Canada Personal Pensions: Defined Benefit vs Defined Contribution Plans

Two of our most well-read articles here on MDJ cover the “government pension” that consists of CPP and OAS. In order to give the most accurate view of the pension landscape in Canada, I thought I’d take a look at defined benefit pensions plans and defined contribution plans as well.

Both defined benefit (DB) and defined contribution (DC) plans are generally referred to as “personal pensions.”

Now, to make matters a bit confusing, that broad “personal pension” category includes the pension you’d get if you work for the federal or provincial governments. Government employees often have a defined benefit pension, and because they’re working in the public sector it can get easy to get confused. Consequently, I’ll try to be as clears as possible when I reference them below.

Also, it’s important to keep in mind that not all defined benefit plans belong to government employees, and not all government employees have those plans. Some government employees fall under the same defined contribution plans that are more common in the private sector.

Are You Saving Enough for Retirement?

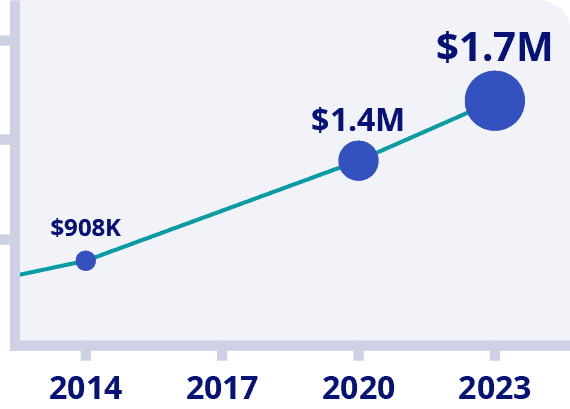

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

Before we get too far into the weeds in the defined benefit vs defined contribution plans discussion, and how to make the most out of each one, here’s a quick look at the Canadian retirement landscape.

- About 6.6 million Canadians are enrolled in a personal registered retirement plan of some kind. That’s roughly one third of working Canadians.

- Out of those 6.6 million Canadians with a pension, roughly two-thirds are defined benefit plans. Eighteen percent are defined contribution plans, with the remainder being a combination of hybrid plans and pooled RRSPs, etc.

- Canadian pension expert Malcolm Hamilton stated back in an interview in 2015 that the private sector had quickly been moving away from defined benefit plans and into defined contribution plans. In a recent conversation we had, he confirmed that this trend has continued and neither of us see any sign of it stopping.

As a teacher I know just how valuable a pension plan can be when it comes to retirement planning. In fact, for a lot of government employees, their defined benefit pension IS their retirement plan.

In this article we’re going to cover some of the differences between the two main types of pensions in Canada, how to estimate your pension, how to tell if your pension plan is safe, if you should take a lump sum pay out, and what certain pension vocabulary like “bridging benefit” and “cost of living adjustment (COLA)” means.

Use the Table of Contents below to jump to whatever part of the conversation makes the most sense to you.

- What is a Defined Benefit Pension Plan?

- What is a Defined Contribution Pension Plan?

- Defined Benefit Pension Plan Formulas

- What is the Cost of Living Allowance on a Pension?

- What is a Bridge Benefit on a Pension?

- What is the Commuted Value of my Pension?

- Deciding on a Survivor’s Benefit for your Pension

- Will My Pension be There for Me?

- FAQ About DB and DC Pensions in Canada

- Canadian Pensions in 2024 and 2025

What is a Defined Benefit Pension Plan?

A defined benefit pension plan is probably the type of setup that you think about when you consider a traditional pension.

The basic idea is that you pay into a plan while you’re working. The employer then takes your money, matches it with their own, and then invests it on your behalf. When you retire, you get a check every month until you pass away.

The key thing to understand about a defined benefit pension plan is that the legal responsibility for making sure those cheques keep coming is completely on the employer. It doesn’t matter how the investments did or if they screwed up and didn’t collect enough money from you up front while you were working – the responsibility is on them.

Obviously this is a big risk for companies to take on, and consequently, defined benefit plans are becoming quite scarce for any Canadians who don’t work for a government entity or one of the massive Canadian corporations (and even those are getting pretty rare).

Generally employees love defined benefit pension plans because you know exactly how much you’ll be getting in retirement and there is no investing knowledge required on their part. It is a pretty simple setup from the employee perspective. We’ll get into how pensions are often calculated in just a second.

Advantages and Disadvantages of a Defined Benefit Pension Plan

1) It is so simple. No worrying about picking your own investments or employer matching percentages.

2) Much easier to use for financial planning – especially if there is a cost of living adjustment built in.

3) There is no risk of your money running out (assuming your employer doesn’t go bankrupt).

4) The investment risk is spread out amongst generations (like in the CPP) – as opposed to managed by a single individual.

5) Defined benefit plans are often packaged with other benefits like extended health plans or life insurance offers upon retirement.

6) If you pass away relatively early after retirement, your spouse often gets a portion of your pension – BUT – the rest of your pension money will be left “in the retirement pot” for the rest of your colleagues to split up. There is no way to leave your pension payments to your loved ones in your will.

7) If you pass away before your spouse, they usually only get 50-75% (depending on the survivor’s benefit options selected at retirement) of your full payment.

8) They are very expensive and time consuming for private employers to provide. This likely results in less up front pay to employees.

9) If your employer (or the pension trust that they have created) goes bankrupt, you may not get your full pension. This is known as “counterparty risk”. We’ll get to this in just a second.

What is a Defined Contribution Pension Plan?

A defined contribution pension plan is a bit more complex from an employee perspective, but is quite simple from the employer standpoint. (Hence the move over to this type of pension setup over the last few decades.)

When it comes to defined contribution plans the employer basically says, “Look, we want to help you (our employee) save for retirement – but we don’t want to be on the hook for this long-term payout that could be 80 years into the future. Instead, what we’ll do is encourage you to save for your own retirement by making your contribution automatic, or by incentivizing you to save by matching whatever you put into your retirement investment plan.

We’ll leave the actual investing and planning up to you, but we’ll give you some money as part of your overall compensation package. When you retire there are no guarantees from our side, but hopefully you’ve made good use of all the money we kicked in along the way.”

Defined contribution plans can come in many shapes and sizes. Here are a few characteristics to look out for when checking out your plan:

- Is your plan automatic? In other words, is an amount automatically deducted from your paycheque depending on your directions to HR.

- What is your “pension match”? How much will your employer contribute to your plan relative to how much you choose to contribute?

- Who administrates your DC plan? Is it a mutual fund company, just a simple RRSP match – what investments do you get to choose from once you contribute?

Once you have the answers to these questions you can formulate your own plan. Here are the two most important things to take into consideration when optimizing your defined contribution plan.

1) ALWAYS make sure to get the free money from your employer’s match. This is one of the easiest wins in personal finance. It doesn’t matter if the match is 100% (“we’ll match it dollar for dollar”), 50% (“we’ll put in $0.50 for every dollar you put in), or even 25%. Always, always, always, if you can at all afford it, try to get that free money from your employer and get it working on your behalf.

Sometimes employers will structure defined contribution plans to say something like, “We’ll do a 100% match up to 3%, and then a 50% match from 4%-8%.” If that’s the case make sure and contribute 8%!

Tom Reid, senior VP of group retirement services at Sun Life Financial recently stated that when it comes to not maximizing the free money from employers, “between $3- and $4-billion across the country per year […] it’s a massive amount of employer match being left on the table.”

2) Always choose the lowest cost + most diverse investing option available. More and more employers are getting smart about using all-in-one ETFs or robo advisors to help administrate their defined contribution plans. Still others will simply contribute to your RRSP alongside you (my preferred option).

However, there are still many companies that force you to choose from a predetermined set of mutual funds if you want to get their automatic contribution math. In those cases, what you should do is:

- Respectfully ask your employer and HR teams to look into better investing options. Mutual funds are generally a terrible investment route in Canada.

- Suck it up, and pick the lowest cost fund (look for funds with a low MER), that still spreads your money out across several asset classes and regions of the world.

- Ask what the minimum amount of time that you have to have your money in the plans’ mutual funds is – then take out your funds + the employer match as soon as possible.

Advantages and Disadvantages of a Defined Contribution Pension Plan

1) The money is yours to do with as you please. Some see this as an advantage because they have some degree of control over the investments (depending on how the plan is administered), but some dislike the added responsibility of selecting investments.

2) By far the biggest advantage for most people when looking at DC vs DB plans is that the assets stay within your personal ownership. This means that if you were to pass away the day after you retire, your estate would maintain full control of the money you had put away. Of course, with a DB pension that money would stay in the pension pool and go to your former colleagues who had the good fortune to live longer.

3) Being able to plan when you take your retirement money can result in more efficient planning. You can plan things so that more of your income ends up in lower tax brackets, and/or make major purchases earlier in retirement if you’re so inclined to make those trade offs.

4) Employers love defined contribution plans because they are very simple from their perspective. They are simply responsible for making a one-time contribution instead of the lifetime obligation that exists under DB plans.

5) Disadvantages include having to know and understand investing, math, and probabilities to a much higher degree. Higher fees, bad advice, and many other potential issues can leave funding your retirement a bit of a minefield if you’re not the studious planning type.

6) You don’t get to take advantage of mortality credits in a DC plan. Mortality credits mean higher pension payments due to some folks within DB plans not living as long as others.

7) It’s all just more complicated in a DC plan. The raw simplicity of a DB plan is a big deal for a lot of people. This is why I’d recommend looking at transitioning at least part of your DC plan (if not the whole thing) into an annuity upon retirement. Check out our investing in Canadian annuities guide for more details.

Defined Benefit Pension Plan Formulas Decoded

So, you never thought you’d use that high school algebraic math stuff again, huh?

If you want to try to predict how much you’ll get from your defined benefit pension plan each month you have a few options:

1) Ask your HR person to sit down with you and explain it. This assumes that they actually know how it’s done – or can point you in the direction of someone who does. Oftentimes these well-meaning folks actually aren’t aware of how all the variables in these plans work.

2) Read on below and decode your own pension plan.

3) Kidnap your old math teacher and offer to release them only when they can tell you in plain language how much money you’ll be getting each month.

Each defined benefit plan is unique, but usually they operate on a specific formula. Each formula will use variables to determine a person’s unique monthly payout. The math folks usually solve problems by showing a variable as a letter or symbol such as “x”. I’ll try my best to use plain words instead of saying stuff like, “If we let X equal the square root of y, then add z, you’ll get your answer – easy.”

The most common variables that you’ll need to know in advance of tackling your defined benefit pension formula are:

- The number of years that you worked.

- How much you earned each year. (Your pension is often calculated as a percentage of your top wage. That top wage is sometimes your final three years, sometimes your best 5 out of the final 7 years, or sometimes it’s not a “top wage” but an average of your career wages.)

- Some pension plans will also use a “magic number” where you add together your age plus the number of years you worked at that job, and when you meet that minimum you can begin collecting your pension.

Usually your defined benefit plan payment formula will look something like this:

(Calculation of your average or top wage) x (2% x # of years worked) = annual pension (divide by 12 for monthly amount).

Of course there are many variables that can go into specific plans, but many look something like this. So a hypothetical pension calculation might be:

-John’s average wage over his top five years was $80,000

-He worked 30 years at this job

80,000 x 60% = $48,000 = A monthly pension of $4,000

If there is an age minimum or “magic number” (where age and years of service are added together) then usually there is a pension formula for a “full” or “unreduced pension” followed by a further calculation that has you subtract for the number of years away you are from hitting these milestones.

Here’s an example.

-Jane’s average wage over her top five years was $80,000

-She worked 30 years at her job, starting at age 25 and ending this year at age 55.

-Jane is eligible for her full pension at age 65 or the “magic number” of 85. There is a penalty of 2.5% per year if she retires before she meets either of those criteria.

It will be 10 years until Jane is 65 years old, but only 5 years until she hits her “magic number”.

Jane has the same years and service as John, and her unreduced pension would be the same $48,000 annual pension. However, she cannot begin collecting that amount if she chooses to immediately begin accepting her pension. Instead her new formula would be:

$80,000 x [60 – (2.5 x 5)] = $40,000. Monthly pension = $3,333.33

These are the main “building blocks” of most pension formulas, but each defined benefit plan in Canada has been negotiated separately and has unique quirks. Many teachers’ pension plans for example have changed at some point in the last 50 years, so some teachers will have one formula for the first part of their career, and a separate formula for the second part. Their final annual pension payment will be some sort of combination of these two agreements, usually proportionate to the number of years worked in each system.

In most cases the best course of action to take when trying to predict your defined benefit plan pension is to ask your HR for a pension estimate. If you are fortunate enough to have a union, they often put on pension seminars where you are free to go and learn. Take your estimate with you, see if you agree with the calculations, and then get your union representative to double check that the estimate makes sense, and that you understand your unique pension formula.

What is the Cost of Living Allowance on a Pension?

One of the most important aspects of a defined benefit pension is whether it includes a cost of living adjustment (COLA). A COLA is a yearly change in your pension payment that takes inflation into consideration.

Some pension plans will have a COLA that will increase your payment by the full percentage of inflation, while others will only increase it by a fraction. Inflation is usually calculated by looking at Canada’s Consumer Price Index (CPI) each year.

For example, if Mark retired last year and his initial pension was $40,000, then if the CPI increase was 6%, Mark’s new payment this year would be $42,400 – assuming he had a full CPI Cola.

If Mark’s COLA was only equal to 2/3rds the CPI, then his new payment would be $41,600.

Cost of living adjustments are all about protecting your purchasing power over the long term. If Mark didn’t have any COLA at all then he would keep getting the same $40,000 each year in retirement. Obviously, if Mark retired at 60, by the time he was 90 that same $40,000 wouldn’t be purchasing nearly as many products or services as it used to!

This reduction in purchasing power is due to inflation. If inflation averaged 2.5% during Mark’s retirement, then his $40,000 annual pension payments would only buy him about half the amount of stuff/services at 90 as when he first retired at 60.

The higher the percentage of the CPI your COLA tracks each year, the more valuable your pension is in the long-term.

What is a Bridge Benefit on a Pension?

Some of Canada’s defined benefit pension plans will include something called a bridge benefit. The bridge that is being referred to is meant to connect your early retirement to when you reach the “normal” retirement age of 65. For example, many teachers, nurses, military personnel, or police officers who choose to retire at 55 will receive a bridge benefit.

Once again, it’s key to understand that every pension plan calculates the bridge benefit slightly differently, so make sure to apply your unique plan’s formula.

That said, most bridge benefits usually operate in the following manner:

- The goal is to give the pensioner a relatively similar amount of income throughout their retirement.

- The pension plan administrators know that “full CPP” will kick in at 65. So rather than have your overall income shoot way up at that time, a bridge benefit takes some of the income you were going to get at age 65 and “front loads” it to the years before that.

- In addition to some of your own “future pension money” coming to you a few years early, pension plans can use some of the overall pension plan’s money to top up your pension during your pre-65 years.

So if you choose to begin receiving your defined benefit pension plan payments before the age of 65, usually what that means is that the amount of money that you have coming from your personal defined benefit pension plan will go down at 65. However, since you’re now getting your OAS and CPP, you’ll either be getting the same or (much more likely) more overall money sent to you each month because now you’re getting your personal pension + your CPP + your OAS.

Of course, this means that to some degree you’re trading getting money today for the ability to earn more in the future. If you live to be 90+ (exact age depending on your details and the details of your pension plan) then it’s probable that you would have been ahead of the game not to use a bridging benefit. On the other hand, getting money that you want early in retirement is a major advantage for a lot of people.

There are some really interesting solutions that pensioners can use to smooth out income where they choose to take the retirement bridge benefit, enjoy that money until age 65, then begin taking their OAS, while still deferring their CPP for a few years after age 65 in order to build up a higher guaranteed CPP benefit for life.

What is the Commuted Value of my Pension?

The commuted value of a pension is the amount of the lump sum the company or trust providing the pension would have to pay out today if an employee decided to take the lump sum in exchange for the income-for-life of a defined benefit pension plan.

Commuted values are usually calculated taking into consideration the present value of money versus long term interest rates and the life expectancy of the group of beneficiaries. Commuted value is only applicable to a defined benefit plan, as with a defined contribution plan the employer’s responsibility ends as soon as they make the contribution alongside the employee.

As with other parts of your pension plan, the commuted value formula that applies to you is likely somewhat unique to your specific plan. Consequently, asking your HR team to explain your commuted value today or for a point in the future shouldn’t be a big deal. It should be presented as, “If you were to retire on this day, you would get these options of a defined benefit plan vs this commuted value that would be paid as a lump sum”.

Pension Plan Lump Sum Rollover and Taxes

If you choose to take the commuted value of your defined benefit pension plan as a lump sum, then be prepared to pay some substantial taxes that year. These taxes are one of the two big reasons why I believe most Canadians are better served by leaving their retirement savings in a defined benefit plan.

The other main consideration is that most Canadians just aren’t very good at managing their own money. Generally we make poor investment decisions and we pay too much to do it! Even in a best case scenario, we’re all still subject to the whims of the market.

Now, the tax situation incurred if you decide to take the lump sum commuted value of your pension is a bit complicated as it depends on several variables. Usually what happens is that the lump sum is effectively split up into two parts. One part goes into a Locked-In Retirement Account (LIRA) while the second part comes to you as cash.

For that cash part, you’ll be taxed at your marginal tax rate. Considering most people worked at least part of the year that they retired, their marginal tax rate on this money will likely top 40%. Now, if you have contribution room in your RRSP, you can transfer this bulk payment to your RRSP to decrease the tax owing “up front”.

Then, as you withdraw the money from the LIRA and/or your RRSP you will pay your marginal rate at that time. Obviously, you can control the pace that you withdraw money at that point – and consequently how much taxable income you take out – until you get to 71 and have to convert your investment portfolio to a RRIF. Make sure to get a detailed estimate on what your tax bill would be if you choose to take the lump sum instead of the monthly DB cheque!

Deciding on a Survivor’s Benefit for your Pension

When you are enrolled in a defined benefit pension plan, you will be asked to make several decisions at the end of your career. The first is when you would like to take a lump sum commuted value as opposed to a lifetime of pension payments. The second is usually when you would like to begin receiving pension payments. The third factor that will likely impact the size of your eventual pension payments is deciding how you wish to handle the survivor’s benefit aspect of your DB plan.

The survivor’s benefit is setup to protect couples who may be dependent on each other’s pension income in retirement. The usual setup is that when one spouse passes away, the surviving partner will be allowed to collect a part of the original pensioner’s income.

Depending on the details of the specific pension plan, usually the survivor’s pension amount is somewhere between 50% and 75% of the original value. Most plans will allow the pensioner to choose the survivor benefit percentage upon retirement.

Now, obviously there is a higher likelihood that either you or your spouse could live to an advanced age vs solely your own chances of living to an advanced age. That means that the pension plan has to take into consideration that it is more likely that they will have to make payments for longer.

Consequently, the higher your survivor’s benefit percentage that you choose, the lower the monthly payments will be for the duration of the pension. Some pension plans will also give a “5- or 10-year guarantee” option where the surviving spouse would be entitled to 100% of the pension benefits for up to 10 years after the original pensioner began receiving payments. Again, this comes with the tradeoff of a slightly lower monthly pension payments.

For most folks it really comes down to how dependent the surviving spouse would be on that income in a worst case scenario. If the gap from 50% to 75% replacement would mean a substantial hardship, then it’s probably worth the relatively small monthly income hit. On the other hand, if the spouse of the pensioner is in very poor health at the time they retire, perhaps it makes sense to eliminate the survivor’s benefit altogether.

Will My Pension be There for Me?

YES!

Well… almost for sure – YES!

Your pension will be there for you.

If you’re talking about your pension cheque still being there when you retire, then you’re obviously referring to a defined benefit pension plan, because if you had a defined contribution plan, then the money would stay in your personal control the whole time.

Historically, DB pension plans have held up very well in Canada. Today, I would argue they are even more rock solid. This isn’t due to pension plans making smarter decisions, it’s simply because a much larger percentage of the plans are held by government employees and not private companies.

You see, for your defined benefit plan to not pay you, the entity that funds the retirement must declare bankruptcy and be wound up. BUT even when this happens, most pensioners will still get a large chunk of what they were entitled to. Even in a worst case scenario like the Nortel Networks fiasco back in 2009, the pensioners eventually ended up with 55%-70% of what they were supposed to get.

Now don’t me wrong – getting a little over half of what you were counting on getting still really sucks!

Here’s how you can try to decide if you can depend on your defined benefit pension in the future.

1) Do you have a government pension?

Because if your pension is covered by the government I’d be over 99.9% certain that you will get your full pension payments. There has never been a federal or provincial employee not get their retirement benefits as they have never had to declare bankruptcy. While I’d be slightly less certain about municipal government pensions, they are less common and even those smaller entities have been very stable since the 1930s.

2) If you don’t have a government pension, what is your pension’s transfer ratio?

The term “transfer ratio” is the one you’re going to want to ask your HR team about.

Now, I wouldn’t panic at all if you don’t have a government pension. Canada’s pension guru Malcolm Hamilton has been quoted several times over the past ten years saying that on the whole, Canada’s defined benefit pension plans are in a solid state.

In order for you to not get paid, your company would have to go bankrupt while having underfunded the pension plan. The transfer ratio is a measure of how much of the plan’s future obligations it could payout if it were terminated today.

If your company tells you that your transfer ratio is 85% or 90%, I still wouldn’t panic. Canada has many regulations to help govern these plans, and it could simply be that the plans have had a really bad couple of years when it comes to investments, and are likely to recover going forward.

The chances are still quite good that your defined benefit pension plan will make payments right on schedule for the rest of your life – although I’d be starting to get concerned the further the plan’s transfer ratio dipped below 90. As of 2021 (admittedly this hasn’t yet captured the recent market downturn) the average transfer rate for Canadian pensions was 103% – so we’re doing pretty well.

If you’re lucky enough to live and work in Ontario, it’s also worth considering that the Ontario Pension Benefits Guarantee Fund will insure the first $1,000 per month of your pension payments – but they are the only province to provide that coverage currently.

If my HR team got back to me and said that my pension plan had a transfer rate of below 85%, I would begin factoring that into my long-term retirement planning, and would probably start incorporating a possible hit to my payouts in the future – just to be on the safe side.

The smaller the transfer ratio, the more cautious I would be in my planning. Of course as more and more companies switch to defined contribution plans, this will probably become even more and more rare.

Are You Saving Enough for Retirement?

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

FAQ About DB and DC Pensions in Canada

Canadian Pensions in 2024 and 2025

As we close in on the end of 2024, there has been some good news on the pension front. There has been a renewed interest in defined benefit pension plans over the last couple years, with a slight uptick in DB numbers.

That trend doesn’t look like it’s going to slow down any time soon as workers in several industries grow more aware of their bargaining power. Of course, that small increase in DB plans has to be taken in as part of the broader overall picture that still sees most Canadians on the outside looking in.

I can say that on a personal level, the forced savings of a DB plan really helped me in my first years as a teacher. Anecdotally, I can say that the vast majority of teachers would be nowhere close to generating the same income in retirement if they were responsible for saving and investing their own money (even with the help of a company-matching DC plan).

All that said, it’s interesting to hear some of my former colleagues talk about how they wish they had the freedom of some of their DC-planned friends when it comes to retirement spending. They’re a bit envious of the fact that people who retire with a DC pension can opt to pull more of it out in their “go-go spending years” (say age 65-75) and then tail their spending off as they grow older.

It will be interesting to see if they still feel that way when roughly half of them live to turn 85 (and presumably the DB plan will look a lot more attractive – especially with a cost of living adjustment built in).

Perhaps the best news for defined benefit pension plans in Canada was that as of August 2024, the average solvency ratio of the plans was at about 124%! Only about 5% or so of DB plans had solvency ratios below 90%. Of course, one would expect healthy solvency ratios given the excellent run the stock markets have had over the last five years.