How Much Do Canadians Spend In Retirement?

You’d think it’d be a relatively easy quest to answer the question: How much will a Canadian spend in retirement?

When I set out to create the first retirement course for Canadians looking to retire in the next 25 years (or in the early stages of retirement) I figured that determining how much the average Canadians spent in retirement would be pretty straightforward. You can check out what that course has to offer by clicking here.

I also knew that it was quite important to get this information correct, as there is no way to answer the much more common question of, “How much money do I need to retire?” – without first having a pretty good idea of what retirement spending will look like.

Are You Saving Enough for Retirement?

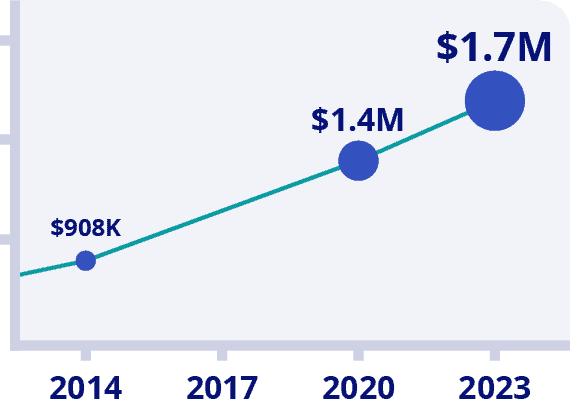

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

Figuring out how much you will spend in retirement is the key starting point to working backwards – and determining how much you’ll need in your nest egg when you retire. From there, we can get some idea of how much we should be saving each year to build up to that retirement nest egg goal.

Once you have a ballpark idea of what spending will look like, you can factor in your CPP, OAS, and possible pension income – then use the 4% rule to determine what your withdrawal rate for retirement should be.

Canadian Spending In Retirement – What the Experts Say

Before we get to how much you need to save and invest in order to retire comfortably in Canada, we need to know how to create a retirement spending plan that fits our unique profile.

Afterall, it doesn’t really matter what the average expenses in a Canadian retirement are, or how much the average Canadian has in their RRSP the day they retire – it’s really about your personal plan and your unique circumstances!

In order to guide your planning, I looked around for some useful rules of thumb. Because recent inflation will factor into some of these numbers that were created a few years ago, I will do my best to adjust for inflation. It’s key to remember that while overall inflation numbers have been high, the spending profile for most retirees doesn’t include things like shelter costs (if you own your own home).

Consequently, the effective inflation rate for most retirees will be a bit lower than the CPI numbers that you see in the news. Sure, grocery prices are up big time over the last five years – but gasoline, appliances, cell phone plans, and TVs haven’t really gone up at all over the last five years.

So it’s important to think logically about inflation and not emotionally react to one-off data points such as your latest grocery or restaurant bill.

Here are the best Canadian retirement spending “rules” and averages from reputable sources.

1) Jason Heath is an excellent fee-only CFP who has written extensively in several Canadian publications and is the Managing Director at Objective Financial Partners in Toronto. Back in 2019 he estimated the average retired couple probably spent a little more than the $31,332 Sun Life reported, and that spending would decrease by about 24% (pre-tax) for retired couples vs what they had spent immediately before retiring. Inflation-adjusted, that Sun Life number would be closer to $35,000.

2) The Canadian government’s Guaranteed Income Supplement (GIS) statistics show that roughly 37% of the Canadian seniors eligible for Old Age Supplement (OAS) – which is basically every senior who has lived in Canada for at least 15 years – are also eligible for GIS. That means that they are earning below the $21,768 threshold if they are a one-person household, and $28,752 if both partners form a two-person household.

Just as a thought experiment, I encourage you to talk to some of the folks collecting GIS, as I know several who are quite happy and live very fulfilling lives. (As well as a few that are not – to be fair.)

3) David Aston, a long-time personal finance writer in Canada wrote in 2020 that he believed a good rule of thumb was that Canadian retirees should look to replace 60% of their pre-tax salary if they wanted to enjoy the same standard of living they had created while working. He felt that number might be able to go down to 50% if you were a couple that had children, and was entering retirement with a mortgage-free house.

His final conclusion was that “a barebones but fulfilling middle-class retirement for a single person in Canada starts about $33,000 per year for a single, and $44,000 per year for couples.” Those numbers were for 65-year-old retirees who owned their own home. His middle-of-the-road retirement number for a couple was $65,000, and his affluent retirement number was $100,000 in annual spending.

If we adjust those numbers for inflation, it would look more like $36,000-$47,000 for barebones-but-fulfilling, $71,000 for middle-of-the-road, and $110,000 for affluent.

4) Perhaps the man most qualified to give answers to all things retirement money in Canada is Fred Vettese. Fred is the former VP and Chief Actuary of Morneau Shepell, and is a Fellow of the Canadian Institute of Actuaries (FCIA).

He has written numerous books and articles on Canadian retirement financial choices, and on a recent podcast episode he put the pre-tax salary replacement number at 40-50% and even mentioned several people he knew who were very happy in retirement only spending 30% of their pre-tax former earnings.

In his latest book (released in 2024) Vettese notes that Canadian seniors actually save a higher percentage of their income than younger Canadians do! He goes on to state:

“If we fail to acknowledge the true spending patterns of older retirees, political correctness may have something to do with it. The mere suggestion that older people don’t need quite as much money can come across as senior-bashing. But while it is a sensitive subject, I don’t think that justifies our shying away from the truth.”

Vettese then goes on to cite numerous studies from around the world that show spending decreasing as folks age into their 70s – and in many cases, net worths actually start to increase on average at this point!

Vettese also cites data from actuary Malcolm Hamilton, who found Canadian seniors on average were saving money, even while giving away an average of 16.1% of their income. That data was from way back in 2001 – but here’s the craziest thing: The average income for Canadian seniors went up 38% between 1998 and 2020 – AFTER we take inflation into account.

It’s worth making that 38% number crystal clear. That’s in “real” terms – meaning that inflation went up a certain percentage over those 22 years, and then the amount of money coming to senior citizens actually went up 38% MORE than that overall inflation number.

5) Nick Maggiulli wrote in 2022 from an American perspective that, “Across all wealth levels, 58 percent of retirees withdraw less than their investments earn, 26 percent withdraw up to the amount the portfolio earns, and 14 percent are drawing down principal.”

That’s an amazing statistic when you think about it. Most people who have a portfolio of investments as they enter retirement aren’t even touching the capital!

Maggiulli’s theory is that retirees will generally adjust their spending downward to match whatever income level that they feel forced to. Due to a lack of understanding of markets and probabilities, this leads to retirees spending much less than they could – or “should” if you want to take an optimization approach. I also recommend reading my previous article on safe withdrawal rates for retirement if you want even more proof of this concept.

For context, let’s toss in a few other random examples.

6) My friends Bryce and Kristy are retired in 2016 and traveled the world on about $40,000 per year. That’s all-in including medical insurance. Adjusting for inflation, it’s still well under $50,000.

7) Inspired by Bryce and Kristy, my wife and I actually semi-retired (we were no longer working 9-to-5 jobs) and traveled to Portugal, Thailand, Japan, Bali, and Los Angeles last year. We spent about $55,000 – and didn’t watch the budget all that closely.

8) Andrew Hallam has really opened my eyes to the possibilities of a retirement abroad, and he has written about folks who retire on between $300 and $500 per month (USD) in developing countries like Mexico. I did a deep dive into the best countries for Canadians to retire abroad in.

9) Finally, I talked to several recent retirees in my extended friends and family circle.

Now to give the full context, I grew up (and my family continues to live in) one of the lowest income parts of Canada. It’s a very rural part of the Canadian prairies, where well-maintained 1,300 sq. ft. bungalows can still be purchased for $230,000 or less.

Several family members stated that while they would miss their annual warm all-inclusive resort holiday during the winter months, they as a couple could live quite well on $35,000, even with recent inflation figures. Now these are folks who buy beef “by the side” and take pride in growing a vegetable garden, so perhaps it’s not realistic for many Canadians – I just thought it was another useful data point.

How Much Do You Need to Spend Per Month In Retirement?

It has been said before, but it bares repeating:

Personal finance is personal!

Consequently, my goal in providing the various estimates above were simply to give you some big, broad parameters.

Do I think it’s possible to retire in Canada spending less than $2,500 per month as a couple?

Yes.

Do I think it’s possible to retire in Canada spending less than $2,500 a month as a couple – while living in Toronto or Vancouver and not owning a mortgage-free home?

No.

There are several variables that only you will be able to answer when it comes to creating your ideal retirement scenario.

- Do you wish to rent or own? (Remember to factor in the maintenance and property taxes that come with owning.)

- Will you want to spend all of your year in Canada?

- What is your preferred entertainment budget?

- How much less will you spend on things like transportation, clothing, and office lunches if you’re no longer working?

- What role did children play in regards to your budget? Presumably they will no longer be a major budget item upon retiring.

- With income splitting, how much lower will your taxes be in retirement than they were before?

This is just scratching the surface when it comes to the variables associated with retirement spending, but I think the best starting point for most middle-class Canadians who own their own home is Vettese’s estimate of 40% of your pre-tax income over your last few years before retirement.

Most people tend to want the same lifestyle that they have grown accustomed to, so a percentage of your final few years before retiring makes sense to me. I used the lower end of the Vettese scale simply because I was pulled in that direction by the compelling evidence of so many retired Canadian couples spending less than $3,500 per month. Obviously, depending on what luxuries you want to add from that point – or what sort of increased spending your portfolio returns allow – you could adjust up from there.

The Retirement Spending “Smile”

Contrary to what many people would assume when it comes to retirement spending over the course of several decades, most people do not spend more as they age. David Blanchett released a landmark study in 2014 that detailed what he called the “retirement spending smile” and every retirement researcher that I’ve read has confirmed the idea.

Blanchett tells us that while people start out spending their full self-allotted budget in early retirement (the “go go Golden Years” as some call them), that spending dramatically falls as folks start to enter that 70-85 age range (the “slow go years”).

For the fortunate retirees who continue to add to the data after 85, the numbers do begin to creep up again, as medical expenses can begin to grow, but these are often referred to as the “no go years” for good reason – it’s pretty tough for most to take those dream vacations hiking Mount Kilimanjaro when they’re 91.

This spending pattern appears to hold true across countries and across the vast majority of income/net worth levels. And when you think about it, it kind of has an intuitive common sense feel to it, right?

Vettese has pointed out that most Canadian retirement spending doesn’t even keep up with inflation!

All that to say, I think the fear that most Canadians have of running out of money is perhaps out of proportion to the actual chances that it will happen.

Do I Have Enough and Am I Saving Enough to Retire in Canada?

Once you have an estimate of what your general lifestyle and spending pattern will look like in retirement, you can begin to put a plan in place.

Over the last year, I’ve helped hundreds of Canadians create their own retirement plan as part of my course: 4 Steps to a Worry-Free Retirement. You can save $50 by clicking the orange button below and entering in the code: MDJ50 when it asks for a coupon at checkout.

My course is learn at your own pace and includes dozens of helpful videos – as well as an optional workbook that you can download or print in order to help you create your own step-by-step retirement plan. You can see what the course looks like by clicking play on the video below.

FAQ About Retirement Spending in Canada

Retirement Spending vs Years In Retirement – The Happiness Tug of War

The full cost of continuing to work in order to add to your retirement nest egg is not obvious when you first think about it.

Sure, there is the added cost of maybe having two vehicles for a household, or maybe spending more on work-related wardrobe pieces.

But there is also the opportunity cost of not doing whatever you want for that time as well. Remember, you have finite time on this planet – and no one knows just how finite that time is.

By adjusting your retirement spending plans downward, we’ll see in the weeks to come the drastic effect this can have on the size of nest egg you need going into retirement.

The cost of not having large amounts of money available in retirement is easy to see: fewer holidays, older vehicles, maybe a semi-forced downsizing of your house. But the costs of endless, “one more year-ing” your way to a later retirement are less easy to envision. That doesn’t make their effect on your happiness any less real.

Some people love their jobs and want to work as long as they are capable – and that’s awesome. What an incredible position to be in! But that’s not most Canadian 55+ year-olds that I know.

While you’re trying to work out your individual number for spending in a Canadian retirement, check out this Ted Talk on the longest study on happiness, and this one on the surprising science of happiness. Then ask yourself if your retirement spending plan will make you the most happy – both in your final years of full-time employment and throughout your golden years.

Are You Saving Enough for Retirement?

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

I've Completed My Million Dollar Journey. Let Me Guide You Through Yours!

Sign up below to get a copy of our free eBook: Can I Retire Yet?

")

Hey there!

I actually spend less than $2000 per month while living as a single in Downtown Toronto. =)

Over the last 10 years I would spend about $21/22k per year on average.

Of course it does not include traveling (I count it separately). And during retirement I will also need to add the cost of out-of-pocket medical expenses (dental for the most part).

Sure there are many expensive condos (with their legendary condo fees) in Toronto, but we can still find older buildings with much better rates, even in Downtown TO.

Really appreciate that update Jacky! What a great data point. If you don’t mind me asking, what do you think would be a typical budget amongst your social group (many of whom I presume also live in Toronto)?

Hey Kyle, well I am an outlier I guess (as many people in the “FIRE” world). I save at least 50% of my income and stayed in the same building for more than 15 years now. I am also lucky to have No Frills/FreshCo nearby and to be within walking distance to my office. And as you may know our Toronto Public Library gives us access to many things (books, dvds, online access to various sites etc…). But most people I know here pay much more and live either in condos or outside the downtown core. I am sure they have never heard of FIRE though. =) So they definitely spend more than my $21/22k per year. For me its all about priorities (I prioritize travel and experience and my road to Financial Independence), being happy while being frugal, and keeping a positive attitude. And the financial markets do the rest. =)

Thanks Kyle for another insightful post. With inflation and the ongoing media doom and gloom, this was just what I needed to remember the big picture – especially as I enter my ‘work optional’ phase and figure out what I want to do in this next chapter. A couple of key takeaways that really hit home for me were #5 – Nick Maggiulli’s writing that only 14% of retirees are drawing down principal! Even though it’s based on American data, I bet it’s similar in Canada as well. My hunch is that this is characteristic of the Baby Boomer mentality that’s driving the ‘Great Wealth Transfer’. Most of the boomers I know are pretty frugal even though they’re sitting on mountains of savings. Coming out of multiple wars, that scarcity mindset has stayed with them, driving penny pinching behavior which will mean more money transferred to their X and Millennial children. I spoke with a financial planner this summer and he shared stories of wealthy retired clients with millions in the bank who worry about spending $10 on breakfast! Also, I really liked #7 and the share from Andrew Hallam’s post about people living on $300-$500 / month. While I’m not an extreme frugalist by nature, these types of stories at minimum open your eyes to different types of options for people who want to retire earlier but don’t necessarily have the savings to bankroll retirement in Canada. As a long time traveler, I definitely see more travel for me, especially to low cost countries like Mexico and Panama. In the Hallam post you shared, there’s a link comparing Panama to Dubai, and since I currently live in Dubai, it definitely caught my attention! Looking forward to your deep dive on low cost countries. We just bought a pre-build in Playa del Carmen, and I’ve been subscribed to International Living for some time. I’ve been curious the impact of inflation in the lower cost countries, so that’s one area I’m really interested to know more about as I haven’t really seen any posts about that on their site.

Isn’t that 14% figure wild?

I know Andrew has generally stated that International Living is a pretty good resource, so I’ve always read their stuff as well. I also know Andrew loves Panama and would recommend it to the vast maajority of people.

The thing with inflation in these low-cost countries is that I don’t think it will actually affect the average retiree there all that much. My theory is that most retirees there will likely not buy a home (although they obviously could), won’t buy a new vehicle, etc. I can’t imagine groceries going up all that much in a lot of these places – as long as you buy locally. But most of all, the number you’re starting from in terms of monthly expenses is just so much lower. So even if inflation averages 5% per year for 2022-2025 (doubtful), that’s 5% per year coming off of $2,000 per month in total expenses, as opposed to $4,000+ per month right?

We got married in that PdC area – loved it. I know it’s super popular with a lot of expats/digital nomads right now.