Edward Jones Review (Canada)

After we published our recent article on the best financial advisors in Canada, my inbox lit up with variations of the same question: Should I use Edward Jones financial planners?

What about the other big name advisory firms? It seems a lot of Canadians are wondering whether these well known brands actually deliver the value their marketing suggests. In fact, Kyle then went on to write about the Best Wealth Management Companies in Canada, because a lot of people were getting confused when trying to differentiate between terms such as “financial planner” “advisor” and “wealth management.”

Because several friends of mine have used Edward Jones over the years, and because their advisors regularly show up near the top of the Globe and Mail rankings, I thought it was worth putting together a detailed Edward Jones Review.

A quick note before we dive in. Everything here refers specifically to Edward Jones Canada. I have not dealt with their U.S. or international divisions, so the focus will stay on Canadian practices and Canadian investor experiences. And to be fair, many of the issues you will read about below are not unique to Edward Jones. They are simply one of the biggest and most visible examples of a financial management model that is still far too common in this country.

Edward Jones Fees and MER Explained

I’m not saying that Edward Jones doesn’t have good advisors working for them. Maybe some of them know their stuff. What I do know beyond a shadow of a doubt is that it is incredibly difficult to understand Edward Jones’ fees and costs.

You’re going to pay commissions to Edward Jones, further percentages to high-fee mutual fund providers, transaction fees, strategy fees, commissions for selling you insurance, commissions for selling you mortgages, etc. All of those fees and commissions stack on top of each other.

Here’s a look at the fees and costs involved versus Kyle’s pick for top financial advisory.

Edward Jones vs Advice-Only Financial Planner Fees Comparison

| Advice Only/Fee Only Financial Planners | Edward Jones | |

| Is there an upfront quote that is easy to understand? | Yes! | Definitely Not. Many percentages and fees to calculate. |

| Percentage the financial advisor and company will take from your portfolio | 0% | Somewhere in the 1-3% range – see below for details. |

| Are there several layers of additional fees such as markups when you buy securities, “strategy fees”, and account fees for every RRSP, TFSA, RESP, FHSA and investing account that you have? | No! | Yes! |

| Are advisors paid commissions to recommend investments? | No | Yes |

| Are advisors paid commissions to recommend insurance products? | No | Yes |

| Are advisors paid commissions to recommend mortgages? | No | Yes |

| Does the advisory company charge fees for services/products such as account transfers, margin accounts (loans), foreign exchange, trading fees, markups on investments you buy, etc? | No | Yes |

*The above information was interpreted from the Edward Jones “Understanding how we are compensated for financial services” document found here. Please consult this document to fully understand the complexity of compensation involved.

Edwards Jones Alternatives

My preferred alternative to Edward Jones (and other commission-based financial advisors in Canada) is Objective Financial Partners.

Objective is run by Jason Heath. If you Google Jason’s name, you’ll find out that he is trusted to write for the most trusted publications in Canadian personal finance. He has decades of experience in the industry, and has built a great team of specialists that can take care of any financial planning curveball you throw their way.

When you go to them with a question or asking for a financial plan, they’ll tell you exactly what is needed to get you on the right track – and give you a quote for their time. It’s very simple and doesn’t require digging through pages of jargon-filled compensation fineprint.

Jason and his team don’t make a nickel off of any products that they recommend to you. They also don’t get paid more if you invest more of your money through their private platform (they don’t have a private trading platform to funnel investors into like the big wealth management companies do). Consequently, they are completely objective (hence the name) about the investments they recommend, and the financial planning tools they advise to use.

Objective Financial Partners is an independent entity and doesn’t have a bunch of overhead costs from paying rent in strip malls or buying the naming rights to a big stadium. You can easily schedule an appointment with them every six months – or if you just need help one time to make sure you’re on the right track, they’ll do that for you as well. I have yet to stump them with a financial quandary – let me know if you manage to do so!

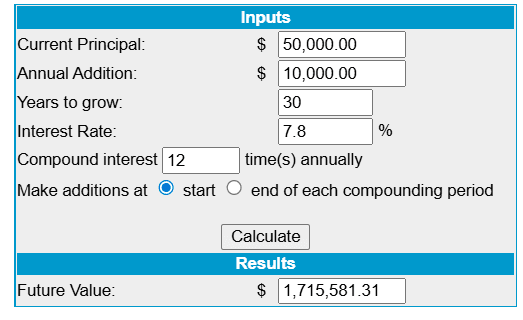

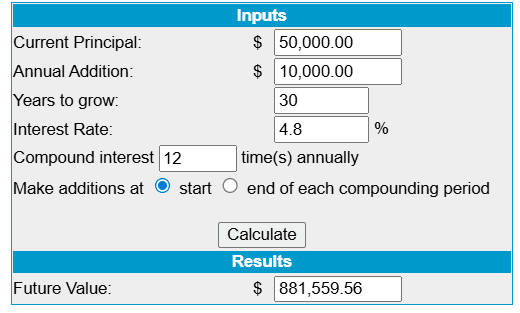

In case you’re wondering if all of these small fees make a difference, let’s take a look at a hypothetical situation. Say you are 35-years-old and have saved $50,000 in your investment accounts. You hope to add $10,000 per year. Here’s a hypothetical look at how I personally think (based on publicly-available data) your money would be likely to grow:

| Using a fee-only, advice-only financial planning company like Objective | Using Edward Jones Portfolios |

| Description of all fees paid: Upfront pre-quoted dollar amount for the initial financial plan. Anytime you want a follow up meeting, you’ll pay a predetermined fee – just as you would for the time of any other professional. Then you would pay the .20% MER (rough estimate for diversified index ETFs that anyone in Canada can access). | Approximation of fees paid: -Likely advisory fee of about *1.5%. -Likely mutual fund fees and other investment fees of about *1.5% -A wide variety of charges described above – averaging out to .2% of your portfolio. |

| Total % taken out of your investments EVERY YEAR: .20% | Total % taken out of your investments EVERY YEAR: 3.2% |

*Note: Edward Jones Canada lists their Guided Portfolio program fees as “starts at 1.5%” here on their website. We were not able to find any data on the exact mutual funds used in those Guided Portfolios, but this article from Rob Carrick at the Globe and Mail, as well as this recent article from Morningstar highlight the fact Canada has some of the highest mutual fund fees in the world.

The percentages associated with annual account fees obviously depend on the size of your portfolio. The schedule of fees can be found here. In our example, the fees on our 35-year-old with a $50k portfolio would be close to .50% originally, but would go down from there as a percentage of a growing (hopefully) portfolio

Your Portfolio With Fee-Only vs Edward Jones (assuming 8% return)

That’s almost a million dollars difference! By taking 3%+ out of your portfolio each year instead of the .20% in ETF fees that you would pay with a fee-only, advice-only adviser, you could be voluntarily paying what is basically a million dollar tax!

Edward Jones Investments

The above look at how Edward Jones’ fees can quickly eat up your portfolio assumes that you will earn the same overall market returns with Edward Jones’ investments as you would with basic low-cost index investing ETFs.

That assumption is almost assuredly incorrect, as it’s much more likely the investments chosen by your advisor will be worse than the market average due to active investing underperformance.

Here’s what Edward Jones Canada writes about their “strategy” for selecting investments on your behalf:

With our years of experience, we know what quality looks like. Our Research department recommends stocks, bonds and mutual funds that we believe will perform well over time – through good and bad markets.

The issue is that there is no evidence that active investment can in any way predict which stocks, bonds, and mutual funds will perform well over time. It is my opinion that the rare handful of geniuses out there who can actually tell “what quality looks like” ahead of time – are working for massive hedge funds – certainly not as small-scale advisors.

It’s impossible to know what specific investments that your Edward Jones advisor will recommend to you. All of the company’s literature says that your investments will be based on getting to know you and developing an overall plan. Yet we see substantial evidence that the company misled investors from 2013 to 2018, and urged them to “churn” portfolios so that they would generate higher fees.

Three things we know for sure when it comes to Edward Jones investments.

1) They will be expensive.

2) The total fees that you’re paying will be difficult to understand.

3) Given the long-term statistics around active management, the investments are almost guaranteed to be below average.

Comparison of Financial Advice

Aside from investments, comparing a fee-only, advice-only financial planning company like Objective Financial to Edward Jones can be difficult on the surface. Much depends on the specific advisor that you choose. I thought Kyle’s take on how to choose the right person for you in his best financial advisors in Canada article was a great starting point.

That said, some broad generalizations can be made:

- Edward Jones’ advisors get paid more to recommend certain insurance products over others.

- Edward Jones’ advisors get paid to recommend products such as mortgages and lines of credit.

- Edward Jones’ advisors receive more bonuses and prizes the more they sell products and services to you. These even include programs like the Edward Jones Travel Awards Program.

- Fee-Only, Advice-Only financial planners such as Objective Financial or fellow Canadian writer Robb Engen DO NOT receive bonuses or any other type of payment for selling products to you.

So, in saying all that, which advisor will give you better advice?

The one who gets a bonus plus a free trip to Hawaii if they recommend a specific insurance plan or investment fund?

OR

The one who gets paid to simply provide you with advice – and gets paid exactly the same no matter which products they recommend.

Obviously it’s impossible to say with 100% certainty which advisor is going to give the better advice, but I think it’s pretty clear why Kyle (and myself) are so partial to fee-only, advice-only financial planners.

Edward Jones Review: FAQ

Edward Jones Review – Final Verdict

Is it possible to get good advice from an Edward Jones advisor: Yes… it’s possible.

Personally, I can’t recommend any financial planning company that charges an impossible-to-define percentage of your overall portfolio every single year. You can see from my calculations above that making the wrong decision about your financial advisor could cost you hundreds of thousands of dollars by the time you reach retirement.

There’s a reason why nearly all of Canada’s financial columnists (who do not get paid for recommending any type of investment advice model or specific investments) all recommend fee-only, advice-only financial advisors. These include Rob Carrick, Andrew Hallam, and even Canada’s own Wealthy Barber – David Chilton (in a recent podcast episode). Indeed, a recent article in the Globe and Mail revealed that there is a booming market for fee-only advisors. It appears the message is finally being widely accepted.

At this point, after decades of conclusive research, there really is no case left to argue on behalf of paying financial advisors by taking a percentage of your entire investment portfolio. That fee structure creates the wrong incentives.

No one is going to tell you to pay down debt if they get paid less for doing so!

The only reason the %-of-a-portfolio system has survived this long, is because most Canadians were never shown a better way. Once people understand how financial advice should be paid for, the old model starts to look pretty ridiculous.

Easy rule of thumb: When every independent expert with nothing to sell recommends one approach – and the only people defending the old model are the ones earning money from it – the conclusion is pretty obvious.

There are certainly advisory firms out there with worse track records than Edward Jones, but I have not seen anything that convinces me they deserve a place on your shortlist. Their fees are extremely high, their compensation structure encourages product sales, and the disclosures can make it hard for the average investor to understand what they are paying for, and how much the final bill actually is!

Don’t just take my word for it! Do your own research, talk to some fee-only planners, compare alternatives, and see what you find. And if you have personal experience with Edward Jones, feel free to share it in the comments below.

Some Final Notes on Canadian Mutual Funds

Upon further reflection, when I updated this article, I felt that I needed to provide some more info on just why Canadian mutual funds are a horrible deal for Canadians. Edward Jones is definitely NOT the only company that takes a commission in order to recommend mutual funds – but there is so much misinformation out there on this topic, that I thought I would take a second to list some indisputable facts about why Canadian mutual funds are bad investments.

1) Over 98% of Canadian mutual funds failed to match the return you would have gotten if you would have invested in a basic Canadian equities ETF ten years ago.

2) The worst mutual funds aren’t even included in most statistics due to something called Survivorship Bias. The basic idea is that every year the worst mutual funds get eliminated, so they don’t even have 10-year records to measure against. This means that substantially more than 98% of mutual funds wouldn’t have matched the average – but they just aren’t around to be included in the statistic!

3) Active investing will encourage you to move in and out of mutual funds – usually at the worst times. The vast majority of mutual fund investors actually end up getting less than the average returns of the funds they are invested in! For more information on this phenomenon, Google “mutual fund fees mind the gap”.

4) Mutual funds in every country are a pretty bad deal, but Canada has some of the highest mutual fund fees in the world.

5) Many mutual funds incur a ton of taxation due to buying and selling investments – passive investment in ETFs do not incur those costs. Look up the work done by Stanford economists Joel Dickson and John Shoven for more information.

6) Just look at all the commercials you see for the big names in the investment industry. Look at who pays millions of dollars for the naming rights on Canadian rinks and stadiums. Where do you think all that money comes from?

7) Don’t take my word for it. Here’s recent Nobel Prize-winning economist Daniel Kahneman in an interview with Der Spiegel: “In the stock market… the predictions of experts are practically worthless. Anyone who wants to invest is better off choosing index funds.” There are many Nobel Prize-winners that agree with Mr. Kahneman! Even former Wall Streeter and best-selling author Michael Lewis invests in index funds – and he has spent the last three decades interviewing the sharpest financial minds in the world!

8) Jack Meyer, the head of Harvard University’s endowment fund stated, “The investment business is a giant scam. It deletes billions of dollars every year in transaction costs and fees.”

9) Andrew Hallam quoted CFP Olivia Summerhill in this most recent book, and she stated, “During the Certified Financial Planning extensive training, the focus is not on investment vehicles. A CFP candidate does not get training in their program if actively or passively managed funds are better for clients.” He goes on to list similar sentiments from several other CFPs. Combine that with the massive financial incentives that advisors have to recommend mutual funds… and you can see why it’s a longstanding problem.

I could actually keep going and make this list 20+ points long – but I think you get the picture!

What a Disaster

My advisor retired and i was transfered to ************* on The Queensway, in Toronto

All I can say is she was in it for her own personnal gain and commissions,

Her lack of knowledge, abiltiy to listen and disregard for her customers best interest promted me to FIRE her.

Once I decided to move my account, I sent her a note to halt all trascations on my account, only to find out she made trades that triggered $10,000 in commissions. It took weeks to resolve with no correspondance from the branch, or even an explanation

I WOULD NOT TRUST THIS ADVISOR TO MANAGE MY KIDS PIGGY BANK

[Editor’s Note – names redacted for legal liability reasons]

This isn’t an apples to apples comparison.

The Edward Jones Model the initial $50k and annual $10k contributions include the cost to hire a financial planner.

For the Fee only model. There’s an additional cost to hire the financial planner. Those need to come out of the initial $50k and annual $10k contribution.

To make it more apples to apples we need to know the Cost of the Fee only planners initial visit and remove that from the $50k. Say it’s $1500 right off the bat, that leaves our 35 year old with $48500 to invest initially. Then each year there’s a visit to review and tweak, say that costs $500. The annual contribution then becomes $9500 instead of $10,000.

If we run the compound interest calculator with the same interest and time horizon with $48,500 initial and $9500 annual. We come out with $1.59 Million after 30 years. That’s $200k less than the example above. But still well over $700k ahead of the Edward Jones scenario.

I just made up the Fee only planner costs. I have no idea how much they actually are. So maybe you can help fill in this gap a bit more accurately.

Thanks for sharing your wealth of knowledge and writing such a detailed view of what terrible value these commission based advisors are.

There is another problem with the example in this article. The author subtracts the MER from the rate of return for the mutual fund. Mutual Fund returns are stated as *net of fees.* So – the “interest rate” for the Edward Jones example should actually be 8%. Gross return of the underlying fund would have been 11.3% less MER of 3.3%. Most articles that talk about the evils of mutual fund fees get this wrong.

When I show a client a Fund Facts document, and it says 13.34% over the last 10 years, it *means* exactly that. Your money grew by 13.34%. Does it matter that there was a 2.4% MER taken *before* that? Just like everything else – you get what you pay for.

No, you’re misleading people here Christopher. There is no way that if the market averages 8%, the Edward Jones reocmmended fund is going to get 11.3%. In fact, it’s much more likely to trail the market average given what we know about how bad mutual fund managers are.

Mutual funds are 100% a case of you get what you DON’T pay for. If you were right, then higher fee funds would of course give better returns (you’re paying more, so clearly the person behind the mutual fund must be picking better investments for you). Of course you are dead wrong: https://sg.morningstar.com/sg/news/154499/how-fund-fees-are-the-best-predictor-of-returns.aspx Please take your propaganda somewhere else.

No. I’m really not. MER is deducted before a return is calculated. When they say a fund returned 8% it *really* paid the end user 8%.

Want proof?

https://www.fondsftq.com/en/personal/positively-invested/management-fees-mer-impact#:~:text=The%20higher%20the%20management%20expense,deducted%20to%20cover%20the%20fee.

https://www.td.com/ca/en/asset-management/documents/investor/pdf/news-insight/Management_Expense_Ratio_En.pdf

https://www.sunlifeglobalinvestments.com/content/dam/sunlife/regional/canada/documents/slgi/810-4169-slgi-insidemers-en.pdf

https://www.rbcgam.com/en/ca/learn-plan/types-of-investments/what-is-a-management-expense-ratio-mer/detail

https://www.investopedia.com/articles/investing/062113/mutual-funds-management-fees-vs-mer.asp

All of the above note that the fund return is *net of fees.*

Also, from the Ontario Securities Commission:

“What is a management expense ratio?A management expense ratio, or MER, is a combination of a mutual fund’s management fee and its operating expenses. They are paid by the fund and are expressed as an annual percentage of the total value of the fund. This means the effect of the MER is already factored into the market value reported in your account statements.

The management fee paid to the fund management company includes the cost to oversee the fund, hire a portfolio manager and other companies to assist in the fund’s administration. Operating expenses can include bookkeeping and administrative fees, marketing costs, filing and legal expenses, as well as taxes.

MERs can range from less than 1 per cent to more than 3 per cent. While investors don’t pay these expenses directly, they are affected by MERs because these expenses reduce the fund’s returns.”

So yes. When a mutual fund such as the AGF American Growth Fund reports a rate of return such as this years YTD return of 12.23% that is *after* the 2.65% MER.

https://www.morningstar.ca/ca/report/fund/performance.aspx?t=0P000070DS

And as for misleading… the morningstar article you referred to exposes exactly zero actual data. What are the ranges of fees they’re talking about? What do they consider a “low” fee vs “High?” What funds, what categories? All that article really says is “I made some pretty charts.”

Christopher,

I really hope you aren’t using your real name to make these comments, because at best you’re revealing your severe lack of knowledge to your clients and colleagues, and at worst you may be opening yourself up to legal liability.

You just spent all that time writing a response when you clearly failed to read what I replied. Let me break this down for you.

1) Yes, mutual fund fees are reported net of MER – that much we agree on.

2) Mutual funds are NOT on average beating their comparable index baseline by as much as their MER charges. It’s ridiculous to suggest this, and possibly criminal.

3) So when I write as an assumption that a market returned 8%, I’m actually giving a hypothetical mutual fund the benefit of the doubt in saying that it would get the average returns of the market minus their MER. This is in fact not really fair because the vast majority of actively-managed mutual funds DO NOT actually achieve market-average results over the long term.

4) You may respond (like most folks who recommend high MER funds) that you “only choose the good funds”. The only problem with that is that there is no academic evidence that supports the idea that an advisor can select the right mutual funds ahead of time. (i.e. “Past performance is not indicative of future results”).

5) Morningstar is pretty much the gold standard when it comes to mutual fund research in several countries… but sure you need more info. Ok, here’s a few more for you.

-Here’s one from NYT: https://www.nytimes.com/2022/12/02/business/stock-market-index-funds.html

-Ben Felix quotes several academic papers from Nobel Laureates and investing heavyweights like Vanguard and proves you’re wrong here: https://www.pwlcapital.com/do-active-managers-really-protect-your-downside/

-Here’s conclusive data from around the world (updated annually) by S&P global: https://www.spglobal.com/spdji/en/documents/education/education-spiva-scorecards-an-overview.pdf

-And to top it all off, here’s where Warren Buffett proved you wrong: https://www.cnbc.com/2022/10/03/billionaire-warren-buffett-swears-by-this-inexpensive-investing-strategy-that-anyone-can-try.html

If you want more, I’d recommend you start by reading John Bogle, Andrew Hallam, and John Robertson.

So, I’m going to past your reply so that I can address it in sections…

“You just spent all that time writing a response when you clearly failed to read what I replied. Let me break this down for you.”

Pot? Kettle. :-)

“1) Yes, mutual fund fees are reported net of MER – that much we agree on.”

Yes. That is exactly what I posted in both my first and second replies. You know… when you said I was misleading people.

“2) Mutual funds are NOT on average beating their comparable index baseline by as much as their MER charges. It’s ridiculous to suggest this, and possibly criminal.”

Please highlight where I suggested that? Or… did you not read my posts? Now.. you say “on average” and I just have to ask – what about the ones that are? And do, every year? Sure, they’re not “average” but they *are* out there. That’s why you need a good advisor.

“3) So when I write as an assumption that a market returned 8%, I’m actually giving a hypothetical mutual fund the benefit of the doubt in saying that it would get the average returns of the market minus their MER. This is in fact not really fair because the vast majority of actively-managed mutual funds DO not actually achieve market-average results over the long term.”

Are you talking about markets, or funds? Because your calculation examples are based on a portfolio that is reporting a return of 8%. Not a market, and perhaps not even an individual fund. But – as in your point 1 – the MER are taken before the reporting of net returns of 8%. So, as I said in my first reply, you are incorrect to reduce the 8% by the amount of the MER. If the statement says you earned 8% then you *really* did.

“4) You may respond (like most folks who recommend high MER funds) that you “only choose the good funds”. The only problem with that is that there is no academic evidence that supports the idea that an advisor can select the right mutual funds ahead of time. (i.e. “Past performance is not indicative of future results”).”

Correct. We can only select funds that have a proven track record. How do you go about selecting individual stocks, or ETFs? Which of those are the “good” ones. How much academic evidence is there that an advisor, (or an individual investor such as yourself) can select the right etf ahead of time? How many of your investments took a beating over the last 12 months?

“5) Morningstar is pretty much the gold standard when it comes to mutual fund research in several countries… but sure you need more info.”

It is. I use it all the time. We have access to their portfolio and analytics for our business. In fact, they have even built recommended portfolios for us, for multiple purposes. But the article you replied with, to disprove something I *never* said… had no real data.

You have confirmed my point from both of my replies – MER comes out before the rate of return is published. So, you agree that your calculations are misleading. Thanks for clearing that up. I haven’t bothered with the rest of your post, because it’s all tangental to what I have actually said, and really nothing more than a smokescreen.

You just keep digging your hole deeper when it comes to revealing your ignorance here Christopher.

1) You still haven’t read my first reply. You are still misleading people. It has nothing to do with if funds report net of MER, it has everything to do with the idea of assuming that mutual funds can beat a market average.

2) You still are not reading the sources of education I provided for you. I pointed out several sources of data and some of Canada’s most acclaimed financial authors that all agree that financial managers cannot pick the very very few mutual funds that outperform ahead of time. In other words, the little mutual fund outperformance (where it exists) is almost assuredly due to luck, and consequently cannot be picked ahead of time. Please, before composing a response, actually do some research… or just keep responding without educating yourself and continue to reveal to potential clients why the traditional model of financial advice compensation is broken in Canada.

“It is difficult to get a man to understand something, when his salary depends on his not understanding it.” – Upton Sinclair.

I’d add that it’s even harder to get a man to understand something when his commission depends on it.

3) Just read the post, you will get your answer. You don’t seem to understand that a fund will underperform the market average over time – so I’m actually putting the passive strategy at a disadvantage here. You’re trying your best to muddy the waters in order to sell products, but it’s really quite simple: your commission-based mutual funds are a terrible deal for investors.

4) In admitting that you can’t pick the better mutual fund ahead of time, you contradict the very notion that someone should pay you high fees to beat the market! It’s incredible that you confidently state things, and then refute your own points in the exact same post!

Obviously you continue to ignore all of the data I presented you with, because if you’d read any of it you’d know I’m a fan of passive index investing – which is based on the premise you shouldn’t be trying to select “the right ETF ahead of time”. There is no “right ETF” when you’re referring to index ETFs. Or did they forget to assign that chapter on passive investing in mutual fund sales school? I personally have done exactly the market average (minus .10 or so) becauase that’s what passive indexing is!

5) So the source that you use for analytics comes out with a study (btw, they do this study year after year to confirm the findings) and you say that the specific article has no real data. Great argument there. Trust Morningstar sometimes… but not when it refutes the idea that your entire compensation structure is ridiculous.

You failed to address the rest of what I’ve written because you’re too lazy to actually read new information and you don’t want to admit that the way you’re charging people for financial advice is unethical. Frankly, it’s a perfect representation of what is being described above by FT when it comes to commission-based salespeople calling themselves “financial advisors” and throwing a bunch of sand in the air instead of actually reading evidence-based sources of information.

I’m sad that you’ll go to work tomorrow and mislead a bunch more people all day Christopher. Hopefully we educate or regulate high-fee mutual funds out of existence sooner rather than later.

Why would you need to pay the fee-only advisor each year Billy? You presumably have the plan in place, only need to chat when there is a major update needed I would think? When I update this article, I’ll indeed show it with the cost of an initial plan.