CPP Ultimate Guide – Eligibility, Payment Dates, Withdrawals & More

Most Canadians know the Canada Pension Plan as a government account they pay money into every month when they are working, and then when they retire, CPP means a cheque or automated deposit that arrives every month.

Sounds simple enough right?

Well…

There are many layers to CPP!

It’s one of those topics in Canadian personal finance where you might be just fine with the broad outline for now, and then come back to you when you need specific details. When I first set out to write about the best age to begin withdrawing CPP Payments I thought there would be some handy rules of thumb. It turns out that there were so many variables that I decided to turn this article into a deep dive of all things CPP.

Please use the Table of Contents below to quickly find the CPP information you’re looking for:

- CPP Withdrawals

- CPP Eligibility Rules

- Applying For CPP

- Deferring Your CPP

- CPP and Early Retirement

- What is The Enhanced CPP?

- CPP Payment Dates 2024

- CPP FAQ

Are You Saving Enough for Retirement?

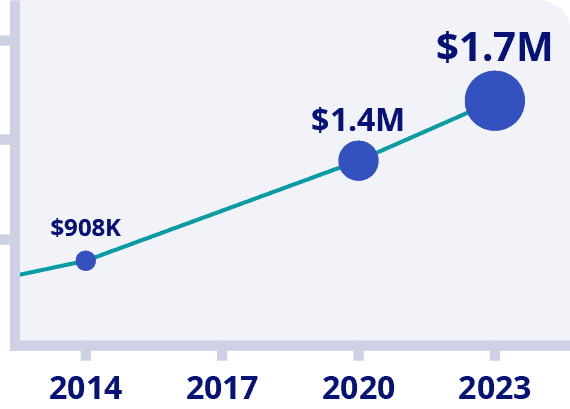

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Get $50 Discount With Promo Code MDJ50

*100% Money Back Guarantee

*Data Source: BMO Retirement Survey

What Is CPP

The Canada Pension Plan – or CPP – was created in 1965 in order to help Canadians efficiently save and invest for their future retirement needs.

The idea is that both employees and employers set aside a percentage (5.95% each in 2024 up to a maximum of $68,500 of income, plus the addition of the new Additional Maximum Pensionable Earnings – which we’ll discuss later) of the employee’s salary, and that amount will then go to the Canada Pension Plan Investment Board – where it is managed by professionals.

These investment professionals can select from a wider range of assets than the average Canadian (such as big infrastructure projects like airports), and they can spread their collective risk out over many decades.

Over the ten years ending March 30, 2022, the CPP Investment Fund achieved an annualized return of 10.8%. Generally speaking, while I think some things could be improved about the CPP – namely how much we pay the people in charge – overall, it is a very good plan compared to what’s offered by most other countries.

Unlike Old Age Security (read our full OAS guide) each Canadian’s CPP payout will be very unique and will chiefly depend upon how much they contributed to the plan over their years in the workforce.

This is your money coming back to you (after investment gains), and it never enters the general government spending pool. CPP is not a tax like the GST or income tax!

At age 60, every Canadian can decide to begin collecting CPP. The cheque or automated deposit will arrive every month until you pass away. The CPP is an extremely well-funded pension program and its risk level is roughly equivalent to that of the entire country/government of Canada collapsing.

When to collect CPP is a personal decision that depends on a lot of variables. Although you can begin CPP at 60, the standard age is 65, and you can defer the start of your CPP to age 70. The later you start your pension, the higher your payments.

How to Estimate My CPP Withdrawals at Age 65

One of the first questions for folks planning their retirement should be: How much will I get for my CPP payment when I retire?

That simple question is actually more complicated than you might expect. Most Canadians choose to take their CPP beginning at age 65. We’ll go over some other scenarios in the next lesson, but for now, here’s how to estimate your CPP payment if you were to begin receiving payments at age 65.

The best rule of thumb I’ve found is from CPP expert Doug Runchey:

Each year of work when you made the full CPP contribution is worth about $30 per month on your CPP cheque. Consequently, if you made 50% of the full contribution, then that’s worth about $15 per month.

Now there are a ton of variables and caveats that go with this rule of thumb. If you want a more precise answer, I suggest grabbing your CPP Statement of Contributions and heading over to Doug’s CPP Calculator here.

In order to understand how much CPP you’re entitled to, you first have to wrap your head around the fact that it all depends on how much you paid into it.

Each year that you work in Canada the government basically says, “OK, we want you and your employer to save for your retirement. In order to ensure that you don’t have to eat dog food after your working years are behind you, we’re going to force your employer to hold back 5.95% of your gross income and make those same employers also pay the equivalent of 5.95% of your salary.

BUT, we’re only going to take that money up to a certain point. That point is called the Year’s Maximum Pensionable Earnings (YMPE). In 2023 the YMPE is $66,600 and the basic exemption is $3,500. That means that if you earn $66,600 or more, both you and your employer kick in $3,754.45.”

($66,600-$3,500) x 5.95% = $3,754.45

If you are a self-employed sole proprietor, you pay the employee and employer contributions as part of your annual tax return filing.

You’ll find that past CPP contributions and future CPP payments are all based off of that YMPE figure that the government sets each year.

So, if a year in which you made equal to or more than the YMPE is worth roughly $30 per month on your future CPP cheque, then obviously if you only earned 80% of the YMPE in a given year – you’ll get about 80% of that full $30 a maximum YMPE-year would have generated. So roughly $24 per month.

It takes 39 years of full YMPE contributions to garner the full or “maximum CPP.”

2024 Update: 2024 is the first year that the government will begin collecting what they’re calling Yearly Additional Maximum Pensionable Earnings (YAMPE). For folks who retire over the next few years, this YAMPE won’t make much of a difference.

It does mean that a little more will come off of your paycheque each year. So, for 2024, the YMPE is $68,500 (due to inflation) and then the YAMPE means that you’ll have to contribute 4% of your income from $68,500 to $73,200.

If you didn’t quite make it to 39 years of full-YMPE contributions between the ages of 18 and 65, don’t worry too much, as most Canadians don’t collect anywhere near the maximum CPP.

The maximum CPP for someone starting to collect at 65 is currently $1,364.60. But, the actual average CPP payment sent out to a new Canadian 65-year-old pensioner is $811.21.

This shows that relatively few Canadians are able to consistently earn the full YMPE for the best 39 years of their working life. Keep this in mind before you pencil in the maximum amount for CPP in your situation.

Now, the government is willing to cut you some slack in your quest to get your CPP up as high as possible…

How to Get the Maximum CPP: Dropout Years

- The CPP is calculated using the amount of contributions that you made during the 47-year stretch between turning 18, and turning 65. (If you take CPP at 65, you can also extend your contributory period to 70.)

- The CPP administrators are going to let you have a “dropout period” where you can erase the 8 years of your lowest contributions to CPP. For some people this will be the first 8 years of their career, for others it will be early retirement years or career sabbaticals.

- Keep in mind that the YMPE changes every year. For example, back in 2009, it was $46,300. The government is going to track your progress on meeting the YMPE each year, and it will show on your CPP Statement of Contributions.

Under these rules, if you can get to 39 years of YMPE, you will be entitled to the maximum CPP payment each month. For each of those 39 years that you were below the full YMPE, your payment will be proportionately reduced.

Using the CPP Child Rearing Dropout to Boost Your Payment

The Child Rearing Dropout (CRDO) is the CPP’s attempt to take parental responsibilities into account when creating a fair pension system. The idea is that a person shouldn’t be penalized due to taking time away from a CPP-producing job to raise a child.

Here’s the gist of the program:

- If a couple has a child under the age of 7, then ONE parent will be allowed to claim the label of “primary caregiver”. They will be eligible to apply for the CRDO.

- For a couple with multiple children, as long as you have one child under the age of 7, then the primary caregiver will be eligible.

- The CRDO is not automatic. One must complete the ISP-1640 in order to apply.

- If the primary caregiver earned less than the Basic Exemption ($3,500 at the moment) then they can use that year as an extra “dropout year” when it comes to calculating their CPP. Obviously eliminating such a low earnings year will help boost your average CPP contribution and allow you to collect a larger pension.

- If the primary caregiver earned more than the Basic Exemption, but less than their average lifetime earnings, then they can also use the CRDO to drop those years – thus increasing their average.

- The CRDO can also be used to help someone qualify for CPP disability and survivor benefits, described in more detail below.

- Prior to 1993, normally the female spouse was primarily eligible to collect the Family Allowances benefit, and consequently are the ones eligible for CRDO during those years. (Unless the couple was split and the child was living primarily with the male parent or the female parent waived her rights.) Since 1993, CRDO eligibility has been granted to the parent who was eligible to receive the Child Tax Benefit.

The bottom line concerning the CPP Child Rearing Dropout is that if you took time off, or decided to scale back to part-time work while you had a child under the age of 7, then you can decide “not to count” those years when it comes to calculating your average lifetime earnings.

CPP Eligibility Rules

The two key criteria to qualify for CPP payments are:

- You need to have contributed at least once to the CPP during the ages of 18-65.

- You must be at least 60-years-old

There is no eligibility rule in regards to the number of years you resided Canada, nor do you have to be currently residing in Canada to get your CPP payments.

If you worked in Quebec you would fall under the Quebec Pension Plan (QPP) and not the CPP. If you contributed to both plans, your benefit will depend on where you’re living when you apply.

If you are working in Canada and earn more than $3,500 per year, you are required to contribute to CPP.

What is My CPP Statement of Contributions?

If you’re trying to determine how much your CPP is going to be, you need to start by grabbing your CPP Statement of Contributions.

*It’s important to understand right off the bat that the CPP payment number that you “could” receive – as stated on the CPP Statement of Contribution – is almost useless. There are so many assumptions that go into that number that it’s not a reliable predictor. (You’d be better off using the rules of thumb mentioned above.)

The information that you need from the CPP Statement of Contributions is how much your pensionable earnings were each year that you paid into CPP. You might notice a little “M” next to some years. The more M’s the better, as they signify a year that you paid the full YMPE. Once you have those numbers, it’s possible to calculate your average lifetime earnings and then see how various retirement scenarios would alter things going forward.

Applying for Your CPP

Once you decide when you want to begin receiving your CPP payments (see below for more details), you need to apply to start receiving your pension.

You’ll be given three options:

1) Start receiving your CPP payments as soon as you can (60 years old – or one month past your 60th birthday).

2) Start receiving your CPP payments at age 65.

3) Choose a specific date to begin receiving your CPP payments.

You can apply for your CPP using either a paper application, or apply online using the My Service Canada Account (MSCA). You’ll also want to be able to access the MSCA so that you can quickly snag your statement of contributions.

Applying by paper means that you have to download the ISP1000 application, complete it, and mail it in, or drop it off at a Service Canada office. Be prepared for your CPP application to take 120 days if you go this route.

CPP Withdrawal Age 60 vs 65 vs 70 – Deferring Your CPP

The vast majority of financial experts agree that the average Canadian should defer taking their CPP as long as they can afford to in – in most cases. (“It depends” is a popular saying amongst planners.)

Yet in his book, “Retirement Income for Life” Canadian pension guru Fred Vettese states that, “Only 1 percent or so of all CPP recipients postpone the start of their CPP payments until age 70.”

Here’s the raw math behind the CPP withdrawal at 60 vs 65 vs 70:

- 65-years-old is considered the “normal” or baseline age for CPP. You can take CPP starting any month between ages 60 and 65 – which would usually be referred to as “taking early CPP”. You can also take CPP starting any month between ages 65 and 70 – which would usually be referred to as deferring or delaying CPP.

- For every year that you take CPP “early” the amount that you get each month will be reduced 7.2%.

- For every year that you defer your CPP, you get an automatic 8.4% + inflation increase to your eventual payment (but of course you miss out on the amount of money you would have gotten that year). If you continue to work after 65, it alters the math a bit, and we’ll discuss more below.

That automatic 8.4% + inflation figure is a pretty amazing financial planning tool to use for retirement. It might not be for everyone, but deferring your CPP is an option that many more Canadians should choose. Like most other personal finance decisions, it’s all about trade-offs.

What deferring your CPP comes down to for most people is:

1) If you really need the income, then there isn’t much more consideration needed. Deferring your CPP will require you to either cut your budget, withdraw more of your own private investments/savings, or to find enough work to offset the loss of CPP income. For many people none of those three solutions are doable.

In other words, if you don’t have a minimum of $200,000 or so savings/investments when you turn 65 – and you’re done with the working world for one reason or another – then you’re probably best off ignoring the rest of this and just taking your CPP at 65. If you qualify for GIS, you’re likely further ahead to not worry about deferring your CPP.

2) If you have significant reasons to believe that you will pass away before 77-80, then you’re better off taking CPP at 65. There are a wide variety of life expectancy calculators out there, but remember that you’re not looking at “birth life expectancy”, but instead the life expectancy for someone who has already made it to 65.

After reading numerous studies, I’d put the average life expectancy for today’s 65-year-old Canadian male at about 85, and the average 65-year-old Canadian female at about age 88. Another way of looking at this, is that there is a 1-in-10 chance that you’ll live to be 99!

The main risk factors for falling on the wrong side of that life expectancy average include smoking, obesity, alcohol consumption, driving habits, and blood pressure. After these behavioural factors, family history would come into play. The more of those boxes that you check off, the greater the occurrence of a debilitating condition before the age of 77-80, and the more attractive taking CPP at 65 becomes.

For what it’s worth, Vettese recently wrote in the Globe and Mail, “The probability of premature death is small. Between ages 65 and 80, there is only a 13 per cent chance of dying if you are female and 20 per cent if you are male.”

3) How do you personally value the trade-off between life-long guaranteed government income (the ultimate hedge against living to extreme old age) vs leaving behind more of an inheritance if you were to pass away before the age of 77.

There is no right or wrong answer to this tradeoff. Personally, I told my parents, I’d like them to spend their money on themselves, and enjoy the reduced stress of having a significant amount of guaranteed income no matter how long they live – but it’s their money!

By far the most common fear that financial planners hear from Canadians when they ask them to consider delaying CPP goes something along the lines of:

“Well what if I use up all (or a lot of) my savings between the ages of 65 and 70 – all so that I get this increased CPP payment – and then I pass away at 73! Now the government gets to keep all my money and I leave nothing for an inheritance.”

While there is no denying the unpleasant reality that the above scenario could occur – it’s important to realize that it’s fairly unlikely (as our average life expectancy shows). The more relevant risk factor is actually having your savings run out in extreme old age, and then needing to drastically reduce lifestyle considerations, and/or depending on family for financial help. The increased CPP payment is an absolute safeguard against that eventuality.

Withdrawing a substantial amount of your investments before 70 can also mean that you get to keep more of your money due to being in a lower tax bracket when you withdraw RRSP income – and can even help avoid the OAS clawback by spreading your withdrawals over more years.

Finally, when it comes to inheritance, remember that if you were to pass with assets in an RRSP, that money is likely to get taxed at the highest tax rate, as it will all be deemed income for the year you pass away. Non-registered accounts would also trigger capital gains in a similar manner.

If you have other assets (such as a house) that you could bequeath to your loved ones, then perhaps this tilts the tradeoff in the direction of deferring CPP at least part of the way to 70.

Oh – and the delayed CPP plan actually gets even stronger when we factor in the recent enhanced CPP boost that was recently announced, as the 8.4% increase will now be applied to a larger principal.

Deferring CPP Withdrawals Break Even Point

Many people are still skeptical about the math behind deferring their CPP and want to know what their “break even point” is if they decide to pass up the guaranteed “bird in the hand” at age 65.

The first thing to understand about calculating the break even point is that it depends on how long you defer. You’ll have to live longer if you defer to age 69 than if you defer to age 67 right?

The second thing to understand is that a break even point will change depending on what you would hypothetically do with the cash the government would send you at 65.

Whether you decide to spend your own savings while you delay taking CPP, take CPP and leave your own savings to keep earning investment returns, or take CPP + invest that CPP money (while you spend your own savings in order to fund day-to-day expenses) it all equals out to the same thing: There is a time value of money element to bring into the equation.

Depending on what investment returns you would receive in the future, the present value of your personal savings will be different. The problem is that there is no real way to know what the future returns of assets like stocks and bonds will be.

The most convincing argument that I read (while reading way too much about CPP break even points) was this one by PWL Capital. The idea is that to compare apples-to-apples, you should use the risk-free rate of return (so that it is essentially guaranteed) because the 8.4% + inflation return that you get by delaying your CPP is basically guaranteed.

If you were to use a bond- or GIC-ladder to keep your money growing (instead of using it to replace the CPP income you could have gotten), then your break even age for taking your CPP at age 66 vs 65 would be age 80.

The longer you delay, the longer you’d have to live to “break even”. Of course this assumes that you would ideally structure your personal investments using a bond ladder (not paying any fees to someone to help you), and doesn’t take into account the relative simplicity of just delaying CPP vs having to manage your own investments until at least 80 years of age.

What Happens to my CPP Withdrawals if I Retire Early?

Nothing special.

In other words, your CPP payments don’t really care if you retire early or not. The same CPP factors apply to you no matter when you retire. Namely:

- What your average lifetime earnings are.

- What age you decide to start taking your CPP payments.

Now, obviously if you decide not to work at any point between ages 18 and 65 that could have some effect on your average lifetime earnings. As we discussed above, you can only “dropout” 8 years of earnings when it comes to calculating your CPP average lifetime earnings.

So, if you had managed to earn a healthy amount of money as an 18-year-old, and managed to make full YMPE contributions all the way from 18 to 57, then you could retire at 57, take eight years of “zeroes” on your CPP contributions – and still get the full CPP pension at 65. Of course, in that scenario you’d have to get by on your own savings from 57 to 65, but given that you’d have been earning a solid paycheque at a young age, that could be possible.

Alternatively, the more relevant example for most people would be that they probably had some years where they did not contribute the full YMPE amount. What that would mean to an early retiree is that you’d “use up” some of your dropout years on those “zero contribution years” of early retirement, and then be forced to include some possible low salary/low contribution years at the beginning of your career, or perhaps some part-time years when you had to switch employers, etc.

Now, if you choose to take your CPP at age 60 to help out with an early retirement, remember that you don’t get the full “eight dropout years”. Instead you’d get to drop out 86 months (a little over seven years) because the dropout consideration is proportional to your years in the workforce.

The important thing to consider is that no matter what your average lifetime earnings are, you will never get less money (even if you’re an early retiree) by deferring your CPP. The reason is that your CPP defer increase of 8.4% + inflation will always be worth more than incorporating one more “zero contribution” year into your personal CPP calculation.

Can I Get CPP While I’m Still Working? Do I Still Have to Make CPP Contributions?

Yes, you can choose to begin getting your CPP payments while you are still working.

Personally, I’m not a big fan of this strategy, as it’s likely going to lead to you paying more taxes than you need to. Plus, you limit the risk-free return you can get by delaying your CPP.

That said, it’s certainly an option.

How this will affect your potential CPP gets fairly complicated. It really depends on what your average lifetime earnings have been up until the point when you choose to take your CPP, and how much you will earn after that time. CPP expert Doug Runchey explains it in detail here.

Here are a few takeaways:

- It used to be that once you decided to begin receiving CPP payments, then you no longer had to contribute to CPP. This changed in 2012. (Yes, it is a bit weird to be both paying into the CPP, but also collecting money from the CPP – no way around it.)

- If you choose to begin collecting CPP before age 65 and are still working, you have no choice, you must contribute until you reach at least age 65.

- If you work after the age of 65 and are collecting CPP you can choose not to contribute any more.

- If you work after the age of 65 and choose not to collect CPP – you are actually still forced to contribute to the CPP even if it won’t actually help you (you’ve already got 39 years of maxed out YMPE contributions).

- If you choose to begin collecting CPP payments, and are also contributing to the CPP during that time (or are 60-65 and are forced to contribute while collecting), you become eligible for an additional CPP benefit called the post-retirement benefit (PRB).

- The PRB is an additional amount of money on top of the CPP payment you were already getting.

- The PRB will automatically begin the year after you start working-while-receiving-CPP-payments and will continue the rest of your life.

- The amount of your PRB will depend on what your earnings were in the years after you began collecting CPP, as well as the age when you earned the income.

What is The Difference Between The OAS and CPP Pensions?

As I explained in my OAS Clawback article, the OAS and CPP pensions are quite different. The CPP is essentially your own money coming back to you (after it was invested by the CPP investment team), while the OAS is more of a flat payment that the government makes out of general tax revenue each year.

Both pensions look very very safe and very very likely to be around when you are ready to collect them.

OAS basically depends on your age and how long you have lived in Canada between the ages of 18 and 65. It can also be “clawed back” if you earn more than the OAS threshold. You can defer collecting OAS, but if you can afford to defer only one benefit it should be the CPP due to the higher increase in benefits and the survivorship rules discussed below. How much you earned while working (or if you worked at all) while you were a Canadian resident will not change your OAS.

CPP depends on how much you have contributed during your working years (as we discussed above) and what age you are when you choose to begin receiving it. There is no CPP clawback to consider.

CPP Pension Splitting With a Spouse

CPP payments are counted as taxable income. Because of that, it makes sense to understand how to structure CPP payments so you pay the least amount of taxes.

The basic idea is that the government wants to give retired married couples a break. So what they do is allow the spouse who has less taxable income (whether from work, RRSP withdrawals, private pensions, or OAS/CPP benefits) to count some of the higher-earning spouse’s CPP pension as their own. The end result is that more of the couple’s taxable income is placed in lower tax brackets.

Splitting eligible pension income is not just for CPP payments (sometimes called CPP sharing), but can also be applied to company/government pension plans, RRSP-based annuity payments, and RRIF payments. Unlike these individual-based pensions, the CPP has its own set of rules that must be followed for spouses to pension split their CPP income:

1) Both spouses must be over 60 years of age.

2) You must be living with your spouse.

3) You must have lived with your spouse during your “joint contributory period” when one or both of you could have been contributing to CPP.

4) Both of you must have applied to begin receiving your CPP withdrawals in order to take advantage of CPP sharing. (The exception being if one of you never contributed to the CPP at all.)

5) Your CPP split will most likely not be a 50/50 measure. The maximum amount of income that a higher-earning spouse will be able to “share/split with” the lower-earning spouse depends on the “joint contributory period”. The joint contributory period is the amount of time that you and your spouse spent together AND while one of you was making CPP contributions.

6) In order to take advantage of CPP pension splitting, you need to complete the Application for Canada Pension Plan Pension Sharing of Retirement Pension(s) – ISP 1002. Both pensioners must sign the form, and usually your accountant will simply include it in the package you sign come tax time.

Note: CPP pension splitting is not the same as CPP credit splitting. CPP credit splitting refers to the division of assets (of which your CPP contributions are considered) in a separation settlement.

How does CPP Survivor’s Pension Work?

One of the major questions that a lot of couples have in regards to CPP withdrawals is: What happens when one of us passes away – do we lose all of that spouse’s CPP?

What you should first understand is that the CPP isn’t a private investment bank account. It’s more like a pooled insurance program. Because some folks pass before others, that’s what allows the payouts to be as high as they are. That’s what shared risk is all about.

Once you’ve internalized that your CPP “account” isn’t a private asset, the way CPP Survivor Pensions work makes a bit more sense.

Here’s how CPP survivor withdrawals work:

- The maximum CPP amount that you’re allowed to collect depends on when you choose to retire. Many Canadians choose the default option of 65 years old. The current maximum CPP Payment for 65-year-olds is $1,364.60 each month.

- If you are fortunate enough to collect the maximum CPP payment each month, then you will not get paid any more money if your spouse were to pass away.

- If you do not collect the maximum CPP payment, and you have a spouse that also receives CPP income, then you will receive some sort of a “CPP top up”, and your “combined benefit” would be higher than your previous personal CPP payment if they were to pass.

- Calculating what your combined benefit would be is not as simple as saying, “Hey, if we add our two CPP pensions up each month, we’re still below the maximum – I guess we’ll get that total amount.” Instead, the CPP administrators look at how old the surviving pensioner is, and how much money their spouse was earning before they passed.

- If a surviving pensioner is below the age of 65, the calculation is: (37.5% x the deceased pensioner’s former payment) + (a flat rate benefit that increases each year – in 2024 it’s $204.69).

- If a surviving pensioner is older than 65, then the calculation is simply: 60% x the deceased pensioner’s former payment. That amount would then be combined with the surviving pensioner’s CPP payment in a fashion that involved further tricky math.

- The maximum amount that the surviving pensioner is able to receive is subject to their personal “maximum” CPP benefit. For example if you chose to begin taking CPP withdrawals before age 65, then your maximum will be lower than someone who waited until 70.

- Most Canadians will need a minimum of 10 years where they contributed to CPP in order to qualify for a survivor’s pension or death benefit.

- There are a few more variations and special adjustments that can be applied, but at this point you likely get the basic idea. See Runchey’s post for more info.

What is The Enhanced CPP?

Many people Googling CPP-related inquiries likely came across the term Enhanced CPP.

The first thing to understand is that if you’re age 55+ and are going to retire in the next 10 years, this whole Enhanced CPP thing is going to have a minimal effect on you. Of course, the more years that you pay into this Enhanced CPP the more important it’s going to be – and the more you’ll notice the increasing about taken off of your cheque if you’re a earning more than $68,500.

Here’s a short summary of what the Enhanced CPP is, and why you might start paying higher mandatory contributions to the CPP program in 2024.

- In 2016, the government announced CPP changes that began to take place in 2019. The main idea was that Canadians needed to start saving more for their future retirements.

- Then in 2019, the government phased in an increase in the employer-employee CPP contributions. From 2019 to 2023, the shared CPP contribution rate went from 9.9% to 11.9% (up to that year’s YMPE).

- Starting in 2024, the government has raised the amount of income considered for a “full YMPE year”. Over two years, a 14% increase will be phased in. Basically this will force “upper middle income earners” to save more money via the CPP – but also receive a larger CPP payment upon retirement. This new amount that will apply over and above the old YMPE will be called the Yearly Additional Maximum Pensionable Earnings (YAMPE). It will also result in calling the old maximum CPP payments the maximum “base” CPP payment – before the YAMPE would be factored in.

- CPP payments began to increase in 2019 (over and above the normal inflation-related increase) as a result of Enhanced CPP, but the full effects of the Enhanced CPP won’t take place until 2065.

- When the full CPP enhancements have kicked in, the CPP will replace 33% of your average lifetime earnings (up to the YMPE), as opposed to pre-2019’s 25%. When you consider the increased contribution room provided by the YAMPE, that could mean as much as a 50% higher pension payment – but again, for most people reading this, the effects will be substantial less than that!

- As a rough rule of thumb, someone retiring in 2024 with full YAMPE earnings will receive about $26 per month more on their CPP payment than what their maximum would have been back in 2019. In 2029, the “extra” amount will be about $100. Again, it’s important to remember that you’ll only get that amount if you added 10 years of full YAMPE earnings during that time.

2024 CPP Payment Dates

Here are the 2024 published CPP payment dates and QPP pension payment dates (effective Jan. 3, 2024):

- January 29, 2024

- February 27, 2024

- March 26, 2024

- April 26, 2024

- May 29, 2024

- June 26, 2024

- July 29, 2024

- August 28, 2024

- September 25, 2024

- October 29, 2024

- November 27, 2024

- December 20, 2024

Are You Saving Enough for Retirement?

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Get $50 Discount With Promo Code MDJ50

*100% Money Back Guarantee

*Data Source: BMO Retirement Survey

Canada Pension Plan – FAQ

Will the CPP Be There for Me or Will It Run Out of Money?

One of the more bizarre conspiracy theories that common Canadians appear willing to believe is that their Canadian Pension Plan payments will not be there for them when they retire. This fear encourages all kinds of bad decision making.

Look, they might slightly change the CPP rules here and there, but this payment isn’t going anywhere, and it should be worked into your retirement plan.

A common statement I hear is: “Well… all I know is I don’t want to have to depend on that. If I get it, great. That will be gravy.”

That’s a very sad statement for me to hear because it will lead to a retirement paycheque puzzle that will always be missing several pieces. You’ll never have an accurate idea of what your options are.

You can depend on CPP – it will be there!

Not sure? Let me try to convince you with a few facts:

1) The one time in the last several decades that a politician tried to change Canadian retirement plans, he got his wrists slapped – hard. It was Stephen Harper, and he tried to very gradually change the OAS payment (not the CPP!), and his changes were immediately used against him. It was then reversed by the Trudeau government.

2) The government just changed the CPP to make it more important going forward. Why would they do that if the CPP wasn’t in good shape?

3) The CPP currently has around $570 billion in it and is the 7th biggest pension fund in the world. The piggy bank is pretty full.

4) Every three years the CPP brings in someone called the Chief Actuary of Canada. They take a look at everything, get together with some of the smartest math people in the country, and then say, “Everything’s good here” or “Uh… folks, we gotta make a few changes so that in 40 years we’re still ticking along.” At the end of 2021 the Chief Actuary did not see his shadow, and so CPP is safe for at least the next 75 years.

5) Remember, the CPP is not the OAS. We’ll talk about OAS payments another day, but the CPP is a separate pool of money. The government can’t just reach into the CPP pool and pull your money out to pay for stuff – it’s completely illegal for them to do that!

Great article, Kyle.

Wow, this may be one of the most comprehensive articles I have read on CPP. Thank you for the obviously extensive reading to pool these points together in one place (and easy to digest). Great read ?