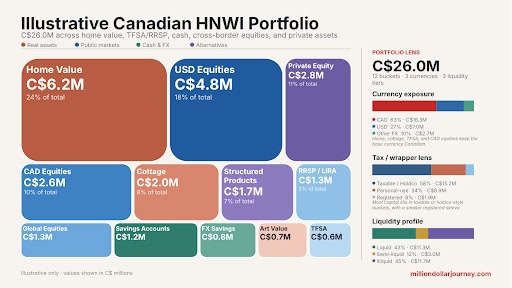

Investing For High Net Worth Individuals

A mistake many people tend to make is assuming that managing a high net worth portfolio is just a larger version of what worked prior. In reality, when you possess a lot of investible wealth, there are more considerations and options than previously.

In Canada, the label HNWI (high net worth individual) means someone with more than $1 million in liquid assets. If you qualify, that puts you in a fairly lucrative group, consisting of roughly just 2% of the country, or about one person in fifty.

That helps explain why we’ve been getting more questions about seven-figure portfolios, along with the oddball investments and complex products that rarely get pitched to someone still building a smaller nest egg.

If you’ve recently obtained high net worth status, make sure and do your homework before handing money over to financial institutions. I can guarantee you that you will be a target for their marketing teams going forward.

If you are looking for professional guidance you can have a glimpse at our best financial advisors in Canada list and understand why in your position, it is critical to use a fee-only advisor as opposed to a wealth manager taking chunks of your wealth every day at a time.

High Net Worth Investing Strategies

The best high net worth investing strategy, like any investing strategy, depends on your goals. If you’re a HNWI below retirement age, your goal is likely the same as any other investor: to maximize your returns over a long time horizon in order to secure a comfortable (or in your case, possibly luxurious?) retirement.

Being a high net worth individual, your retirement is likely quite secure already but you don’t become a high net worth individual by squandering the power of your money. Many HNWl’s want to use that money to generate high returns and increase their wealth.

High Net Worth Investing: Longterm, Diversified Investment

The optimal strategy for long term wealth generation is, in principle, the same for everyone: Assemble a basket of diversified investments at low fees and hold them for a long time. So if long term wealth generation is the goal, then my advice for high net worth individuals is the same as for any other passive investor: pursue a disciplined long-term investment strategy such as dividend investing or index investing.

These approaches ignore market noise and avoid short-term speculation, so you can play the long game and grow your assets more safely. Diversify your portfolio across industries, markets, geopolitical boundaries, and asset classes, rebalance once in a while, and hold on for the long haul.

Because HNWI portfolios are so large, it’s even more important to minimize fees. It can be worth thousands to chase after a few basis points in management fee savings. If you want to keep managing your own investments or use a robo-advisor service, pay even more attention to fund management fees. Even the tiniest percentage fee difference can translate into substantial savings.

In our latest Best Canadian Online Brokers Comparison, Qtrade came out on top, both in terms of its rock-bottom fees and its world class customer service.

One advantage of a larger portfolio is that you can carve out a small portion for strategies I would usually tell most investors to skip, not because they suddenly become safe, but because the rest of the portfolio can still do the heavy lifting. These include things like Private Equity investments, selling or buying options, engaging in commodity investing, and other niche investments.

I still think simple usually wins, even when the account balance gets big enough for the financial industry to start pitching you fancier ideas. Having access is the easy part, while sizing those positions properly and being able to clearly explain why it’s a better opportunity than any straightforward financial investment like shares or bonds.

High Net Worth Investing: Maximize Buying Power

Although the fundamental approach is the same for HNWI and everyone else, one small tweak to HNWI could be to keep more cash on the sidelines. This isn’t out of fear of being over invested, but rather to keep the buying power handy to take advantage of opportunities such as sudden market drops or business opportunities.

As an example, I missed a good chunk of the 2020 lockdown market crash because it took time to liquidate some assets and transfer between my accounts. If I’d had more cash on hand, I could have bought more aggressively into the market dip. I didn’t have much cash ready and missed much of the roaring growth after the March 2020 market crash.

While a large portion of your investments should be in equities, I recommend keeping 15% to 30% in cash so you can jump on chances to buy aggressively into a market crash or other opportunities. This is the best approach for building high net worth asset allocation over time.

High Net Worth Investing Strategies for Different Goals

Having a high net worth gives you the financial freedom and security to try different things and have different goals. Say a big part of your portfolio is already dedicated to long term wealth generation, then you can afford to invest the rest of your wealth in fun and creative ways.

If you want more excitement in your portfolio and are willing to take on more risk, you can dedicate a portion to more speculative investments like collectibles or commodities.

Do you have an interest in vintage sports cards, comic books, or art? Maybe those interests can be channeled into a side trading hobby. Have fun and make profit at the same time. See our guide on Collectible Investing In Canada for more ideas.

How about commodities? If you are interested in analyzing economics and predicting global resource supply and demand, you can try your hand at commodities speculation. See our guide on How to Invest in Commodities in Canada for more details.

Everything is best enjoyed in moderation, even fun. Please only use a small portion of your overall wealth for speculative investments like collectibles and commodities.

High Net Worth Investing After Retirement

Congratulations on retiring with a big nest egg! My typical recommendation for retirees is to gradually transition their equity asset allocation to safer investments like bonds, GICs, and high interest saving accounts.

The same recommendation applies to high net worth individuals too, but only up to the point where the safe portion of the portfolio guarantees a comfortable retirement lifestyle. That is, if the low risk bonds in your portfolio already give you enough interest income to sustain the retirement you want, then there is no need to transition more of your equity holdings into safer fixed income investments. Leave the equity assets to grow so you can maximize your estate, which can be left to heirs or to charity.

Are You Saving Enough for Retirement?

Answer your retirement savings questions with 4 Steps to a Worry-Free Retirement. The first online course for Canadian retirement.

Visit Now & Get $50 Free (Code MDJ50)

High Net Worth Portfolio Management

This article focused mostly on DIY investment styles and strategies, but of course, I know there are plenty of professional money managers out there ready to help you manage your portfolio. After seeing just how many truly bad financial planners there are there in Canada, I recommend Objective Financial Planners out of Toronto.

Jason Heath is the founder and you can Google his name to see how well trusted he is all over Canada. The also have a lot of experience doing online financial planning so you can get help wherever you live and never have to change out of your PJs!

There is also no shortage of hedge funds out there that would be happy to sign up a high net worth client. Their promises of high returns can be very tantalizing. However, I don’t recommend hedge funds to main street investors, nor do I recommend them to high net worth investors. Their high fees simply cannot be justified.

It’s incredible how many hedge funds can get away with outrageous management fees for weak performance not even close to returns from simple index funds. Sure, the very top hedge funds can outperform the overall market index; some funds even do so with some consistency. But hindsight is twenty-twenty.

The chances of finding the lucky fund that consistently outperforms the market is very low. In the meanwhile, it’s not worth the high fees to search for that rare, consistently high-performing hedge fund.

Working with a Financial Planner as a High Net Worth Individual

For high net worth individuals in Canada, the role of a financial planner extends far beyond the realm of basic asset management. These experts offer nuanced, all-encompassing services that address the multifaceted aspects of wealth.

This can include devising sophisticated estate plans that guarantee a seamless transition of assets to future generations, to implementing advanced tax strategies aimed at significantly reducing fiscal burdens.

A financial planner can customize your investment portfolio to align perfectly with your unique risk appetite and financial aspirations, ensuring each investment decision is meticulously calibrated for optimal performance.

Additionally, financial planners provide invaluable guidance on charitable giving, enabling high net worth individuals to support causes dear to them in a manner that is both impactful and tax-efficient. This strategic philanthropy not only furthers social good but also enhances the individual’s legacy, intertwining their wealth with broader societal benefits.

For those with interests and assets that span across borders, the planner’s role becomes even more critical. They offer expert advice on managing international investments and navigating the complex web of global tax laws, ensuring that your wealth is not only safeguarded but also positioned for growth in the international arena.

By tapping into the expertise of a financial planner, high net worth individuals in Canada can unlock the full potential of their wealth, leveraging it not just for personal gain but as a powerful tool for generational wealth transfer, philanthropic endeavors, and global investment opportunities.

A financial planner can help HNWIs ensure that their wealth is not merely preserved, but also serves as a dynamic force for positive impact, both now and in the future.

Create a Real Portfolio Hedge

When most investors hear the word “hedge” they immediately think of hedge funds, or other investments that seem clever, complicated and only reserved only for folks with millions to invest.

The real issue is often a lot simpler. If you need to hedge against uncertain scenarios, it may mean your portfolio is too concentrated on certain assets. The first obvious fix is to increase the level of asset allocation diversification, look at the various components within it, and how correlated they are between themselves.

I am somewhat in favour (especially when it comes to a larger size portfolio of HNWIs) of sacrificing some potential gains in exchange for risk minimization. Hence, I would buy into an asset that behaves differently than the broader market, even if I think its prospects are less promising over the long term than those of my “core investments.”

Given those goals, I wouldn’t start with hedge funds. Many of them still move too closely with the public markets they are supposed to offset, which means the promised protection is usually thinner than investors expect. Beta, which is just a measure of how closely an asset moves with the broader market, is often high enough that the hedge is only partial at best (if any at all). In other words, when folks panic, hedge funds aren’t going to protect as much as one might think.

I’d venture to say something similar about Bitcoin, and about a fair bit of the commodity space as well, because once risk assets start falling together with the market, it is not much of a hedge at all.

The options that strike me as a genuine hedge, are less elegant on paper. Real estate is one example, even though I am not naturally drawn to it as an investment because it is illiquid, the returns are often not that exciting, and I still see more long-run upside in technology. In spite of that, in an inflation-heavy environment, or a doomsday scenario for the financial system, real estate can do a respectable job of preserving wealth.

Owning a business in a sector with inelastic demand can also be a real hedge. If customers still need what you sell in a recession, and prices can rise with inflation, the income stream remains unharmed.

I have also seen some niche allocations to rare industrial materials, and I understand the appeal. Their prices are driven more by supply, demand, and geopolitics and as such they are one of few areas which are function-driven rather than speculation-driven. That does not make them safe (far from it), or stable (they are extremely volatile) – but they do serve a certain purpose in larger portfolios.

Selling Options as a Way to Make Extra Income

Selling options is often pitched to high net worth investors as a clever way to create “safe income,” (which is usually when I start getting suspicious). There are theoretical ways to make an income on options if you stop thinking about them as a way to gamble (“speculate”) and start treating them as a disciplined way to get paid for taking risks you already wanted.

Many investors read about investing in options and picture easy premium, steady cash flow, maybe a little financial engineering on top of a blue chip stock portfolio. In practice, the relatively safe version of options trading is much narrower. For most wealthy investors, it comes down to two strategies: covered calls on stocks you already own, and cash secured puts on stocks you would be happy to buy anyway.

Selling an option means you are taking on an obligation in exchange for cash today. The buyer gets a right, you get a premium (a relatively small amount of guaranteed cash). That sounds attractive, and sometimes it is, but the premium is not free money. It is compensation for giving up some upside, or for agreeing to buy into a decline.

A lot of the bad advice in this area leans on the idea that “most options expire worthless,” as if that proves sellers have an edge. The actual CBOE data is more interesting. Only about 30% to 35% of options expire worthless, while roughly 55% to 60% are closed before expiration, and only about 10% get exercised. So the simple story people tell themselves is not really the story of how the market works.

But the key thing to remember is that you aren’t trying to win some bet on Polymarket or Kalshi. You are trying to use option pricing to improve the terms on positions you already understand. If you would not happily own the stock, or if you would be upset selling it at the strike price, the strategy is probably wrong for you no matter how “safe” the premium looks.

Covered calls are the cleaner starting point. For example, you own 100 shares of a stock, then sell a call option with a strike price above the current market price. In exchange, you collect premium income. If the stock stays below the strike, you keep the shares and the premium. If it rises above the strike, your shares may get called away at that preset price.

I get why this appeals to people, especially HNWIs sitting on large appreciated positions that already throw off dividends. If you own, say, 2,000 shares of Royal Bank and would be perfectly content selling part of that stake at a higher price, writing calls against a portion of the position can add income without changing your overall plan very much.

The tradeoff is simple: you get cash now, you cap some upside later. It’s the manual version of those covered call ETFs that appear to be all the rage these days (but actually aren’t a very good deal).

Cash secured puts are the mirror image, and in some ways I think they are the more useful tool. You set aside enough cash to buy 100 shares at the strike price, then sell the put. If the stock stays above that level, the option expires and you keep the premium. If the stock falls below it, you buy the shares at an effective discount once the premium is included.

That structure is much safer than naked put selling (which I would not describe as conservative in any normal-person sense of the word), because the purchase money is already there. For an HNWI with a large cash allocation, this can function like a limit order that pays you while you wait. If you wanted to buy Brookfield, CN Rail, or an ETF at a lower price anyway, getting paid to set that willingness in advance is not a bad deal.

There is some real evidence that income can be meaningful. The S&P 500 Daily Covered Call Index posted an annualized yield of 9.90% from inception through December 31, 2025, and its total return from December 18, 2023 through the end of 2025 was 17.34% on a NAV basis.

For most wealthy investors, the practical takeaway is: Sell covered calls only on positions you would genuinely sell anyway. Sell cash secured puts only on positions you would be happy to own at a given price point no matter what. Keep position sizes modest relative to your overall portfolio, use liquid names, and do this in tax sheltered accounts (such as your RRSP or TFSA) where possible.

High Net Worth Investing For Canadians – FAQ

High Net Worth Investing in Canada: Conclusion

Achieving HNWI status doesn’t flip the investing script – fundamentals don’t change just because you hit a certain number – whether your net worth is a cool grand or a hefty million. Sticking to a diversified spread, think ETF portfolios, for the long haul remains your best bet for building wealth.

There are, however, a few ways for high net worth individuals to fine-tune their approach for that extra edge: Before you hit those golden retirement years, make sure you have an RRSP and TFSA withdrawal plan ready to minimize taxes and max out your OAS.

Once again, it bears repeating that banks and insurance companies really love to soak Canadian high net worth individuals for as much as they can. By charging seemingly small fees (2.5% doesn’t sound like a lot right?) they can wreak havoc on long-term returns.

Finding a wealth management company that doesn’t charge a commission percentage – but rather a set transparent fee – is even more for HNWIs because 2%+ of their portfolio can be a pretty massive chunk of money to give up each year!

Hello,

I work with several advisors and people in the HNW range.

All of the advisors require $2mm to qualify unless you have some other connection to get in. Many are “culling” their smaller accounts to keep the client size manageable.

Thank you for the regular and helpful emails that address so many investment topics. My question is about your thoughts on having cash available for market dips as you illustrated. I have also read here and elsewhere that it is best to stay invested and not to try to time the market. Can you please clarify both positions ie: regular investing vs saving for market sales. Thank you.

Clyde