Investing In Gold In Canada 2026

Given the insanely speculative run we’ve been on in 2026, it probably isn’t a big surprise that our comment board has been full of requests about how to invest in gold in Canada (and then how to sell gold as well)!

Just a month ago it looked like gold was on an unstoppable trajectory. The narrative was that central banks were buying the precious metal in order to diversify away from US Dollars and hedge against market risk. Then the speculators jumped on board and we were off to the races.

Then something really weird started to happen. Gold – which has always been looked at as a “safe haven” (a place to put money when everything else was doing poorly and there was a general panic) – started to go down… in the middle of a war?!

A war is usually the exact conditions that gold is supposed to do quite well in. So, has investing in gold basically just turned into buying a meme stock – or is this a short term phenomenon? In this article we’ll give you all the details on why people invest in gold, the different ways you can buy gold or get exposure within your portfolio – and why it may actually not be the best choice after all.

If you’re thinking about investing in gold, it’s important to understand how it fits into your overall portfolio. Our free ebook Can I Retire Yet? explains the key principles of diversification and long-term planning, helping you decide whether gold plays a useful role in your path to financial independence.

Why Invest In Gold?

The theory behind investing in gold is that the precious metal has simply been the most consistently valuable means of payment/savings for several millennia.

That long-term value hold, plus the concept of scarcity, (there is only so much of it that can ever be created) gives gold its perceived value. Historically, when people are scared away from other types of investments (stocks, cash, bonds, etc.) they often turn to alternative investments, i.e. owning gold. This means that people usually invest in gold for the following reasons:

1) They believe it will go up in value. In other words, they are speculating that they can sell it for more than they paid for it.

2) They’re pessimistic about the investment returns for any asset, and they hope that since gold has held value for so long, it will continue to do so no matter what. They’ll buy gold for now, and if other assets look better later on (when things have “calmed down”) then they can always sell it and move on.

3) They have lost faith in the banking system and/or the government (which they would likely refer to as “the man”), and invest solely in tangible assets like real estate, commodities, art, and potentially firearms if they are the “Patriotic types.”

All cards on the table, I’m not a huge fan of either one of these theories, and definitely prefer Canadian dividend stocks or keeping it super simple with a Canadian all-in-one ETF if you’re building wealth for the long term.

How to Invest in Gold in Canada

There are several different ways to invest in gold in Canada: buy physical gold at a bank or from the Royal Canadian Mint, buy gold bars at Costco, invest in gold company shares, invest in gold ETFs, or invest in gold futures.

1. Buy Physical Gold From Banks or The Royal Canadian Mint

The old school way to buy Gold is to actually purchase physical bars of gold bullion and/or gold coins. Canadian banks, the Royal Canadian Mint, or a variety of private retailers can facilitate these purchases if you’re so inclined – but a word of caution here: Possessing your own physical gold can be quite risky as it’s impossible to track if it’s ever stolen from you.

A quick search reveals that as of late March 2026, buying a 1 oz gold bar from the Royal Canadian Mint (via TD) will cost you $6,300. You can buy this gold bar online from the TD website and pick it up at any TD branch, or have it shipped to you in Canada for free.

You can also purchase gold coins from The Royal Canadian Mint – and some of them are actually usable fiat money (although I’ve never tried paying at the grocery store with one before).

It should be pointed out that while a gold bar is theoretically useful in the event of a complete global meltdown (and I’m still not sure about that one), in the meantime, it will be much harder to buy and sell than a Gold ETF or shares of a gold mining company would be. I am also not a huge fan of storing extremely valuable items at home, in terms of security and insurance costs.

There’s also an alternative in the form of buying physical gold and storing it in a designated vault in Canada or off-shore. It’s easier to sell through a platform like that if you want to liquidate your position.

2. Buy Gold from Costco in Canada

Yes, this is a real thing now. If you want to buy physical gold in Canada, Costco has quietly become one of the easiest places to do it. On Costco.ca’s bullion page, you can find a mix of 1 oz gold bars, Royal Canadian Mint bars, Valcambi bars, and Maple Leaf gold coins.

At the time I checked, Costco Canada had a 1 oz Valcambi Suisse gold bar listed at $6,359.99 and a 50g Valcambi bar listed at $10,169.99. They also had Royal Canadian Mint gold products and smaller-format options like 10g bars and fractional Maple Leaf coins.

The Costco route is pretty straightforward. You need a membership, most of the gold appears to be sold online as a member-only item, and the listings usually come with pretty tight purchase limits. Some folks online like the idea that they can buy gold with a credit card and get credit card benefits on the purchase as well.

That said, buying gold from Costco does not magically solve the usual physical-gold headaches. Gold bullion purchases are generally final sale, so you are still taking on all of the usual risks that come with owning physical gold. You have to think about storage, insurance, theft risk, and the hassle of eventually selling the metal to someone else.

So while it might feel amusingly convenient to toss a gold bar in your cart while buying paper towels and a rotisserie chicken, physical gold is still physical gold. It is a lot less convenient to buy and sell than a Gold ETF.

3. Buy gold Exchange Traded Receipts (ETRs) or Precious Metal Certificates

If you want to own some actual gold but don’t want to invest in, say, a state-of-the-art home security system, you can purchase a precious metal certificate from big banks such as RBC, CIBC, or Scotiabank. These certificates are basically title deeds for precious metals. They prove that you own a certain amount of gold, but it’s stored securely by the bank.

The Royal Canadian Mint offers Exchange Traded Receipts (ETRs) which are similar to precious metal certificates, but can be traded on the Toronto Stock Exchange (Royal Canadian Mint CDN Gold Reserves, ticker symbol MNT).

4. Invest in Gold Company Shares

If you’re less interested in being able to get your hands on actual bullion and more interested in general investing, you could consider buying gold company shares. These come in two varieties: mining company shares and royalty company shares. Royalty companies provide mining companies with the financial backing they need in order to build a mine and extract a gold deposit.

The Toronto Stock Exchange (TSX) is home to many gold companies including Franco Nevada Corp (FNV), Barrick Mining Corp (ABX), Agnico Eagle Mines Ltd (AEM), and Kinross Gold Corp (K). You can find a gold company in our best Canadian mining stocks article.

Just remember that while the value of these gold companies will obviously be somewhat dependent on the price of gold, they are individual companies at the end of the day. They come with unique costs, assets, management, etc. Consequently their future profits might prove to be quite different from one another.

5. Invest in Gold ETFs

The easiest way to invest in gold in Canada is definitely to buy a Canadian Gold ETF. Several Gold ETFs are free to trade with our favourite online brokerage, Qtrade. Read our Qtrade review or sign up by clicking the button below:

The Best Gold ETFs in Canada

A few years ago, the case for picking one gold ETF over another at Qtrade often came down to trading costs. That’s no longer true. You can read our Qtrade review for full details or see how it compares to the best online brokers in Canada.

As of 2026, all ETF trades at Qtrade are free, so there’s no longer any special advantage to choosing a gold ETF just because it used to be on a commission-free list. That’s a good thing, because it means investors can focus on what actually matters – the fund’s structure, management fee, liquidity, currency exposure, and whether it holds physical bullion, futures contracts, or gold mining stocks.

Not all gold ETFs are really the same thing. Some hold actual gold bars in a vault. Some use futures contracts to track the price of gold. Others don’t hold gold at all, and instead own shares in gold mining companies. Those are all very different bets, even if they get lumped together under the same “gold ETF” label. Here’s how I’d approach buying a gold ETF in 2026.

1) BMO Gold Bullion ETF (ZGLD)

For most Canadians who want straightforward exposure to the price of gold, ZGLD is probably the best all-around option right now. It holds physical gold bullion, has a very low MER compared to most competitors, and offers direct exposure without getting cute with futures contracts or mining stocks.

If your goal is to own gold because you want a hedge against inflation, geopolitical drama, or just the general weirdness of modern markets, then owning an ETF backed by actual bullion is usually the cleanest way to do it.

2) Purpose Gold Bullion Fund (KILO)

KILO is another strong option for Canadians who want physical gold exposure. It holds allocated gold bullion and has a very competitive fee structure. It also offers a few more version choices than some older gold ETFs, which gives investors flexibility depending on whether they want currency hedging or U.S. dollar exposure.

For practical purposes, KILO and ZGLD are both very solid choices. If I were splitting hairs, I’d probably lean toward whichever one offered the better mix of liquidity, spread, and fee at the time I was buying.

3) iShares Gold Bullion ETF (CGL or CGL.C)

CGL is still one of the best-known gold ETFs in Canada, and that familiarity counts for something. It holds physical gold bullion and is easy to buy through any Canadian brokerage account. There is also an unhedged version, CGL.C, which some investors may prefer if they want their returns tied more directly to both gold and the U.S. dollar.

The main downside is cost. CGL is still a credible option, but it generally comes with a higher MER than some of the newer or more aggressively-priced alternatives.

4) BMO Equal Weight Global Gold Index ETF (ZGD)

If you want exposure to gold mining companies instead of the metal itself, ZGD is one of the most interesting options in Canada. It holds a basket of global gold miners and uses an equal-weight approach, which gives smaller companies more room to matter than a traditional market-cap weighted fund would.

But here’s where things get messy. When it comes to gold mining companies, all the glitters is not gold. These miners are businesses, not commodities. That means your returns are influenced not only by the price of gold, but also by management decisions, production costs, debt levels, geopolitical risks, and all the other baggage that comes with owning stocks.

So ZGD can do very well in a strong gold environment (as profit margins obviously go up), but it is not the same sort of defensive asset that physical gold is supposed to be.

5) iShares S&P/TSX Global Gold Index ETF (XGD)

XGD is another long-time Canadian option for investors who want to buy gold miners rather than bullion. It remains a perfectly reasonable ETF, and for many years it was one of the standard ways Canadians got exposure to the sector.

That said, I’d probably rank it a bit behind ZGD today if your goal is broad gold-equity exposure. It still does the job, but it’s no longer the obvious standout in the category.

6) Horizons Gold ETF (HUG)

Horizons Gold ETF (now under the Global X banner) is still around, and it still offers exposure to gold through rolling futures contracts. That means HUG is still useful for some investors.

But it is no longer the easy default recommendation it once was. Back when ETF commissions mattered more at Qtrade, HUG had a very obvious edge in this article. As of 2026, that edge is gone.

Now that all ETF trades at Qtrade are free, I’d only put HUG near the top of the list if you specifically want futures-based exposure.

6. Invest in Gold Futures

Advanced investors could also consider investing in gold futures or options. If you choose to invest in this way, what you’re essentially doing is placing a bet on the future price of gold. While both gold options and gold futures are derivatives, gold options can give the investor more flexibility.

If your goal is to buy gold in order to hedge against certain scenarios, it is definitely cheaper to buy gold futures (or derivatives) than to borrow money and invest in a direct dollar-for-dollar ETF. Each gold futures contract represents 100 to 400 troy ounces per contract, with very low leverage costs.

You can explore options or futures by opening a margin account with your online broker. However, you can save yourself some headaches by simply investing in the Horizons Gold ETF, which tracks the performance of the Solactive Gold Front Month MD Rolling Futures Index ER.

Is Buying Gold a Good Investment?

Gold has not been a good investment in the past.

This goes against the sort of “common sense wisdom” that many people have passed along over the years.

The numbers just don’t lie though.

Stock market historian Jeremey Siegel’s research has proven that a dollar invested in gold back in 1802 would be worth about $227 today.

Wow – a 22,700% return you might think – that’s pretty spectacular.

Here’s the thing though – that same dollar invested in the US stock market would have grown to roughly $37 Million Dollars today!

It turns out that gold might be ok at storing value over the long term. Some market historians will make the interesting claim that adjusted for inflation, gold will purchase the same amount of goods today that it did two thousand years ago.

The problem is that it doesn’t do much. It just sits there looking shiny.

Companies make profits, pay dividends, own physical assets, invent new more productive technologies, and generally are really good (as a group) at building value.

That’s enough to retain value, but not enough to build value.

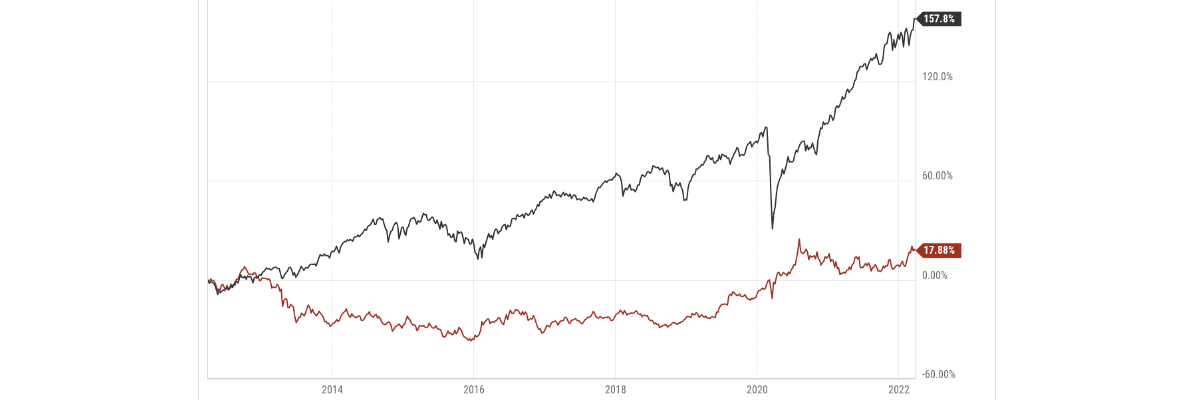

All of that said, gold was a fantastic investment in 2025 as speculators followed central banks and legitimate long-term buyers. In fact, the recent run up in gold has done so well, that gold has actually beat the returns of the Canadian stock market over the past five years.

As well as the past ten years!

Of course, over longer terms, investing in stocks has always beaten investing in gold (and in my opinion always will – just look at the long-term data for more details).Oh, and before you ask, yes, using HXT as our Canadian returns proxy includes the juicy dividend payments that our Canadian dividend kings churn out year after year.

Gold Investing FAQ

Gold Vs. Other Metals

Gold is different from most metals in a sense that its value is derived from a collectible acknowledgement of it as a store of value. While it has certain industrial uses, it is estimated that the price of gold is something like 90% speculation and 10% industrial demand. I think the current price trends that I have mentioned support that theory to a large degree.

With silver and other precious metals, a more significant portion of their value is driven from their industrial use, with some acknowledgement of them as stores of value.

With purely industrial metals, like copper, or strategic metals like Indium or Gallium, there may be speculation in the short term, but long-term, the price is pulled by the true economical balance between supply and demand. Because of their inelastic demand and growing geopolitical tensions, there is an argument that they are actually a less speculative investment that precious metals like gold and silver.

What If the World Goes to Hell?

I re-published this post on March 24, 2026, and reader Jay Cameron left a comment that was fair enough that I should answer it directly.

He wrote:

“I kind of expected more from MDJ on this article… Gold is for ‘very bad case scenarios,’ but it doesn’t have to be a global meltdown. What about runaway inflation and the stock market suspends trading? In this case you want physical gold.”

I think Jay’s comment represents a pretty broadly-held belief, so I figured I’d address it in some depth here.

On inflation, we already wrote a separate post on Canadian inflation stocks and my view hasn’t changed. We still like Canadian dividend stocks, especially banks, telecoms, and Canadian National Railway. Those strike me as some of the best hard assets around – with business models that can pass along increased costs to the final consumer.

Gold is a bit of a different conversation. If we get runaway inflation and stock markets freeze up (admittedly, a pretty small tail risk), then yes, physical gold has a much better case than something sitting on a brokerage statement you can’t access. If the scenario gets darker than that, banks could theoretically stop honouring their obligations, the financial plumbing breaks, and trust in regular currency goes out the window… then gold could end up looking smart.

My hesitation is simpler than that. I don’t know which disaster I’m supposed to be hedging against. That’s the whole problem.

Maybe it’s inflation. Maybe it turns into a barter economy where nobody cares about gold because they’d rather have food, fuel, medicine, or a working generator. Maybe it’s an impact winter and indoor farming suddenly becomes the hottest business model on Earth. Maybe it’s a nuclear event where food and shelter matter a lot more than shiny metal. Maybe climate instability makes desalination businesses the kings of the next economy.

Or maybe the economy takes a punch, limps for a while, and keeps going anyway. That’s not exactly a rare outcome. My crystal ball remains embarrassingly useless here, but you get the point in terms of bars of gold not being ironclad insurance in a worst-case scenario.

There are just too many ugly versions of “things go badly,” and they don’t all point to the same winning asset. Some scenarios have gold as the winner. Others end with farmland as the better hedge. Some end with people raising insects in a basement and calling it dinner (which is not the sort of portfolio allocation most advisors put in the brochure).

Gold might be the right hedge for one specific kind of very-low probability breakdown. I just don’t have enough conviction that even those worst-case scenarios will be saved by gold bars.

Should I Invest In Gold Today?

Gold may be one of the oldest investing tools still in circulation, but it’s certainly not the best or most reliable. Even its one redeeming investment quality – its ability to store value – is quickly losing steam. In fact, folks that advocate for buying bitcoin are using the exact same arguments that gold bugs have been using to argue for investing in gold for years! Those arguments just don’t hold up.

While gold is likely to retain some value over time, the fact is that a solid investment portfolio has vastly more growth potential in the long run. Our official verdict: you’re better off taking a look at the other low-risk investments available in Canada. Gold may glitter, but low-risk investments with guaranteed profits outshine it every time.

Gold is lot better than anything that can be printed on a piece of paper

Precious metal certificates from RBC, CIBC, or Scotiabank ?

How soon we forget ? I wouldn’t take that recommendation with a ton of salt

Would like to remind you certain Finance Minister’s action back in 2022

I kind of expected more from MDJ on this article. They figured out that gold is a store of value, not an investment, but didn’t complete the intellectual journey. If you are hedging against a bear market there are other (better) options. Gold is for “very bad case scenarios,” but it doesn’t have to be a global meltdown. What about runaway inflation and the stock market suspends trading? In this case you want physical gold. What about a localized war/rebellion? If you have no access to your online accounts, 10 oz of gold in your pocket as you walk across a couple borders is a much better safety net than an etf somewhere.

What if your PM seizes your bank accounts because they decided (after the fact) the political cause you supported was the wrong one?

Two of these scenarios sound far-fetched and they are perhaps unlikely in Canada, but we do share the artic circle with a country who has a reputation for invading neighbors! Gold (and silver) can be traded for local currency in nearly every country in the world. I don’t advocate having a lot, but ask yourself “if my currency was worthless and my family had to start over with the clothes on my back wouldn’t it be great to even have just $5k in precious metals?” or “If I lost access to my online accounts for x period of time, what do I need to not suffer to much?”

The sad truth is that if you have a localized rebellion or some other extreme scenario then all bets are off when it comes to the global economy. Bonds lose value, banks go bankrupt, all money is wiped out, why do you think the conception that gold is a token of wealth would necessarily still apply? I think buying real estate would work better in this scenario, just add whatever you planned to put in that gold bar and spend it on a bigger house.