oil companies absolutely crushed that number. Looking at Suncor, Canadian Natural Resources, Cenovus, and Imperial Oil, the group delivered roughly 300% total return over the same five-year period. In other words, investors in these companies saw about three times the return of the broader Canadian stock market.

Interestingly, 205% of that return came from capital gains, while about 95% came from dividends. Canadian energy companies have quietly become some of the most aggressive dividend payers on the TSX, and those payouts added up quickly for investors who were willing to tolerate the volatility that comes with commodity businesses.

However… to provide even more context: Even with that incredible five-year performance, the 10-year total return for those same companies is only around 235%.

The basic idea is this: Oil stocks rarely deliver smooth, steady compounding. They tend to move in powerful cycles. Long stretches of weak commodity prices can drag returns down for years. Then a supply shock, geopolitical event, or commodity cycle reversal can send profits and share prices soaring in a relatively short window. The last five years happened to line up with one of those powerful upcycles.

As I mentioned earlier though, there’s another reason (in addition to the broader oil cycle) that these companies have been printing cash. Over the last decade, the Canadian oil industry quietly became much more efficient. Oilsands operators spent years cutting costs, improving reliability, and squeezing more production out of existing assets. Most projects today can operate profitably with oil prices somewhere around US$40 per barrel. That’s a huge shift from the old narrative that oilsands projects needed extremely high oil prices to survive.

Another key difference is how management teams are allocating capital. During the 2000s and early 2010s, oil companies spent enormous amounts of money trying to grow production as quickly as possible. Investors often got burned when those expansion projects ran over budget or when oil prices collapsed. Today the industry looks very different.

Instead of chasing growth, most of the big Canadian producers have focused on paying down debt, returning capital to shareholders, and running their operations more conservatively. Balance sheets across the sector are far stronger than they were during the last oil boom. Several companies even issued special one-off dividends in addition to raising their quarterly dividend payouts fairly aggressively.

Share buybacks have also become a major driver of returns. Since 2021, the large producers have spent billions repurchasing their own shares, shrinking the number of shares outstanding and boosting per-share profits. For long-term investors, that combination of dividends plus buybacks has been extremely powerful.

Adding the Best Canadian Pipeline Stocks to My Portfolio

In addition to my list of best oil dividend stocks, I also hold a couple of Canadian pipeline stocks: Enbridge (ENB) and TC Energy (TRP). You’ll find those companies in the portfolio that focuses on Canadian Wide Moat Stocks and are stellar Canadian dividend all stars.

Some folks consider these large pipelines to be part of the “energy stocks” universe, while others say that this midstream segment constitutes its own investment class completely. I see an argument both ways, but the important thing to know is that pipelines are much less tied to the price of oil for their profits.

While I largely missed out on the Tourmaline surge, I’m still pretty happy with my larger, more stable stock allocation. You can see below that pipeline stocks haven’t had nearly the wild cyclical ride that Canadian oil dividend stocks have had. Instead they rely much more on steady dividends for their overall returns.

If Canadian energy producers are the “boom” side of the energy sector, pipeline companies tend to be the “toll collectors.” The basic idea is simple: Oil and natural gas still need to move from the wellhead to refineries and then to export terminals. Pipelines own the infrastructure that makes that happen, and in many cases, they get paid whether commodity prices are high or low. Prices would have to get CRAZY low before it made sense for the oil companies to cut production altogether and not pay the pipelines.

Over the last five years, the large Canadian pipeline companies – Enbridge, TC Energy, and Pembina – have delivered roughly 125% total return. That’s a solid result, especially considering that the underlying business model is designed to be much steadier than the volatile profits of oil producers.

A big reason for that stability is long-term contracts. Many pipeline projects operate under agreements that last 10 to 20 years (sometimes even longer). Energy producers commit to paying for transportation capacity whether they fully use it or not. Those “take-or-pay” contracts create a fairly predictable stream of revenue for pipeline operators. In practice, that means pipeline companies often behave more like regulated utilities or infrastructure assets than traditional energy businesses.

That predictable cash flow is also why Canadian pipelines have become some of the most reliable dividend payers on the TSX. Yields in the 4%–7% range are common, and investors have come to expect steady dividend growth over time.

Of course, pipelines are not risk-free. Large infrastructure projects are expensive and politically controversial. Environmental approvals, regulatory battles, and construction delays have become a major part of the story over the last decade. Projects like Keystone XL and Coastal GasLink showed just how complicated building new pipeline capacity can be in North America.

That political risk has created a strange dynamic for investors. On one hand, it makes it harder for pipeline companies to build new projects. On the other hand, it also makes existing pipelines more valuable, because replacing them is extremely difficult.

From a long-term investor’s perspective, pipeline stocks often sit somewhere between high-yield dividend stocks and infrastructure investments. They usually don’t deliver the explosive upside that energy producers can during commodity booms, but they tend to generate steady income and more stable returns over time. For investors who want exposure to the energy sector without betting directly on oil prices, pipelines can offer a useful middle ground.

The Canadian Energy Stocks Dividend Portfolio

I’m happy to hedge inflation and accept those risks. I now have an 11% allocation – not including the generous toll-taking by way of my Canadian pipeline stocks. And given that I am in the semi-retirement stage (my wife is within 5 years of retirement) I am glad that I moved to the energy dividend stocks approach.

In addition to the Big 4, I also hold positions in Birchcliff Energy (BIR) Freehold Royalties (FRU) and Pine Cliff Energy (PNE). I also hold the Ninepoint Energy Income ETF (NRGI) that holds more U.S. stocks. I’m happy to have that added exposure.

Here’s a list of some current yields available in the space.

Canadian Energy Stocks By Dividend Yield

Here’s a quick ranking of the pure-play Canadian oil stocks by dividend yield:

1) Whitecap (WCP.TO) 5.35%

2) Canadian Natural Resources (CNQ.TO) 3.90%

3) Suncor (SU.TO) 3.07%

4) Tourmaline (TOU.TO) 3.02%

5) Imperial Oil (IMO.TO) 2.13%

As a relatively small company (and consequently a more risky investment) Whitecap offers one of the highest dividend yields among larger Canadian oil producers and pays its dividend monthly (which makes it particularly attractive for income-focused investors). The company has focused on keeping its payout well covered by free cash flow, although like most upstream producers, the dividend ultimately depends on oil prices remaining reasonably healthy.

Canadian Natural Resources has built one of the strongest dividend growth records in the Canadian energy sector. The company has increased its dividend for more than two decades and benefits from long-life oilsands assets that generate very large cash flows during strong commodity cycles. Many investors view CNQ as one of the most reliable dividend growers in the TSX energy sector.

Suncor’s dividend yield is slightly lower, but the company combines dividends with large share buybacks and a diversified business that includes refining operations. That integrated structure tends to stabilize cash flow compared to pure oil producers, and management has increasingly focused on returning capital to shareholders.

Tourmaline is primarily a natural gas producer, and its dividend structure reflects that. The company pays a regular base dividend but often supplements it with special dividends when gas prices are strong, meaning the total income investors receive can vary from year to year.

Imperial Oil offers the lowest yield in the group, but that’s partly because the company returns a larger share of its excess cash through share buybacks rather than higher base dividends. Over time that approach can still produce strong total returns even if the headline yield looks modest.

The main takeaway is that Canadian energy dividends can be attractive, but they remain tied to commodity cycles. When oil and gas prices are strong, these companies generate enormous free cash flow and return large amounts of capital to shareholders. When prices weaken, dividend growth can slow or pause until the cycle turns again. If you’re looking for a pure dividend yield play, then Canadian pipeline stocks are probably more your cup of tea.

Where to Buy Canadian Energy Stocks?

Canadian energy stocks, and the ETFs mentioned above, can be bought through any licensed broker or financial institution. Our top pick at the moment is Qtrade, but if you want to see more options then check out our full list of online brokers in Canada.

Best 2026 Broker Promo

Up To $2,000 Cash Back + Unlimited Free Trades

Open an account with Qtrade and get the best broker promo in Canada: $100 when you invest $1,000!

The offer is time limited - get it by clicking below.

Must deposit/transfer at least $1,000 in assets within 60 days. Applies to new clients who open a new Qtrade account by July 31, 2026. Qtrade promo 2026: CLICK FOR MORE DETAILS.

Canadian Energy Stocks – FAQ

Best Energy Stock to Buy In 2026

If there’s one clear takeaway from looking at Canadian energy stocks over the last decade, it’s that timing and patience matter a lot. That rings pretty true this week!

These companies are not slow, steady compounders in the same way that Canadian bank stocks are. Energy profits ultimately depend on oil and natural gas prices, and those prices can swing dramatically depending on global economic conditions, geopolitical events, and supply shocks. That said, Canadian oil companies have grown fairly adept at setting sustainable dividends and focusing on efficiencies as opposed to the traditional growth-at-all-costs mentality we saw in the early 2000s.

We saw a perfect example of the cyclical reality even before this most recent Middle East war. After the enormous profit surge in 2021 and 2022, the oil price pullback in 2023, 2024, and 2025 meant that profits across the sector cooled somewhat. Returns were still respectable, but they didn’t quite match the bonanza investors experienced during the earlier part of the cycle. Even so, strong companies continued to perform well.

It’s also one of the reasons why quality companies such as Canadian Natural Resources (CNQ) continue to show up near the top of many Canadian energy stock rankings year after year. The company has built a reputation for disciplined growth, strong free cash flow generation, and a management team that consistently prioritizes shareholder returns.

Another key advantage is CNQ’s cost structure. While many oilsands companies require relatively high oil prices to remain profitable, Canadian Natural Resources can still generate profits with WTI oil prices at roughly $35 per barrel. That kind of resilience matters in a sector where commodity prices inevitably move in cycles. That’s why it’s my pick for Best Canadian Energy Stock in 2026.

More broadly, the Canadian energy sector today looks very different than it did during the last major oil boom. Balance sheets are stronger, capital spending is far more disciplined, and management teams are clearly prioritizing returning cash to shareholders rather than chasing production growth at any cost.

When oil and natural gas prices are strong, Canadian energy companies can generate enormous profits and reward shareholders handsomely. When the cycle turns the other way, returns can stall for years. That’s why energy stocks tend to work best as one component of a diversified portfolio, rather than the entire strategy.

For Canadian investors specifically, though, the sector remains hard to ignore. Energy is a major part of the domestic market and one of the country’s most important export industries. Owning a few of the stronger companies can provide both income and exposure to global commodity cycles.

Just don’t expect the ride to always be smooth. Canadian stocks can be incredibly profitable investments during the right part of the cycle, but as the last decade clearly shows, they often require a fair amount of patience along the way.

Best 2026 Broker Promo

Up To $2,000 Cash Back + Unlimited Free Trades

Open an account with Qtrade and get the best broker promo in Canada: $100 when you invest $1,000!

The offer is time limited - get it by clicking below.

Must deposit/transfer at least $1,000 in assets within 60 days. Applies to new clients who open a new Qtrade account by July 31, 2026. Qtrade promo 2026: CLICK FOR MORE DETAILS.