Canada’s Purpose Longevity Pension Fund: Is It a Guaranteed 6.15% Pension for Life?

For many years Canadians had some excellent options when it came to determining where they were going to get money from in retirement.

You had your Sturdy Canada Pension Plan that you had paid into.

Then you had the Old Age Supplement (OAS) to look forward to receiving each month.

Finally, many Canadians got to enjoy a defined benefit (DB) pension plan that was nice and simple at the point of delivery. You just went down to HR when you felt like you were nearing the end of your career, and asked them what your company pension was looking like (or if you were a math whiz, tried to figure it out for yourself) and then you knew that if you retired on “Day X” you would get “Y dollars” each month until you went to the great tax haven in the sky.

While the CPP and OAS are still going strong (much stronger than most would believe actually) the pension plans that Canadians used to enjoy are simply a nostalgic memory.

So when the Purpose Longevity Pension Fund launched last month “promising” an annual cash flow of 6.15% – it raised a few eyebrows (including my own).

If you’ve read our free eBook Can I Retire Yet, you’ll know that I’m a big proponent of the 4% rule. This is the rule of thumb that essentially says retirees can afford to withdraw 4% of their investment portfolio each year and not have their portfolio well run dry.

So that begs the question: How can we jump up to a 6.15% from our previous 4% rule of thumb? The answer lies in the annuity/tontine-esque aspects of the Purpose Longevity Pension Fund.

Ultimately, I’ve decided that while the Purpose Longevity Pension Fund is a very interesting product (really it’s part annuity, part pension plan, and part mutual fund) it really isn’t a great path forward for most people.

Are You Saving Enough for Retirement?

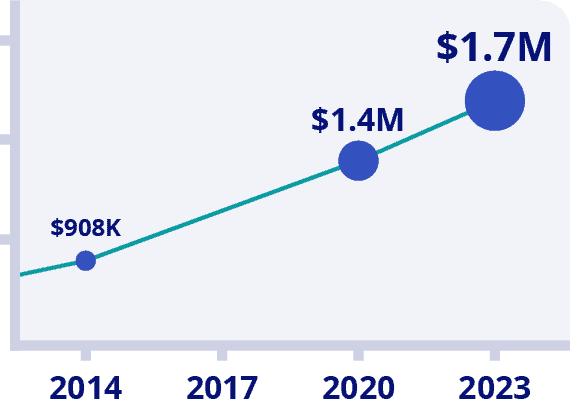

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

Quick Compare: Purpose Longevity Pension Fund vs Annuity vs Vanguard VRIF

It’s really hard to compare specifics across these products, but we’ll do our best when looking at it from the perspective of a 65-year-old looking out over the next 35 years.

| Purpose Longevity Pension Fund | Non-Guaranteed Annuity at 65 | Vanguard VRIF | |

| Targeted Investment Return | 3.5% | Varies widely. Not really relevant to the client, as they are guaranteed a certain payout in exchange for their principal. | 4.3% |

| Annual Money Yielded Into Your Bank Account as a % of Original Contribution | Hopefully 6.15% | 4-5% Depending on what conditions you attach to your specific annuity. | Varies based on market conditions. Will likely be quite close to 4% over the loooong term. |

| What happens if I pass away relatively young? | You get what is left of your original capital investment, but none of the investment returns that your money has generated. | Depends on specifics – but most annuity programs either say, “Thank you for your contributions” or they allow for some amount payable to a surviving spouse. | It’s 100% your investment – so whatever your last will and testament says, that’s what will be done with it. |

| Is the return guaranteed? | No | Yes | No |

| Management Fees | .6%-1.1% (mutual fund fee structure) | 1-3% – paid upfront and in annual fees that are pre-calculated into your promised payout. | .29% |

| Types of Investments | 47% stocks, 38% fixed income, and 15% alternative investments that include gold and commodities, picked investments by mutual fund manager (using mostly ETFs) | The amount of money to you is not really dependent on investments… but most annuity companies usually invest through stock-based mutual funds. | 45% stocks, 55% bonds, using Vanguard’s index ETFs |

How Does the Purpose Longevity Pension Fund Pay 6.15%?

The key to understanding how Purpose Longevity Pension Fund promises to pay out 6.15% while only getting 3.5% on their investment return is to factor in the part of the product that is similar to an annuity or tontine – the longevity risk pooling.

The idea at the heart of the annuity, the old-school tontine products, and the new Purpose Longevity Pension Fund is that we have no idea how long we are going to live – but we do know how long the average person like ourselves is going to live. We can therefore determine with relative (somewhat morbid) accuracy how much total amount of money the group of us will need to fund our lives between 65 and our final day.

So, if you want to manage your risk and create a safety net that won’t run out, annuities have traditionally made the value proposition of:

“Look, you want income for life? You want a pension? We can provide that to you. You will always have a cheque headed your way…”

“… but the other side of the coin is that you’re going to pay us a very healthy commission and annual fee for managing this whole thing, and if you pass away relatively young, your money stays with us – and that’s how we can afford to pay out a decent chunk of change to those who keep on living.”

We’re overdue for a super in-depth post on annuities here on MDJ – but I’ve been putting it off because it’s such a complicated topic. (2022 update: I’ve finally written it! see my investing in annuities guide here)

There are so many different factors to take into consideration when looking at crafting the right annuity deal for yourself. But for the purposes of understanding the Purpose Longevity Pension Fund, what you need to know is that Purpose has created a middle ground when it comes to this “pooling of risk”.

Essentially when you put money into the Purpose Longevity Pension Fund they’re going to keep track of two separate parts.

A) The original money you invested.

B) The investment returns that your money has gained.

The stream of money into your bank account each year (that is very likely to be 6.15% of your original invested amount even though it’s not guaranteed) is going to include some of “A” and some of “B”.

The key here is that when you pass away your estate will get back all of “A” that has not already been “paid back to you” over the course of your retirement.

HOWEVER – all of “B” that remains, will be left in the fund. In this way, there is a sort of annuity/tontine aspect to spreading the risk of longevity around all of the investors.

Example: Say you invest $200,000 in this new fund at age 65, with the aim of creating $12,300 per year in income for yourself. If after five years you were to pass away, the fund would not have returned a lot of your own money to you yet – perhaps in the neighborhood of $35,000 or so. In this situation, your estate would get $165,000 back from the fund, but any remaining investment income would stay in the mutual fund in order to continue paying other investors their 6.15% each year.

It’s an interesting middle ground in terms of balancing protection of original capital, but also protecting against the long shot that you might be the 1 in 500,000 that lives to be 110 and may outlive their portfolio.

But What If The Money Runs Out?

But What If the Money Runs Out?

Here’s what Purpose CEO Sam Seif had to say about the new product in various media and press releases:

It’s designed very simply, to take the best of what a defined benefit pension plan and an annuity would do, which is more certainty in matching an income stream to a person’s life term. You also get the flexibility of the mutual fund structure that is accessible and redeemable so you can buy at once, you can buy ongoing, or you can also redeem it.

The way the mechanics of the product work is if you put in your money, you’re going to get your income stream based on the yield of 6.15 percent every year (after you turn 65). And if after a number of years you pass away, or if you decide to redeem, what you get back is your unpaid capital. So, if you pass away, let’s say after five years, you’ll have a bunch of capital that you haven’t been paid back — you’ll get that money back or your estate will get it. So, you don’t lose that capital, it’s a really important point.

But at the same time, all the returns on your money stay in the pool for the benefit of all the individuals who continue to stay in the pool. What that does is it actually lowers the required return in the portfolio to generate a 6.15 percent yield for everybody. It only needs a net return of about 3.5 per cent on the assets in the pool to generate an over six per cent yield to all the individuals and more.

In regards to the assertion that the 6.15% payout might not be safe, Seif was quoted as saying:

We could actually be paying higher yields today, but we’ve chosen to take a more conservative bent. Those conservative assumptions mean that we have a higher probability of actually increasing distributions than anything else. Yes, there’s always a risk that you have to reduce the distributions if we had a very persistent negative return environment or something like that. But our view is that, because we’re not having to take so much risk in the portfolio, we shouldn’t see those types of things actually impact us negatively.

The fund is separate from Purpose, so Purpose is the manager. The fund would exist and we would just have another management run it thereafter if for any reason that was required. The manager is the manager of the pool, but the pool is set up with the benefit of all the individuals in the pool. So it has no impact if Purpose was to not be the manager or somebody else would become the manager.

The Purpose Longevity Pension Fund brochure promises: “No financial institution ever profits from investors passing away.” That seems to be true from everything I’ve read about it.

Purpose Longevity Pension Fund Review: Why It’s Not for Me

I see what Purpose is trying to do here and applaud them for recognizing a potential niche that needs to be filled. I just can’t wrap my head around the active management and high fees. It’s too high a price to pay for me to recommend it to people who are motivated enough to read a personal finance blog.

Now, my hope would be that this sets a new trend in the market and we see competitors enter and take those fees down. If we could come up with a robo-advisor-esque, passively-managed version of this that cost about .5% annually, I think I’d be all in.

I’ve always thought the idea behind annuities was really solid. So many people have pension envy when it comes to teacher or nurse pension plans (and hey – they are excellent perks, no doubt about that) but the truth about this plans is that when a person passes, only a fraction goes to their spouse, and when both halves of the pair are no longer with us, that money is gone.

If my wife and I were to have continued working as Canadian public school teachers for the next 30 years, and had 40+ years of paying thousands of dollars into our Teachers’ Pension Plan – and then tragically died at the age of 66 in a car crash – that money we paid into the Plan isn’t going to our family – it’s staying in the plan to pay other people. That’s the price of doing business if you want to maximize yield/return on your money, but also want guaranteed income for life.

That said, the amount of money taken out of the pot due to commissions and fees has always really bothered me when it comes to annuities. Not to mention there is a solid opportunity cost to committing and “locking in” all of that money instead of staying flexible.

The Purpose Longevity Pension Fund solves some of those problems and I believe that it will find a market. After one year, the fund’s actual holdings will become public information. Until then, all we know for sure is that the Purpose has stated investments would include: a conservative investment portfolio comprised of investments in a broad range of asset classes which may include fixed income, equity, derivative instruments, inflation sensitive securities and cash. The Fund’s ability to meet its investment objectives is dependent, in part, on the mortality of unitholders within each class and the investment returns achieved.

If Purpose sticks to broad-based ETFs and cuts their fees, they might create a fan in me yet. This would be especially true if you are a healthy 65-year-old that has a history of longevity in their family. (Nothing is written in stone, but it doesn’t hurt to play the odds!)

Until that cost reduction happens, the cost savings by understanding how to DIY your investment throughout your golden years is just too substantial to ignore.

The Vanguard Retirement Income ETF Portfolio (VRIF) represents an excellent alternative for 65-year-old-ish retirees who are looking for a very simple way to generate a relatively safe return over the long term – but still keeps 100% of control of their money with them.

Purchasing a unit of VRIF will spread your money out over thousands of safe government bonds and the bluest of blue-chip companies. You can see the ETF’s details here. Best of all, you get this conservative portfolio for a fee of only .29% ($29 on every $10,000 invested) each year.

To access the benefits of this product you simply open a Canadian discount brokerage account, and buy/sell this one ETF over and over again.

I've Completed My Million Dollar Journey. Let Me Guide You Through Yours!

Sign up below to get a copy of our free eBook: Can I Retire Yet?

Why hasn’t VRIF become popular? It’s only attracted 300M AUM over 3 years

Yeah I’m not 100% on that one either tbh Mark.

Thanks for the review Kyle. I like seeing these products because a number of my friends look for advice on retirement cash flow. I also agree that out of all the Canadian funds I’ve seen, the VRIF is the most attractive. I’d like to see more history behind this ETF, but the MER is in the right range and I trust Vanguard to find the numbers to make this sustainable. The product is not a fit for my current strategy which is primarily dividend growth, but if I die early I do want options that I can recommend to my wife.

Yeah it’s a good attempt at what an ideal product might look like. I hope it spurs more competitors! Like you, Vanguard has earned my trust over the years.