The Best Investments for Canadian Retirees: Stocks vs ETFs vs Robo Advisors

When discussing the best investments for Canadian retirees it’s important to understand upfront that it’s a nuanced topic. There is no one-size-fits-all silver bullet answer that will fit everyone.

I personally recommend checking out this retirement course that I gave feedback to the author on (Kyle writes here at MDJ as well). I also recommend reading these articles in order to get the full range of retirement investment options:

- Safe Withdrawal Rates (essentially, how much of your investment portfolio can you sell off each year to fund your day-to-day spending)

- How to Withdraw from Your TFSA, RRSP, and Non-Registered Accounts in Retirement

Now it’s time to talk about the nuts and bolts of how to build the best retirement portfolio for your specific needs. In other words, what actual investments to put inside your TFSA and RRSP (or RRIF).

If you’ve been following my writing here on MDJ over the years you won’t be surprised to learn that I think Canadian dividend stocks and simple Canadian ETFs are the best investments for most Canadian retirees. (And most Canadians of any age, really.)

That said, I guess as I get closer to retirement myself, I thought it might be worth it to dive into the specifics around the actual mechanics of handling a retirement portfolio, and what the various investment options are. To be honest, I don’t want to spend a lot of time talking about exotic stuff like investing in gold, or various cryptocurrencies. I wouldn’t recommend those types of investments to anyone – let alone retirees who are usually more risk-averse.

Are You Saving Enough for Retirement?

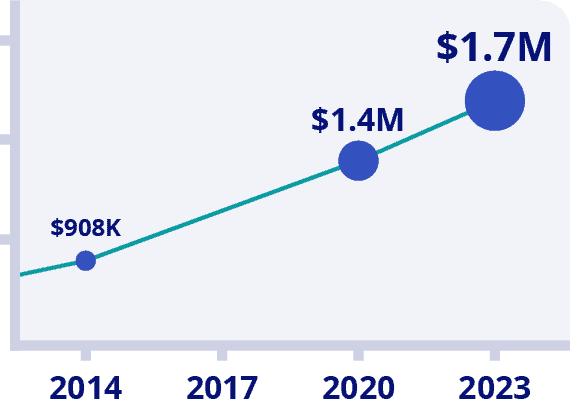

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

Why Real Estate Isn’t the Best Investment in Retirement

And while I know that many Canadians have had good luck with buying real estate over the last few decades, I don’t think that’s a very good investment for Canadian retirees. Here’s my primary reasoning:

- Using a lot of leverage to take out a mortgage on a rental property can be very risky (as Canadians who purchased homes the last couple of years are finding out right now).

- The risk of having so much of your wealth tied up in 1-3 single houses might work out – but it’s also a recipe for disaster. It all depends on the supply and demand of one single neighborhood in one city.

- The headaches of being a landlord get less and less fun as you get older.

- Canadian housing prices are still amongst the highest in the world, even after losing steam in 2022. I just don’t see how the asset continues to grow in value nearly as fast as it has been.

- The income generated is not tax efficient at all.

Now if you want exposure to a broader category of Canadian real estate, you can check our Best Canadian ETFs article for more on which REIT ETFs caught our interest.

Like I said, I know that it has worked for a lot of people over the years – and if you have a portfolio greater than $2 million or so, then the risk in buying an investment property isn’t quite as magnified – but I just don’t think it’s a good blanket recommendation when it comes to Canadian retiree investments.

Should Canadian Retirees Be in the Stock Market?

Yes! Canadian retirees should be invested in the stock market!

I am always amazed by how many folks over the age of 55 are terrified of owning pieces of the biggest companies in the world. The truth of the matter is that when you look at the longevity statistics for Canadian couples these days, there is roughly a 50% chance that you’ll live to be 90-years-old (especially if you’re female or in the top 30% of Canadians when it comes to net worth).

That means that there is a very good chance that either you or your spouse will be withdrawing from your portfolio for four decades! That’s a pretty solid time horizon to accept some risk.

Now, that said, how much risk to accept is really the toughest decision to make when it comes to investing. If we all agree that we can take some of the week-to-week volatility out of a portfolio using fixed income investments like GICs or bonds, then the question becomes, just how much risk is there when it comes to a retirement portfolio that includes various combinations of stocks and bonds?

(We’ll get into the best ways for a retiree to actually make those investments in just a second.)

A lot of smart people claim that a good rule of thumb when it comes to a retiree’s investment portfolio was: “100 – (your age) = the percentage of your portfolio you should have in equity”.

So if you were 60 years old, and had a $500,000 portfolio, then you could have $200,000 invested in stocks/equities, and $300,000 invested in fixed income like bonds or GICs. As you get older, you’d want to continue to tilt more towards fixed investments.

Personally, I would consider that a very, very conservative way to handle my investments. I have been convinced that one should be much more open to investing in stocks in retirement by the extensive work that Karsten Jeske has done over at the Early Retirement Now. “Big ERN” has conclusively proven that over longer periods of time (such as 20+ years) stocks are not more risky than bonds.

Consequently, I think it makes sense to have much more of your net worth in stocks than the traditional rules of thumb allow. I certainly intend to do so in my own retirement portfolio.

Now that said, risk is not an easy concept to internalize. While the math might show that stocks make sense as a retirement investment, it doesn’t necessarily help cure the behavioral pitfalls that humans are prone to.

Retirees have more time to think about their investment portfolio, and they are more focused on the day-to-day movements. This means that the large movements we sometimes see in stocks (40% down in a year for example) can feel extra painful.

If you are going to lose sleep and feel a lot of stress when the inevitable market downturns occur, then you need to make sure that you have planned for that – otherwise you’re guaranteed to feel a ton of pressure to sell your stocks at the worst possible time (when the market is at the bottom). Consequently, you need to determine your own risk tolerance when it comes to stock/bond allocation.

For me, I think 90%+ stocks is likely to be the best fit throughout my retirement. I think a lot of other people would be more comfortable with 60% stocks and 40% bonds or using the bonds/age rule of thumb discussed above.

Retirement Income Using “Investment Buckets”

You will see a lot of experts out there recommend the idea of splitting up your retirement investment portfolio into three “mental buckets”.

The idea behind these buckets is that it can reassure you that you have enough safe retirement investments for the next 1-5 years, while also making use of the long-term returns associated with the stock market. Here’s a look at one model of this retirement bucket investment strategy:

Bucket 1: I Need the Money This Year

This money should be in one of our Canadian High Interest Savings Accounts. You’ll need it in the next few months to pay your day-to-day bills, so you want it “liquid” and readily accessible.

Bucket 2: I Need the Money In the Next Five Years

Usually I’d say this money should be in bonds or bond ETFs, but I think that given how high Canadian GIC rates are right now, GICs actually make the most sense.

The idea here is that the stock market often goes down for 1-5 years at a time – so you don’t want to be forced to sell off your riskier investments at a bad time. Consequently, what you should do is create a “fixed income ladder” where you determine your spending needs each year, and then put that much money in a 1-year GIC, a 2-year GIC, etc.

Each year, when your GIC matures, you just take that money and roll it right into your high interest savings account for spending purposes.

Bucket 3: Your Stocks – I Need the Money In Five or More Years

Stocks (aka: equities) are the riskiest investment in most retiree’s portfolios. They are for the long term, and you don’t want to be forced to sell them at the wrong time. Most years (about three-quarters of the time) stocks gain in value. But there have been years when stocks are down 40% or so. Those can be scary years if you need money ASAP!

Now these buckets don’t all correspond nicely to what should be in your RRSP and TFSA, so to fully optimize this strategy, I recommend re-reading Kyle’s primer on withdrawing from your RRSP, TFSA, and non-registered accounts in retirement.

There is nothing terrible about this retirement bucket investment strategy. If it helps you sleep at night, and lets you stick to your plan – then I think it’s a good idea. That said, I don’t believe that it’s the optimal solution.

Again, Mr. Jeske’s research and reasoning has led me to the conclusion that investment buckets aren’t (mathematically speaking) the best way to go.

Now – it bears repeating – math does not take behaviour into account. The most important consideration to make when looking at what percentage of your retirement portfolio to have in equities, and how much to have in fixed income, is that you understand yourself, and your reaction to what you might be looking at in a 2008-type of scenario for stocks.

Ok, with that warning in place, we actually see from Jeske’s research that stocks are not in fact riskier over the long term. So for me, personally, I will likely only have two buckets:

1) The cash I’ll need this year – which I’ll put in a high interest savings account.

2) My long-term investments. These will almost assuredly be all stocks. Given that I have a high exposure to Canadian dividend stocks in my non-registered portfolio (including my Smith Manoeuvre investments), I will likely spend the dividends that I receive each year first, and then make further liquidity decisions from that point.

Cutting Fees On Your Canadian Retirement Portfolio

Once you’ve decided on your personal best investments for a Canadian retiree, the next two questions become:

1) How do I buy and hold those investments for the lowest possible cost?

2) If I want to make it a little easier, am I prepared to pay a little more?

If you’re a longtime MDJ reader then you know that I keep our Best Canadian Online Brokers article updated monthly, and that purchasing your own stocks, bonds, and ETFs through a broker is the lowest cost way to invest.

Right now, my favourite online broker (Qtrade) has an outstanding RRSP season promotional offer:

With Qtrade, you get a very beginner-friendly platform that will allow you to buy and sell ETFs for free. Your dividend stocks will cost you a few bucks every time you buy and sell them.

A Quick MER Fees Explanation

Management Expense Ratios (MERs) are a very important number to understand when it comes to investments for retirement.

MER fees are kind of awkward for Canadians to understand, because we’re used to paying for things in Canadian Dollars. We go to the dentist and we pay a couple hundred dollars for a cleaning. We go to a lawyer and they tell us the cost will be $250 per hour.

The investment industry, on the other hand, long ago realized that if you charge people in a weird way that no one understands – then you can charge them a lot more! MER is shown as a percentage. That percentage number is always a small number – BUT what you have to realize is that the percentage you see applies to every single dollar that you have invested (whether your investments made money that year or not).

Canadian mutual funds (a very common way to invest in stocks and bonds) have the highest mutual fund fees in the world at about 2% in 2022 according to Morningstar mutual fund expert Ian Tam. That means that if you have a $500,000 portfolio, you’re paying about $10,000 every year in MER fees.

The sooner that all Canadians get out of mutual funds the better. Their high MERs are a scourge on investor returns. Don’t let anyone else tell you differently. There is no evidence that mutual fund managers can pick stocks any better than your pet cat – just stay away from them.

Back to regularly-scheduled programming…

MERs on basic index ETFs are about 0.10% to 0.25%. In other words, they’re about 10% the cost of a mutual fund. They’re also more tax efficient than mutual funds, and have a vastly superior long-term track record when it comes to investment performance than the average mutual fund in Canada.

Of course, if you buy your own stocks, then you don’t have to pay any MER. In that case you only pay the transaction cost to buy or sell the stock.

While paying no MER sounds pretty good (and it is), it can be difficult and time consuming to build a truly diversified portfolio of individual stocks. Consequently, a lot of people will use index fund ETFs to easily and quickly invest their retirement nest egg.

As we’ve previously talked about, an index fund is a general term that covers a few different specific types of investments. When we talk about an investing “index” – that’s just code for “all of the assets in a given market”. That given market could be all of the stocks in Canada, or it could be a broad sampling of government bonds in the USA. An index can also be a much smaller and somewhat complicated niche, such as one that tracks the prices for agricultural companies and is called “COW” (I’m not making this up).

Remember that ETFs are the nanaimo bars of investments. By buying one small square (“unit” in investment terms) you get to benefit from many tasty layers of stocks or bonds.

Most Canadian retirees only need to focus on the most basic indexes and index funds. These big, simple, index funds are very cheap to buy and list every single one of the biggest companies in the world, or all of the government bonds in Canada.

If you Google “index funds” you’re likely to be bombarded by ads for a financial industry that is trying to sell you high-fee products under the guise of being friendly to low-cost investors. What happened here is that the big financial companies realized that low-cost index investors, who didn’t want to pay crazy high fees to invest in mutual funds, were killing their golden goose. So, they started to invent different products that stole the common names that had been applied to this newer, cheaper style of index investing.

ETFs are going to spread your investment dollars out so that you’re guaranteed to get the average of that specific market (for about 10% of the cost that you’d pay for mutual funds in Canada).

For example:

- The VCN ETF takes your investment dollar and uses it to buy small chunks of the 185 biggest companies in Canada. You will get the average return and the average dividend from this diverse group of companies.

- The VXC ETF buys small chunks of the 11,400 biggest companies outside of Canada. (More than half of them are in the USA.)

- The VAB ETF splits your investment dollar into hundreds of the lowest-risk bonds in Canada. You will get the average interest rate that these bonds are charging their borrowers, and the average of the very small capital gain movement that they will experience as well.

Should Canadian Retirees Use a Robo Advisor?

ETFs are the cheapest way to harness the power of index investing.

There are two main ways that Canadian retirees can choose to handle their index investment portfolio.

1) Go online, open a discount brokerage account, put money into that account, and buy the ETFs directly using the Toronto Stock Exchange (TSX).

2) Open an account with a robo advisor (which will then purchase index ETFs on your behalf automatically).

Now, opening a discount brokerage and going full DIY as you handle your own investments is very doable for most people. You’ll probably have to dedicate a few hours to the reading and paperwork so that you can get properly set up. After that, it will take you literally a few minutes each year to handle your investing – if you stick to simple index investing, that is.

However, a lot of people get intimidated by this process. A lot of the terminology can be kind of scary, and while we’re generally fine with spending hundreds of dollars to purchase clothes online, buying hundreds of dollars of ETFs online proves to be a much easier process to endlessly procrastinate.

I, personally, have recommended index investing through discount brokerages to hundreds of people over the years, and I bet close to 90% left our chats saying that they were definitely going to do it.

The most common result?

They did nothing. They didn’t open a discount brokerage account. They didn’t buy ETFs. They didn’t start investing.

Maybe I’m just not much of a motivational speaker!

That psychological hurdle of getting started and actually clicking “buy”, combined with the small paperwork obstacle, has proven to be a very large mountain to climb for most people who are busy in their day-to-day lives.

This result is nothing short of a financial tragedy.

Anything that prevents people from investing or indirectly funnels them into the clutches of slick-talking financial salespeople means that folks are giving up a ton of financial freedom in their lives. They’re giving up family trips or early retirement. They’re giving up the incredible feeling of financial independence. And they’re giving it up because the financial industry has worked really hard to tell them that they can’t invest on their own, and to confuse the mathematical facts of how long-term investing truly works.

Into this gaping chasm of information and action stepped the robo advisors. About ten years ago a service began to exist that basically said:

“Send us a small amount of money each month [or each year…or whenever] and we’ll instantly invest it into a pre-arranged batch of index ETFs for you. Oh – and we’ll also be around to answer any questions you might have about how to use the platform, or how taxes work on this investing stuff.

Basically, email us or use our online chat, and we’ll answer your questions. In return for this convenience, we’re going to charge you somewhere in the neighbourhood of about $60 annually for every $10,000 that you invest with us (an MER of .60%).“

Initially, I was skeptical of any financial service, but these platforms were sticking to index investing, and using most of the same ETFs that I was – so they couldn’t be all bad. I started to recommend them to a few of my friends who hadn’t been able to climb the DIY discount brokerage mountain.

Then a magical thing happened: nearly all of the people who I recommended the robo advisor option to actually did it!

My friends opened an instant index investing portfolio and hooked up their bank accounts within minutes. They loved how simple it was. They loved that they could ignore the math involved with rebalancing their asset allocation. I loved that they had someone at the robo advisor to answer all of their questions – because then we could talk about more fun things at dinner parties!

All of that being said, I still feel slightly hypocritical at times recommending a product that I don’t personally use. I feel that for my individual preferences, opening a discount brokerage and cutting my investment costs to the bone is worth the tradeoff in time and convenience. That said, I’m also a geek who likes to read financial books for fun – so I’m not a great test group. You’ll have to decide if the cost is worth it for you.

Our article on the best all-in-one ETFs in Canada fully explains the trade-offs of costs and convenience when it comes to the various different ways to invest in stocks in Canada. I really think it’s worth each retiree’s time to consider a robo advisor if they don’t want to handle their own investments. The fees are substantially lower than the ones from mutual funds and it is really just so incredibly easy to use one.

Best ETFs for Retirement Income in Canada

While I think that there is a really solid argument for a plain vanilla all-in-one ETF being an excellent option, I know that many retirees are looking for income-based ETFs in order to enjoy retirement cash flow.

Here’s a quick comparison of three interesting options if you’re looking to prioritize dependable income in Canada:

| Purpose Longevity Pension Fund | Non-Guaranteed Annuity at 65 | Vanguard VRIF | |

| Targeted Investment Return | 3.5% | Varies widely. Not really relevant to the client, as they are guaranteed a certain payout in exchange for their principal. | 4.3% |

| Annual Money Yielded Into Your Bank Account as a % of Original Contribution | Hopefully 6.15% | 5-7% Depending on what conditions you attach to your specific annuity. | Varies based on market conditions. Will likely be quite close to 4% over the loooong term. |

| What happens if I pass away relatively young? | You get what is left of your original capital investment, but none of the investment returns that your money has generated. | Depends on specifics – but most annuity programs either say, “Thank you for your contributions” or they allow for some amount payable to a surviving spouse. | It’s 100% your investment – so whatever your last will and testament says, that’s what will be done with it. |

| Is the return guaranteed? | No | Yes | No |

| Management Fees | .6%-1.1% (mutual fund fee structure) | 1-3% – paid upfront and in annual fees that are pre-calculated into your promised payout. | .29% |

| Types of Investments | 47% stocks, 38% fixed income, and 15% alternative investments that include gold and commodities, picked investments by mutual fund manager (using mostly ETFs) | The amount of money to you is not really dependent on investments… but most annuity companies usually invest through stock-based mutual funds. | 30% stocks, 70% bonds, using Vanguard’s index ETFs |

These are three very different products, but they’re all created with retirement income in mind.

I’m not going to go too far into Canadian annuities because we’ve got an excellent article on the site already that goes quite in-depth. Suffice it to say, I think a lot of Canadian retirees would be well served to replace the “fixed income” portion of their portfolio with an annuity.

Vanguard’s VRIF is probably the best ETF for retirement income in Canada, as it uses a conservative asset allocation, further juiced by options in order to squeeze out the most income possible. It also has quite a low MER.

Finally, the Purpose Longevity Fund is an interesting mix of annuity-style risk pooling and investment returns. It’s a bit complicated, but essentially the product is able to hold very conservative investments – while paying out over 6%, because it only continues to pay you if you’re alive. If you pass, your estate will get most of your original payment back, but your investment returns will stay in the fund – thus benefiting those that live the longest. Here are the details on the purpose longevity pension fund.

Sunlife Retirement Income

In late 2024 Sun Life (a large Canadian insurance company) came up with yet another product aimed at providing income for Canadian retirees. The product is simply called MyRetirement Income.

One thing to keep in mind when looking at all of these products is that the underlying investments never really change. It’s almost always some mix of stocks and bonds (very similar to what you’d find in an all-one-ETF).

Occasionally there is a tweak such as a little bit of options revenue, or a little bit of exposure to gold. The better ones have an annuity-esque aspect where you’re kind of pooling risk (with the financial risk we’re talking about not actually dying sooner – but living longer).

MyRetirement Income is a bit different in that it is aimed at folks who have defined contribution pension plans. For a quick primer check out Kyle’s article on pensions in Canada. Defined contribution (DC) plans are used by many private employers (as opposed to the government – which uses mostly defined benefit plans). Sun Life facilitates a big share of Canadian DC plans, so it makes sense that they might want to develop a product for this market.

MyRetirement Income allows clients to simplify their retirement payments. Basically, the day you go from saving to retirement, to spending in retirement, you can let Sun Life know the date you want to receive cheques until (say your 90th or 95th birthday) and Sun Life will send you a cheque each month for a corresponding amount.

In order to guarantee these payments, Sun Life is going to put your money into a very conservative pot of investments. Because it takes age into consideration (like an annuity or the Purpose Longevity Fund) Sun Life can afford to pay out a fairly high percentage of the money in the fund (as some folks will pass away sooner than others and not collect all of their monthly cheques).

For example, if you retire at age 65 and start collecting payments – opting for the 95-year-old option – you’ll get an income rate of 5.9% of the money you put into MyRetirement. It’s not accurate to say that it’s an investment return, because a lot of that is your own money being withdrawn and handed to you.

But here’s the real crux of the matter… The mutual funds used within the SunLife MyRetirement product have an MER of about 2%. That’s insanely high!

For that reason alone, it’s really not worth looking into the product at all. You’d be much better off just looking at some combination of annuities and stock market investments such as VRIF.

Best Investments for Canadian Retirees – FAQ

How to Choose Your Personal Best Investments for Retirement

Nobody can tell you in advance what the best investments for the next 20 years will be. There are probably many people who claim they can tell you this information thanks to their magical crystal ball – but they’re lying.

If you ask any of the best financial advisors in Canada, they’ll all tell you the same thing: Choosing the best investments for retirement is all about defining your personal goals and risk tolerance. After that, selecting the right asset allocation to stocks and bonds is pretty straightforward.

In addition to figuring out what your risk tolerance is and choosing the right asset allocation strategy for your nest egg, you will need to decide what platform you want to use to invest in these assets. Some folks just aren’t comfortable with DIY-ing their retirement investment portfolio using a discount brokerage account.

If you’re looking for the ultimate combination of safety and convenience for your retirement investments, I recommend checking out Kyle’s retirement course by clicking here. In that course, he breaks down why the best solution for most people is probably a combination of an annuity, and a simple broad-based all-in-one ETF. He also answers any questions that you have in his online classroom.

Are You Saving Enough for Retirement?

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

I've Completed My Million Dollar Journey. Let Me Guide You Through Yours!

Sign up below to get a copy of our free eBook: Can I Retire Yet?

Thanks for the article. With respect to “Vanguard’s VRIF is probably the best ETF for retirement income in Canada, as it uses a conservative asset allocation, further juiced by options in order to squeeze out the most income possible. It also has quite a low MER.”. What are your thoughts on BMO’s relatively new ZBAL.T? https://www.bmogam.com/ca-en/products/exchange-traded-fund/bmo-balanced-etf-t6-series-zbal-t/

It has a higher yield than VRIF (~5.6% vs 4%), higher allocation to equity, and may be a good option for a retirement portfolio.

It really boils down to how much risk you want to take Mike. The higher allocation to equity means you’re almost definitely going to see more volatility over time. I would argue that yield that high takes some pretty high risks. What happens is that if in a given month they don’t have enough dividends on hand from the underlying stocks/bonds, and there are no capital gains to harvest, they’re going to have to return some of your original capital to you. It’s not the end of the world, but in a worst case scenario, that 6% yield will be on a much smaller portfolio than before.

There is an error on the 100 – your age rule. The article says “100 – (your age) = the percentage of your portfolio you should have in fixed income”. It should be: “100 – (your age) = the percentage of your portfolio you should have in equity”.

That would be correct Yael! *changed/updated*

Thanks for the help!