Managing Money In Retirement – Investing with Cognitive Decline

Since writing Canada’s first online course that looked at how to create a DIY financial plan for your retirement, I’ve gotten a few inquiries about a topic that is quite delicate, and generally isn’t much fun to talk about. (By the way, you can see what the course is all about by clicking here.)

I’m referring to planning for the possibility (some might say probability) of cognitive decline as we age.

Obviously this is a massively large topic that includes many emotional elements, and should probably be looked at in a big picture context. But I’m not really qualified at all to write about the psychological, emotional, or spiritual aspects of aging.

What I’m going to do instead is address how we might want to look at financial decision making as we age, and at what stages we might want to simplify our financial planning options.

Are You Saving Enough for Retirement?

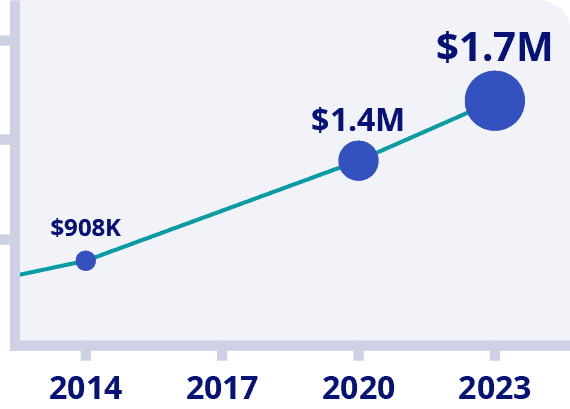

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Get $50 Discount With Promo Code MDJ50

*100% Money Back Guarantee

*Data Source: BMO Retirement Survey

My Biggest Fear

As I said right upfront, this isn’t a topic that’s fun to talk about.

In fact, for me, it’s possibly the least fun scenario to contemplate. See, I know folks generally say they don’t want to think about and/or plan for death – but I actually find that relatively easy to address. It’s a guarantee that both my wife and I will one day go to that great tax haven in the sky. Planning for it might not be easy, but it’s not exactly complicated either. There’s really only one variable to consider – the date at which it may occur.

Cognitive decline is a much, much, trickier problem to consider.

There are so many variables:

- How fast will it occur?

- Will it increase my cost of living?

- What if one spouse handles more of the finances than the other spouse?

- How do I know if I’m still making good enough decisions to DIY my own finances?

- Do I have an advisor and/or loved one that I can trust 100% to handle things if I begin to transition financial responsibility?

When you’re trying to address an issue that has so many moving parts like this, it’s impossible to have a one-size-fits-all solution.

While some of my former students might argue that I have in fact experienced some cognitive decline, I’m fairly certain I do not have any direct experience with this process yet. So what I’ve done is talk to several CFPs who have decades of experience in helping people plan around all aspects of their retirement, including a possible lack of DIY ability as a person ages. The conclusions below are the result of hearing various strategies and researching the statistics on cognitive decline.

Cognitive Decline In Canada: The Numbers

It is quite difficult to categorize the various types of “natural aging” relative to more serious conditions such as dementia. Here’s my best attempt to give you some idea of the big picture view of Canadians as we age (courtesy of the Alzheimer Society and Statistics Canada):

- 40% of us will experience memory loss as we age.

- About 8.4% of Canadians over 60 have dementia.

- Between “mainstream memory loss” and a diagnosis of dementia, there is a condition commonly referred to as mild cognitive impairment (MCI) – 10-30% of us will develop MCI.

- Financial fraud against those 65+ in Canada is increasing by 30-50% per year (depending on the source you prefer).

We are also living longer than ever before. A hypothetical Canadian couple who are both 65-years old today, has a 25% chance that one of them will live to age 98.

All of this adds up to a situation that I think most of us intuitively know is true. As we live longer, we are increasing the chances that we will spend a portion of our life where making our own financial decisions is not in our best interests.

At the same time, I know from watching my own family and loved ones that sacrificing various types of independence as we age really really sucks. There is just no other way to put it.

I can’t really imagine the day I admit to myself that I should no longer be driving, or handling my own online brokerage account. I’m quite certain I will be reluctant (probably even stubborn) to decide that I have crossed the line from, “I forget the occasional name or date,” (heck, that’s me already) to, “How do I switch money from my brokerage account to my bank account… I’m not sure where to go for help.”

To make matters even more difficult, this cognitive line is not easy to measure or define. If our politicians have recently proven anything to us, it’s that basic cognitive tests aren’t perfect measuring sticks.

What To Do About It

Now that we’ve established that this thing is real, that it sucks, and that it’s much harder to plan for than passing away – the real question is: What can we do to prepare for medium-bad scenarios, and worst-case scenarios?

I’ve written a lot about 4% + inflation rule and how to withdraw money from your RRSP and TFSA accounts, but this type of manually-optimized drawdown of your nest egg assumes that you’ll be just fine handling the DIY part of your investments the entire time that you and/or your partner are on planet Earth. Given the numbers above, I’m not sure that’s a great assumption.

Here’s a non-exhaustive list of best practices I’ve found in talking to CFPs, my own friends and family, and browsing health studies conducted by universities and the AARP.

Working With a Planner Doesn’t Always Work

Obviously the Rolls Royce of retirement planning options is to work with one of the best financial advisors in Canada. For a set-fee (NOT a commission) they can help you navigate choppy financial waters year-in and year-out, or simply give you a plan that you can stick to.

There is really no replacement for an excellent financial advisor.

HOWEVER

There are way more bad or mediocre financial advisors in Canada than there are good ones. And as we age, our ability to tell good from bad is going to decrease.

I wrote about the wealth management companies in Canada, and how to avoid the vast majority of them.

The bottom line here is that if folks are getting paid a commission to recommend certain products or investment strategies to you, then they are going to have a strong incentive to do that – whether it’s in your best interests or not!

So while working with a planner can be a good solution (especially in more mild cases of cognitive decline) one has to have a significant level of trust in their planner, and be confident that they possess the tools to effectively evaluate if that planner is capable or not.

Consider Annuities and Deferring CPP and OAS

One of the easiest wins for Canadians looking to dementia-proof their retirement journey is to look at long-term guaranteed income solutions that won’t need any decisions or paperwork as one ages.

I have written extensively about investing in annuities in Canada, as well deferring CPP and OAS.

Many Canadians instinctively hate these options. The idea of giving up “free money” now, for larger benefits later, just seems counterintuitive.

But I’ll tell you – every single CFP I talked to loves the certainty of an increased CPP and OAS cheque when it comes to creating a financial plan. These payments are indexed to inflation, and they’re just very efficient ways to create a relatively high “income floor” that is guaranteed throughout a person’s retirement, no matter how long they live or what their cognitive condition is. CPP and OAS payments are also relatively difficult to “mess up” as one gets older, and they are resistant to large-scale fraud efforts.

The same principle holds true for annuities. The continued paradox of so many Canadians saying they would love to have the pensions that many public sector employees enjoy – but hate the idea of buying an annuity – continues to astound me. The choice of giving up cash today, in return for a guaranteed stream of payments isn’t an easy one, but it is one of the best ways to protect yourself against cognitive decline.

Automate Bills As Much As Possible

Creating a list of the bills that you pay, and showing a loved one where you keep that list (in addition to where you keep details about account numbers and personal details – maybe a safety deposit box?) could be a huge time-saver at some point.

Automating as many of these payments as possible will prevent fees for bills that you forgot to pay from popping up. Setting these up sooner rather than later in life is a quick and easy win.

Which Loved One to Ask for Help?

We’ll get into what a Power of Attorney is in just a second, but before we get to that step deciding on a loved one that can be your “money person go-to” is a big step. The AARP information I read used the term “advocate”.

I really like the idea of a designated financial “advocate”.

This is the person that you might ask for a second opinion from time to time, and who can help you fight back if organizations or individuals try to take advantage of you. The better communication and the more trust established at a relatively early age, the easier the job will be for both the retiree and the advocate.

I’ve talked to several retirees who felt that “as they were getting up there in years” they had someone in their life they completely trusted – but who maybe didn’t have an ideal level of financial literacy. Consequently, they created an educational plan for both they and their advocate.

Often this just meant a few conversations together to explain why certain decisions had been made, and even just understanding all the vocabulary around financial matters in Canada. Some booked an hour time slot with their fee-only financial planner, and had their advocate come to the meeting with them. This way everyone was on the same page.

I love the idea of this sort of proactive planning. Honestly, I think there are many people for whom this “advocate position” could be the catalyst for finally learning about finances and getting their own financial future optimized.

I’d be remiss here if I didn’t attempt at least a bit of self promotion and say that going through my course together – 4 Steps to a Worry-Free Retirement – would be an excellent way to ensure that your loved one knew how to plan their own retirement, as well as a guarantee that your advocate knew what they were doing when it came to helping you in the years to come.

I have to admit that I’m not sure what the best way to select your designated “advocate” is. All I know for sure is that the rates of financial abuse of elderly are through the roof in Canada from everything that I read. Consequently, I would place trust above financial knowledge when it comes to choosing your financial helper. The other thing I’m pretty certain of is that the earlier one starts this process, the easier it is for all parties involved, and the clearer the long-term instructions can become.

What Does Power of Attorney Mean in Canada?

No one wants to think about the day when they are ultimately going to have to hand over full control of their financial situation to someone else, but like much of the other recommendations in this article, it’s much better to consider it sooner rather than later.

The main reason for that is that a Power of Attorney document will only be considered valid if the person is “mentally capable” at the time of signing.

You can read through the details of what a Power of Attorney is all about here – but the long and short of it is:

- You can assign anyone to be your Power of Attorney – don’t get confused by the “attorney” phrasing and believe that you need a lawyer.

- A Power of Attorney is a legal document that gives someone(s) authority to manage your money and property on your behalf.

- If you have a general Power of Attorney, then as soon as you become “mentally incapable of managing your own affairs” the document is now void.

- If you want a document that will continue past the “mentally incapable” point then you’ll need an “enduring Power of Attorney”.

- Unless you specify otherwise, your Power of Attorney can make financial deals, open accounts in your name, pretty much do anything with your finances – so it’s pretty important to get this person right.

- You can continue to make decisions for yourself (in addition to the decisions made by the Power of Attorney) as long as you are considered mentally capable.

- Some experts recommend having two individuals named as Power of Attorney to make fraudulent behaviour more difficult to carry out.

- Banks and financial institutions may have their own Power of Attorney firms that they want you to complete in addition to the general one.

Jason Heath of Objective Financial Partners has written about the fact that people who are acting as power of attorney have a fiduciary responsibility to manage the grantor’s financial affairs. That means they can be held criminally liable for damages that result from negligence. This is why I recommended bringing a fee-only financial advisor into the picture sooner rather than later if you don’t have someone in your life ready to take on this responsibility.

Heath highlights portfolio management specifically saying, “Be mindful of tax considerations from selling investments and most importantly, treat the money like it belongs to your parent. Some children have a tendency of treating what could someday be their inheritance like it belongs to them before it really does.”

Final Thoughts

As you proceed through retirement and get the feeling that you might not “have quite as much zip on your mental fastball” as you once did, the sooner you address these longer term scenarios the easier you will make it on yourself and your “advocate”.

One common scenario that several planners brought up was when one member of a couple had always handled the finances in the household division of labour. In that situation, the quick cognitive decline (and even worse if this decline was imperceptible to the individual suffering from it) of the more financially-active spouse placed quite a burden on the formerly-passive partner.

Having to learn a lot all at once, as well as evaluate where to get trustworthy information from is not a situation you want to put a loved one in. You might be picking up the theme of this episode is that addressing this sooner rather than later is in your best interests.

Finally, do yourself a favour and make sure your will is up to date, as you don’t want to add this to your advocate’s to do list at a later point.

This topic is certainly one of the reasons I have decided to utilize a Canadian BTSX-style dividend investing approach. Other than our RSPs that we will melt down, we expect to live of our dividends without the need to sell shares. I fully understand this is not always optimal from a total return approach, but it is a sustainable, hands-off approach that ought to maintain itself long into the years when I may no longer be capable (or interested in) maintaining oversight on our accounts.

That’s probably true James. The approach is certainly more hands off than most! I do wonder though, say we have a bad 2008-style crash again and a bunch of your portfolio cuts their dividends? I’m not trying to make a point or anything, I’m honestly asking. Do you think you’d have someone you could trust to help you if you were on that memory loss continuum?

I think that’s a great question. Is there some risk? Yes – but I think the risk is more that in a 2008 style collapse we will be at risk of no raises to dividends and potentially not be able to keep pace with inflation. Are there one or two names in our portfolio that could cut or eliminate the dividend? I think there’s some risk with ENB, with BCE, and certainly with MFC who has proven they will do it. I didn’t own Algonquin at the time of their cut, but I did pick up some shares sub $7.50 – might they cut or eliminate in the future?

The rest of our picture is my wife has a modest DB pension (it’ll equate roughly to about 2x full CPP @ age 65) – she will be able to start it when she turns 58. To me, that’s our ‘bond’ for retirement. That, and we will likely defer both my OAS and CPP to 70, while she may take OAS to replace her bridge benefit, and maybe CPP too. We are trying to achieve smooth taxation and relatively smooth income, using the Go-Go, Slow-Go, No-go plan. I think this plan will make it much less difficult to navigate any event of significance.

However, back to your original question. I have met twice with a private wealth investor from one of the big 6 banks. I think he does an excellent job and I subscribe to his weekly newsletter. I’ve always been a DIY guy and hated the idea of fees, but in the document I’ve prepared for my wife in the event of my death, my advice is she use him. I accept that I should and would be prepared to turn the reigns over to him as well should I start to feel incapable, or disinterested in continuing to manage the portfolio.

Of course, by that time I might be okay with our children taking on some of the responsibility. Time will tell.

Thanks for the question! It made me think this out a bit more than I already had – I appreciate that!

Sounds like one heck of a plan with several fail safes built in James! I was about to say, “I don’t know that I’d be so sure on that ENB and BCE dividend,” – but you’ve got so much safety net going, I think you’re more than adequately covered.