Retirement Calculators – How Much Do You Need to Retire?

This popular article was originally written in 2017, but since then, a couple of the calculators have gone offline. I have updated this article with a couple of new additions. Enjoy!

A reader recently asked me if she had saved enough for retirement. While it seems like a challenging question to answer, it can be roughly calculated via online calculators providing that you have fairly accurate inputs.

Are You Saving Enough for Retirement?

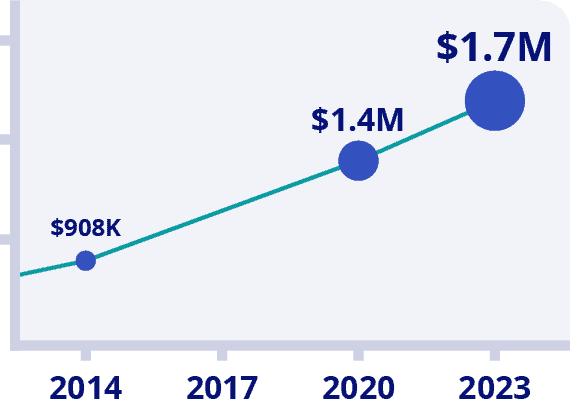

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

Generally, here’s what you’ll need for any online retirement calculator:

Expenses

Some online calculators will take your expected retirement expenses as a percentage of your gross income. Many financial institutions will tell you that you need at least 80% of your income to live a comfortable retirement.

However, if you run your actual expenses, you’ll likely discover that you need much less than 80% of your pre-retirement income. From my research, 50-60% of your pre-retirement income is reasonable – but only if you are retiring with no debt which I think every retiree should be going for. When I ran the numbers for our family, 55% of our pre-retirement income was enough to maintain our lifestyle during retirement.

Canada Pension Plan (CPP) and Old Age Security (OAS)

Most people have no idea what they should receive for both CPP and OAS (me included!). To get an accurate amount, you can obtain your CPP statement online. Otherwise, there are calculators that can estimate your CPP based on your career income. The first calculator below is offered by the federal government and will help provide an estimate of both CPP and OAS.

Total of your Assets

If you regularly track your net worth, then you’ll have the totals of all of your assets. Most importantly, the total of your RRSP, TFSA, and non-registered accounts. You’ll need this info for pretty much any retirement income calculator.

5 Useful Retirement Income Calculators

In my search for a retirement income calculator, I had a hard time finding the perfect calculator.. at least perfect for me. Each had their merits but also some serious drawbacks.

1. Mawer Retirement Calculator

I came across this free calculator when looking for replacements for both ES planner and Retirement Advisor (both no longer work). Mawer is known for its reasonably priced mutual funds and is very popular among investors.

I must say that I was impressed with this calculator due to its ease of use, and the ability to add a spouse right away. It also allowed me to enter a retirement age before age 50 which was an added bonus. Personally, I like seeing numbers by year to see where the money is coming from. Mawer does a good job at summarizing the results, but a little more detail would be appreciated!

This is among my favorites of the batch!

Highlights

- Separate accounts for you and spouse/partner

- Allows you to estimate your own CPP/OAS rather than make assumptions

- Calculates net worth at death

- Income tables by year

- Allows you to modify income requirements on the fly and even show you the maximum you can withdraw and die with $0 in accounts (assuming you live until 89)

- Allows you to add whatever additional income sources that you wish, such as business income.

Drawbacks

- Cannot add home as an asset

- More details would be appreciated for the income table by year. Such as how each income source would be drawn down over time.

2. Canadian Government Retirement Calculator

In my search, this was the first retirement calculator that I came across and was actually surprised that it was created by the federal government. This calculator is pretty thorough with government benefits but lacks in some areas such as adding a spouse, non-registered assets and general taxation. The biggest weakness is for the extreme early retirement crowd, the earliest age for retirement in this calculator is age 50.

Highlights

- Calculates OAS and CPP – with the ability to customize. Also provides average monthly amounts for Canadians (which can be helpful) and adjusts based on how early you start taking CPP

- I like how it graphically shows income by age and impact of CPP and OAS on retirement

Drawbacks

- Neglects non-registered accounts, needs to account for taxation in retirement

- No ability to add spousal assets (I just used total family RRSP, TFSA etc)

- Earliest retirement age is 50

- Doesn’t show ending balance of accounts at death

3. BMO Retirement Calculator

This calculator is what you can expect from a big bank. Very skimpy on details, but very pretty to look at. However, out of the big bank calculators that I used, I liked the BMO product the best. It was very easy to use and allowed me to input spousal financial information.

What was also refreshing was that I was able to enter any retirement age – unlike the calculators above – and my own number for my expenses. The downside is as mentioned above, very little detail in the final report and no ability to customize CPP/OAS. As a side note, CPP will likely be much lower for an extremely early retiree due to a high number of low contribution years before the age of 60.

Highlights

- Asks straight up how much I need for retirement

- Includes spousal assets

- Allows for early retirement projections

- Intuitive graph and allows for revisions to inputs to model different scenarios

- Calculates net worth at death

Drawbacks

- Needs table that shows income by year – lacks detail

- Cannot customize CPP/OAS

4. Sheffar Potter Muchan/Dinkytown Retirement Calculator

This is a fairly bare-bones calculator that lets you enter everything on one screen (which I like). It accounts for early retirement, and you can enter your own values for the rate of return before/after retirement. I also appreciated the detailed table that breaks down income sources during retirement. The biggest downside that I could see is that you cannot add spousal assets.

Highlights

- Very straight forward, enter everything on one screen.

- Allows for early retirement projections

- Intuitive graph and detailed tables that shows income sources during retirement

- Calculates net worth at death

Drawbacks

- Does not include spousal assets

- Cannot add home as an asset

- Does not allow for business income during retirement

- Cannot customize age to start benefit of a company pension plan (assumes retirement age)

5. DIY Rough Back of a Napkin Calculator

In the archives, I wrote about how to quickly calculate what you need for retirement:

- Work out a budget of expected expenses during retirement. Don’t forget to include income taxes, albeit reduced, as an expense.

- Calculate how much the Government will provide you during your retirement years. You can use the Canadian government calculator here.

- The difference between 1 and 2 is how much income from savings (and/or company pension) that you will need.

- Take the number calculated in step 3, and multiply by 25. That is the amount you will need to have saved (in todays dollars). If you have other sources of income, like from company pensions or rental properties, then reduce step 3 by the other income amounts, then multiply by 25.

This quick calculation is really for traditional retirement age (60+) where government programs can really pay for a significant portion of your retirement needs. Once you calculate your “number”, you can figure out how much you need to save today with the following table:

Monthly Savings Required to Reach Your Number (Assuming 4% real-return growth rate)

Required Savings Monthly Savings (retire in 25 yrs) Monthly Savings (30 years) Monthly Savings (35 yrs) Monthly Savings (40 yrs) $200,000 $389 $288 $219 $169 $300,000 $583 $432 $328 $254 $400,000 $778 $577 $438 $339 $500,000 $973 $721 $578 $423 $600,000 $1167 $865 $657 $508 $700,000 $1362 $1009 $766 $593 $800,000 $1556 $1153 $876 $677 $900,000 $1751 $1297 $985 $762 $1,000,000 $1945 $1441 $1095 $846

This is obviously a very quick and rough calculation. If you want the down and dirty details, you can read them in my article “retiring early in Canada” and discover that you may not need as much as you think.

The Perfect Calculator?

I’m sure that financial planners have access to powerful modeling tools for a variety of situations. However, I’ve yet to come by a calculator that handles everything that I need. My idea of a perfect retirement income calculator would have the ability to:

- Include partner/spouse assets in the calculation;

- Include contributions to RRSP, TFSA and non-registered accounts for both spouses;

- Have a field for anticipated monthly expenses during retirement;

- Include expected business/rental income during retirement;

- Income home as an asset;

- Choose your own retirement age;

- Include a field for estimated CPP/OAS during retirement and when you want to start taking it (for extremely early retirees, CPP will be lower due to a higher number of low-income years);

- The ability to manipulate to choose which account to draw down first (here are some of my retirement account drawdown strategies);

- Account for taxation of different accounts and ability to set the tax rate for each account. When you start drawing down from your RRSP for example, it will be taxable at your marginal rate. When you draw from a TFSA, withdrawals are tax-free. However, when you draw from a non-registered account, it’s tax-free when you withdraw, but you may have to sell to generate the cash to withdraw.

- A detailed table (by year) showing the drawdown from each income source, the balance remaining in each account, and final net worth at death.

Final Thoughts

There you have five of my favourite retirement calculators. None of them are perfect, but the product from Mawer comes the closest. Give them all a try if you can and let me know what you think. If you are interested, check out my financial freedom updates here.

Are You Saving Enough for Retirement?

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

I've Completed My Million Dollar Journey. Let Me Guide You Through Yours!

Sign up below to get a copy of our free eBook: Can I Retire Yet?

Great article and comments BUT, I’ve yet to find a calculator that takes into account the diferent ages and hence the diferent age of retirements for spouses. My wife is 10 years younger and eager to work until 60 at which time I’ll be 70. Right now I’m into forced retirement at 57 so working part time. Also needed is the correct calculations so that both spouses can work out the CPP payable taking into account the dropouts. I could use a calculator that takes all this into account so I can be sure of when I can stop working PT and when I can start drawing from my RRSP and CPP. Wife will have Defined Benefit Pension. Anything out there? Right now, I’m getting pretty skilled with Excel… Retirement project may be publishing my own calculator. :)

Hi Bruce – did you get to putting an Excel sheet together that you could share? Thanks a bunch.

The CRA site is the only one that accounts for a defined benefit pension that has a bridging amount between retirement and 65 (perhaps because all the other sites are trying to sell you mutual funds or RRSP loans?). You can sort of fudge your spouses numbers by their CPP/OAS as “other pensions” however every income source (including those fudged ones) seems to be considered taxable as far as OAS clawback calculation though, even TFSAs or reverse mortgage income.

The Mawer calculator goes wonky if you put a revised income amount at the end – the first entered amount stays ok but put in anything over 100k as revised it goes to 136,678 ? ( :) ), revised = 99,999 seems to work though.

Then there’s my Real Quick Back of Napkin Calculator ( RQBNC -TM pending) (with the caveat that you need to know your annual expenses preferably over many years – really a lifestyle cost )

Take your total saved amount (RRSP, TFSA, non-reg etc.)

divide by annual expenses

add that number to your age

if > 95 (100? or expected age of demise) – you’re good to go

< 95 – keep working/saving /change lifestyle

if you have a paid off place to live that's a bonus safety net and will leave something for your heirs to squabble about.

examples:

– saved $1,000,000 expenses are $40,000/year and you are age 50

= 25 + 50 is < 95 – nope – something has to change

– saved $2,000,000 /$40K/ age 50 = 50 + 50 = 100 – done like dinner; open a cold one

YMMV

Thanks for the heads up, I will check out that bug and test it as well. I have not heard of that “95” rule. Putting it in practice seems a little conservative – especially if you plan on retiring early.

Say for example, a 65 year old couple with, $1M saved and $60k in expenses. If they worked, their CPP/OAS combination could already be $30k of those expenses, and $1M should easily be able to cover the remainng $30k. But according to the 95 rule, they are not ready ($1M/60k+65=81.7).

Maybe the 95 rule is for single people only? It’s a little too simplistic to me as it doesn’t count for other variables like OAS/CPP and pension income.

the Real Quick Back of Napkin Calculator is a bit (lot) tongue in cheek – I wouldn’t use it as a sole decision maker – the “95” is anticipated date of demise as mentioned – pick whatever number suits you- it is also a VERY conservative “calculator”.

yes government income supplements are not factored in – but do you know for sure that they will be there? – CPP probably will be around but be aware that there is factoring for years where there is no income eligible for CPP deduction hence CPP contributions – I ran in this because for a large number of years my private corporation paid me in dividends (not ’employment income’) hence no CPP contributions which ultimately reduced CPP payout – something that someone who FIREs s/b aware of because there will a large of non-employment income years.

Very good points. Business owners who get paid by dividends would need to run projections with a low amount of CPP. Also note though that CPP allows a certain number of low-income/no-income years that can be omitted from the CPP calculation.

I also believe that CPP will be in existence for some time to come. As for OAS, I can see the age requirement (65 to 67 etc) moving to a more sustainable model, but it would be political suicide to remove it completely.

ESPlanner basic calculator is now also unavailable.

Looks like they are dropping off like flies! I will have to look around for additional calculators.

The calculators start at 50…..I wish. MDJ is compulsive reading in order for me to be on target to retire at 65. My bad but thanks for the excellent information FT and all you commentators.

Hi Leo & Greg,

Your assumptions for rate of return of investments after you retire all make sense. The issue, though, is that a sustainable withdrawal rate needs to be lower in case things go wrong. Retirement can be 3 or 4 decades, so there is a lot of time for things to go wrong.

The “4% Rule” is generally sound. I worked through the actual 150-year history of stocks, bonds and inflation to see what rates have been sustainable. Withdrawals of 3-4% (depending on asset allocation) have been very sound.

I have found ways to get 5-6% by managing it carefully over the years. Most people should stick with withdrawals of 3-4%. That’s 3% for an income portfolio, 3.5% for a balanced portfolio (which most seniors do), and 4% for an equity portfolio.

I will be writing a detailed artilce on this shortly.

Ed

Hi Ed,

I’ll be interested in your planned article. Some things I’d be interested in seeing addressed in it: How did you go through the 150 year history stocks? And what income harvesting (eg. rebalancing) and withdrawal strategies (eg. fixed rate inflation-adjusted or fixed percentage) did you consider? It would be hard to beat the analysis Michael McClung does in http://livingoffyourmoney.com/. Are you familiar with this? I’d be interested to know what you think of it.

The book provides strong evidence that the highest safe withdrawal rates come from balanced portfolios, too much equity (more than 60%) and you run the risk of having to sell stocks when the are down which leads to a death spiral to running out of money.

The book also provides strong evidence that though you can usually afford to withdraw 5-6%, putting a 5% floor on your withdrawal rate is pretty risky.

good read. Will check them out. 4% average definitely seems low but guess depends how conservative one is. keep it up

I publish a spreadsheet retirement calculator on my blog at http://pabroon.blogspot.ca/2015/05/retirement-planning-and-forecasting-20.html that has all the features of your Perfect Calculator.

I just started using your spreadsheet Steve, it works really well! You’ve obviously put a lot of work into this, this is the best calculator I’ve found.

When I started blogging, I calculated my number to be around $2M. Once I reach that figure, I think I can make around 5% in income for that amount. So $100K pre-taxed a year is enough for me.

You should think about how much you withdraw after inflation if you plan to be retired for a long time (I hope you do :). 4% after inflation is a good rule of thumb, so you’d need $2.5M if you want to have $100,000/year pretax spending power for the long term with a low chance of running out of money. This book goes into a lot more detail of the factors and strategies to consider, it’s expensive but has a 100 page free preview http://livingoffyourmoney.com/.

Thanks for the advice Greg, I really appreciate it. When I retire, I think that I will still have some sort of income that’s not coming from my savings. Three sources that I have not accounted for yet are my pension from work, CPP and real estate income.

Hi Leo,

Is that $100K in today’s dollars or future dollars? In a couple decades, the cost of living will probably be about double today.

Ed

then there is the Liberal factor of over taxation that’s libel to change your plans