Financial Freedom Update Oct 2022 Update ($73k in Dividend Income!)

Welcome to the Million Dollar Journey Oct 2022 Financial Freedom Update – the third update of the year! If you would like to follow my whole financial journey, you can get my updates sent directly to your email, via Twitter and/or Facebook.

For those of you new here, since achieving $1M in net worth in June 2014 (age 35), I have shifted my focus to achieving financial independence. How? To build my passive income sources to the point where they are enough to cover our family expenses. Mostly through passive and tax-efficient dividend investing.

Here is a little more detail on our passive income goals:

How it all started – Original Financial Goal

I always find it interesting looking back at previous goals. Here was the big goal after hitting the Million Dollar Net Worth milestone:

Our current annual recurring expenses are in the $55k range (after-tax), but that’s without vacation costs (and no mortgage payments). However, while travel is important to us, it is something that we consider discretionary (and frankly, a luxury). If money ever becomes tight, we could cut vacation for the year. In light of this, our ultimate goal for passive income is to have enough to cover recurring expenses, and for business (or other active) income to cover luxuries such as travel, savings for a new/used car, and simply extra cash flow.

Major Financial Goal: To generate $60,000/year (after-tax) in passive income by end of the year 2020 (age 41).

Reaching this goal would mean that my family (2 adults and 2 children) could live comfortably without relying on full-time salaries (most recently a one-income family). At that point, I would have the choice to leave full-time work and allow me to focus my efforts on other interests, hobbies, and entrepreneurial pursuits.

Achieving Financial Freedom: You may be thinking, 2020 is long gone – what has happened since then? I’m happy to report that we reached financial independence in 2020 – a little ahead of schedule. While the goal now is to continue building and reinvesting those dividends within the portfolio I’m finding that as the years go by, more focus is being put on indexing. Having said that, I haven’t sold any dividend positions in favour of index ETFs… yet. Find out below how much our passive income has grown since 2020!

Financial Independence Update – Oct 2022

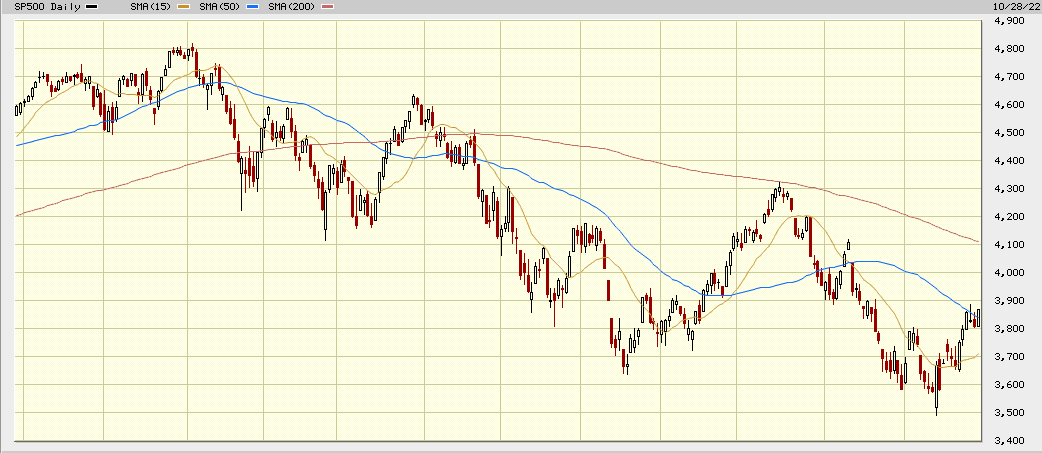

All investors can agree on one word when it comes to the markets this year – volatile! In the last update (in June), the S&P500 made new yearly lows, but started to climb back in August. The index took the opportunity to sell off some more to make new lows in early October. There is currently some buying, but is this the bottom? Who knows! What I see is that this is a great opportunity for investors who are currently in the accumulation phase.

What’s causing the volatility? The biggest factors are likely inflation, tightening of money supply and higher interest rates. In addition, big-tech earnings are not impressing the market either which is causing some super mega-cap stocks (like Facebook) to take a dive.

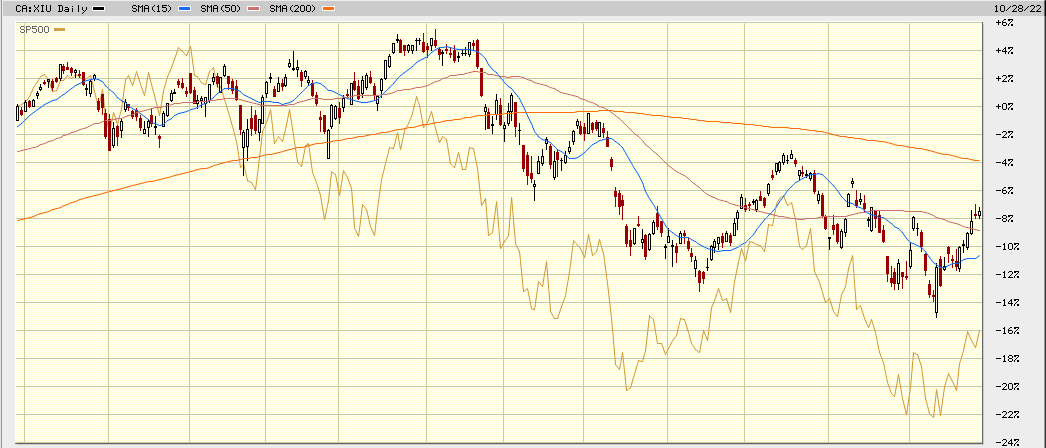

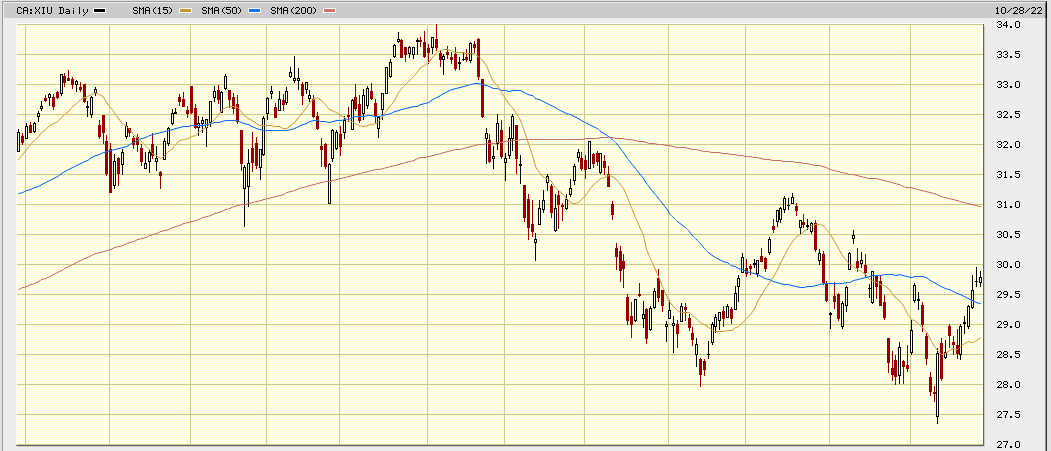

These factors have resulted in a rotation from risk (ie. technology) to more boring defensive stocks (ie. mostly blue-chip dividend stocks) and commodities (due to oil supply, and higher inflation). This is one of the reasons why the TSX has held up so well this year versus the S&P500.

In November of 2021, the S&P500 (an index of the largest 500 companies in the US) was floating around 4600. By June 2022, the S&P500 lows hit around 3650. Since the update in June, the correction has continued making new lows (3600 earlier this month). As of this post, the S&P500 is trading at around 3860.

Could this be a pit stop to build some energy before moving higher? Or perhaps the beginning of a larger correction? Only time will tell! In any event, I’m a believer in staying invested over the long-term which historically has proven to be fruitful for patient investors – myself included!

Not including dividends, the S&P500 (as shown above) has declined about 16% year to date (YTD). While the TSX has been relatively strong, it has started succumbing to the pressure and has declined about 8% (YTD).

While the extreme market returns are great for portfolio growth, it’s healthy for markets to take a bit of a break – especially for investors still in the early days of accumulation.

How often and when do I make the decision to buy? I like to buy quality dividend companies (and indexes) when their valuations are attractive. In other words, when they are being sold off (ie. dip). You can see some of my favourite Canadian dividend stocks here.

As I’ve mentioned in previous updates, I’ve left full-time salaried work which means I’m spending those dividends that I’ve grown and nurtured over the last 15+ years. As a result, my investment cash position has dwindled down over the years, so no more large investment purchases – at least for now!

Most of the portfolio additions are driven by reinvesting those growing dividends. Thus far in 2022, I have deployed modest amounts of capital into the following Canadian dividend positions:

- Sunlife (SLF)

- Suncor (SU)

- Canadian Natural Resources (CNQ)

- Fortis (FTS)

- Royal Bank (RY)

- Telus (T)

- Waste Connections (WCN)

- Brookfield Infrastructure (BIP.UN/BIPC)

- Algonquin Power & Utilities (AQN)

- Index ETFs (not quite dividend stocks, but they are likely included in the indexes!)

The goal of the dividend growth strategy is to pick strong companies with a long track record of dividend increases. Since the last update, there have been more dividend increases – check them out below.

2022 Dividend Raises

Thus far in 2022, the Canadian portion of my portfolio has received dividend raises from:

- CU.TO (1% increase)

- MRU.TO (10% increase)

- CNR.TO (19% increase!)

- BIP.UN/BIPC (6% increase)

- CNQ.TO (27% increase!)

- NTR.TO (4% increase)

- BCE.TO (5.1% increase)

- BEPC.TO (5% increase)

- TRP.TO (3.4% increase)

- ENGH.TO (15.6% increase!)

- TRI.TO (10% increase)

- T.TO (7% increase)

- SU.TO (12% increase)

- L.TO (11% increase)

- WN.TO (10% increase)

- AQN.TO (6% increase)

- SLF.TO (4.5% increase)

- FTT.TO (4.9% increase)

- BNS.TO (3% increase)

- BMO.TO (4.5% increase)

- CM.TO (3.1% increase)

- RY.TO (6.7% increase)

- NA.TO (5.7% increase)

- H.TO (5% increase)

- EMP.A (10% increase)

- FTS.TO (5.6% increase)

- NWC.TO (2.7% increase)

- EMA.TO (4.1% increase)

Top 10 Holdings

Our top 10 holdings move around quite a bit. This time around, it’s a good mix of industrials, infrastructure, utilities, and the big banks.

In our overall portfolio, here are the current top 10 largest dividend holdings:

- Canadian National Railway (CNR)

- TD Bank (TD)

- Royal Bank (RY)

- Brookfield Infrastructure (BIPC/BIP.UN)

- Fortis (FTS)

- Bank of Montreal (BMO)

- Enbridge (ENB)

- Telus (T)

- CIBC (CM)

- Nutrien (NTR)

*not counting index ETFs (they are my largest holding).

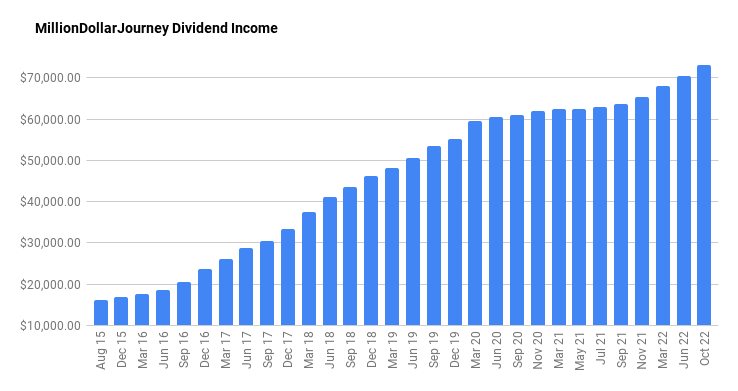

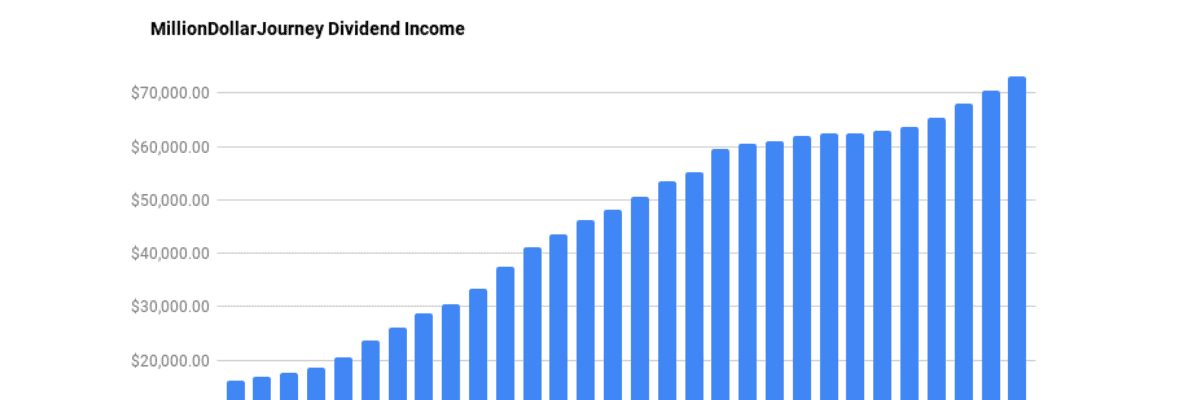

Dividend Income Update

As mentioned, there have been a number of healthy dividend increases and we managed to deploy some capital into dividend stocks.

As you can see in the chart below, the dividend increases have really made a difference in increasing our forward annual dividend income to $73,000. Given enough time for portfolios to compound, slow and steady does work!

The dividends are counted from all of our family accounts including non-registered (including leveraged account via the Smith Manoeuvre), RRSPs, corporate investment account, and TFSAs.

Final Thoughts

For a number of years, these updates have been during a pure bull market. Now 2022 has an entirely different tune, particularly in the US and global markets. Canada, on the other hand, has been a pleasant surprise by showing relative strength in these market conditions – at least for now. Regardless of market conditions, the dividends keep rolling in, and the last few quarters have been especially satisfying due to the noticeable bumps in the dividend graph above. This is one of the major benefits of dividends for retirees – getting paid regardless of the markets being up or down!

I’ve noticed that other dividend investors/bloggers are comparing their dividend income to a comparable income/hr. $73k/year equates to about $36.50/hr in passive income (based on a 40-hour work week), and depending on how the investments are structured, most of that can be tax-free!

I wrote a post about withdrawing from your RRSP or TFSA where, with no other income in retirement, you can make up to $50k in dividend income (within a taxable investment account) and pay very little to no income tax (depending on the province). The benefits are even greater if you can split the dividend income with a partner/spouse.

If you are also interested in the dividend growth strategy, here is a post on how to build a dividend portfolio. With this list, you’ll get a general idea of the names that I’ve been adding to my portfolios.

If you want a simpler investing strategy that outperforms most mutual funds out there, check out my post on the best all-in-one ETFs in Canada. I’m a fan of indexing as the iShares XAW is my top individual holding.

Keep investing that cash flow and stick with a long-term plan. Your future wealthier self (sooner than you think!) will thank you for it.

May I ask your net worth as of today? I have been following your posts for a very long time but haven’t looked in a little while