How Much Do You Need to Retire in Canada? Not as Much as You Think!

For the traditional “retire at age 60 or 65” situation, the popular advice pushed by the financial industry is to save enough to replace 70% or even 80% of your gross income during working years. Another popular notion is that you’ll need at least $1M to retire comfortably.

The truth of the matter is that providing that you go into retirement with no debt (mortgage, consumer etc), and continue to live a modest lifestyle, you will likely need way less than that.

Expenses during Retirement

While every situation is different, there are a few significant expenses that should be reduced or eliminated during retirement.

These expenses include:

- Mortgage payments;

- Reduced income taxes;

- Saving for retirement;

- Childcare expenses (hopefully);

- Work clothes, lunches, commuting costs; and,

- CPP, EI contributions.

Rather than use a “rule of thumb”, I like using actual budget data to calculate anticipated expenses. I did this exercise in a popular article on early retirement, and I worked out that our family would need about 55% of our family income to retire comfortably.

While family incomes may vary, many financial types agree that the average family will require between 50-60% of their pre-retirement gross income to live comfortably during their golden years.

The Income

While 55% of gross family income sounds great compared to the industry standard 80%, it gets better! A couple who has lived and worked in Canada for most of their adult life will be entitled to government income benefits during retirement.

The main income benefits include Canada Pension Plan (CPP) and Old Age Security (OAS). Longevity of these income sources aside, according to Stats Canada, the average amount paid out by CPP is $7,600/retiree/year or $15,200/couple/year (assuming age 65 when commencing payments).

OAS, which is paid out the government tax base and calculated based on how long the retiree has lived in Canada, maxes out at $550/retiree/month or $13,200/couple/year. Combining the two brings a couple over $28,000 a year (rounded down to be on the conservative side).

With many middle class couples with no debt able to retire on approximately $50k/yr in todays dollars, that only leaves a gap of $22k/yr to be funded by company pensions and/or savings (RRSP, TFSAs etc). If there are no other company pensions, the question now is how much savings are required to generate the remainder, or in this example, $22k per year?

Using the 4% rule, which is assumed to be a “safe” portfolio withdrawal rate for a portfolio to last 30 years, simply divide the $22k (or whatever your number is) by 4% or simply multiply your number by 25. In this example, $550,000 in savings should do the trick. Even without a company pension, this is much less than the millions that we are made to believe to need.

Bottom Line

Figuring out how much you need to retire is not as complicated as some make it out to be. It’s pretty much a four step process:

- Work out a budget of expected expenses during retirement.

- Calculate how much the Government will provide you during your retirement years. You can use the Canadian government calculator here.

- The difference between 1 and 2 is how much income from savings (and/or company pension) that you will need.

- Take the number calculated in step 3, and multiply by 25. That is the amount you will need to have saved (in todays dollars). If you have other sources of income, like from company pensions or rental properties, then reduce step 3 by the other income amounts, then multiply by 25.

Note that this is an extremely simplified version of approximately how much you will need to retire. To get an accurate picture, you will need to account for taxation (which depends on how you structure your investment accounts).

In addition, there is uncertainty in the availability of government programs when looking at drawing from them decades away. In my opinion, it’s best to be as conservative as possible when estimating your “number”. In a future article, I will review how much you need to save today to hit your future “number”.

In any case, when you are ready to invest your savings, here is a comparison of the top discount brokers in Canada.

Are You Saving Enough for Retirement?

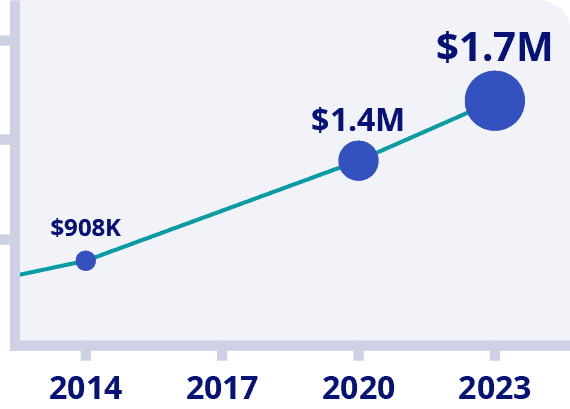

Canadians Believe They Need a $1.7 Million Nest Egg to Retire

Is Your Retirement On Track?

Become your own financial planner with the first ever online retirement course created exclusively for Canadians.

Try Now With 100% Money Back Guarantee*Data Source: BMO Retirement Survey

for the title of this thread, I say, ‘different strokes for different folks’, based on age, lifestyle & their individual needs & wants – there isn’t a one-fit formula

being old, tired & retired …. age post 65 ++, mortgage free, with our total all-in combined ‘expenses to income’ of less than 30%, which hasn’t changed much since retiring early.

a huge factor for us is that we are fortunate that we are no longer saving for or to get to retirement

with the above, we are cash flowing each month even though our month/month expenses average across 2018 are less than $2000/mth

cash assets are not invested in any ‘risky investments’ whether they’re indexed funds, mutual funds, dividend stocks.

we have zero of – precious metals, diamonds, a boat, a second home/income properties, cottage or toys.

OK, so even if all of our cash was in an HISA, we’d likely end up paying tax as well as not keep up with inflation

given that we cash flow, that cash flow no longer needs to be re-invested

bottom line:

life is good for us living in Canada despite the winters.

our goal as it has always been is to live a healthy stress free life till we simply don’t wake from our sleep … target age 99 & that we both die within 30 seconds of each other

for us & our lifestyle, time of life – liquid cash is key

we are not planning on leaving a legacy/inheritance

for now, we live a comfortable life here in the GTA metropolis on what the Government hand-out’s give us, even though our high cost of ‘property tax & utilities’ amount to approx 40% of our expenses or the equivalent of 12% of our income

The assumption on a percentage required of your working life income is flawed. The difference on earning $200 K / year vs someone earning $100 K / year significantly impacts the equation. The only rational way to calculate is by having the accurate assumptions of what you need as “essential” and what you want as “discretionary”. Without this relatively accurate information you are fooling yourself. The other critical factor that few speak of is your withdraw strategy of registered and non registered savings. This is key to minimizing your tax impact. Do not rely on investment professionals to lead you down the garden path, put pencil to paper, it is much easier than you think. Nobody can manage your portfolio and retirement planning as well as you can do on your own. Its your money, get and stay involved.

I think I am a little late to this interesting discussion, but what the heck. I’ll give it a shot. First of all, most people have the perception that if you retire (you don’t work on your primary job anymore), you don’t have another source of income. Instead of using the word retire, let’s change it to financial independence/freedom. When you achieve this status, I think you’ll probably be able do what you want. Hence, if you need supplementary income, it’ll shouldn’t be that hard to find some side hustle nowadays. In addition, most people who achieved FI has more than one sources of passive income.

Now to the amount of money that you need when you are financially freed. This is really a personal preference. When I calculate this number, I don’t factor in old age security or any types of pensions at all as I don’t like to be at the mercy of other parties that provide me an income. Instead, I think that I can generate a modest return from my net worth of about 4%-5% on annually basis. I want $80,000 to $100,000 of annual income per year (all other incomes are icing on the cake), which works out to about $2M = (80,000/0.04) or (100,000/0.05). I am at $1.1M now and about 10 years from my FI goal. I’ll achieve financial freedom @ 48.

Hi Leo,

Good post.

One question: Did you account for inflation? Do you want $80-100,000/year of income in today’s dollars or in future dollars?

In other words, when you are financially independent (at age 48), do you want the future amount that buys what $80-100,000/year buys today?

FT’s article is about retiring today, not in the future.

With most of the retirement plans I have seen, people are saving for a retirement 20-25 years in the future. By then, inflation should roughly double all the figures.

It sounds like your financial independence (like FT) is much closer than 20-25 years.

Ed

Hi Ed,

Thanks for bringing up the inflation beast. When I retire, I think that my biggest expense is going to be my grocery bills. One way to lower that is to grow my own food in my backyard. I have been blessed to have bought a good size home with lots of yard space and had been saving quite a few dollars with my home grown fruits and vegetables. The other sources to counter inflation are my CPP and pension from my employer, I have not included that in my income sources when I retire.

As for retirement date, I am 10 years away and a lot of things can change in 10 years. Hopefully I can continue to learn during this 10 years and find a war to make my retirement income worth in today’s dollar rather than the future.

I learnt one more thing to consider in my retirement already. Thanks for making me think.

-Leo

Three things for a happy retirement .#1 Good health (no smokin’ok?) #2 No matter how humble ,But own the roof over your head…Renting in retirement can be a deal breaker..#3 Own your auto ..No finance on anything..In Canada have your Old Age/CPP/GIS and a bit of savings…With those three going for you Don’t worry be happy ..Live a little frugal ..Enjoy the freedom of no more kissing up to anyone..But those #1 #2 #3 are a must have

Michael, Thanks. I second your motion.

There is a wealth of information in the topics and conversation on this website, but if I were moderating the comments I would consider blocking posts by SST unless they are constructive. It would be good for the website, and it would be good feedback for SST.

re: “None of your posts have been relevant to the topic”

Really, Ed? REALLY?

ALL of my posts have been relevant to the topic:

“How Much Do You Need to Retire in Canada?”

It’s just that ALL of my posts have been in complete opposition to your OPINION on the topic.

“How Much Do You Need to Retire in Canada?” (based on theory)

Ed’s Opinion: $1 million is needed to retire in Canada.

“How Much Do You Need to Retire in Canada?” (based on reality)

SST’s Opinion: $1 million is not needed to retire in Canada.

As for “intelligent conversation”…doesn’t take much intelligence to see that since <1% of the population has $1,000,000 in investable assets, there's a whole lotta people retiring on less than a million dollars and living to tell about it. That trend won't drastically change over the next century, let alone 25 years.

As for my "hijacking all threads to your same old topics and away from the topic in the thread," I provide opposing factual content to your "same old topic" theories of people needing $1,000,000 and how easy it is to attain said million. You keep posting that and I'll keep responding in kind.

Perhaps you should change the wording of your comments to something such as, "To possibly generate an income of $70-120,000 (before tax in today’s dollars; or $140-240,000 per year in future dollars) to continually support an accustomed comfortable lifestyle with quite a bit of entertainment and travel, at least one million future dollars in investable assets will be required."

And perhaps I should change the wording of my comments to something such as, "Anyone can, and will, retire on any amount of money."

I understand, Ed, that you are a paid advertiser on this website and you have a vested interest in the content supporting your business, I, however, have no interest in the same. My biases are toward fact. Until such time that the owner of this website sees fit that my content is unfit for his private property, I will continue to provide fact-based content. The owner of said website can always i) moderate my submitted posts and/or ii) ban me from his personal property if he so chooses.

What is to be respected are Canada's Fundamental Freedoms, expression being one of those.

Beyond that, exciting times lay ahead, Ed. As of 2015 (or sooner) we'll both have companies competing for the pre and post-retirement investment dollars of Canadians.

Fun times, indeed.

It appears to me that the point SST makes is sound. Many people do not get to the million dollar mark and still do retire. The bigger issue here is the fear mongering among investment industry so called experts. Make no mistake, they want your investment dollars.

re: “Saving enough to become a millionaire is not complicated, even for those with median incomes; just save a high percentage of your income for 40+ years and invest it well…”

No, it’s definitely not complicated, but it is intensely difficult (for many reasons).

Like saying anyone can run 100 meters, but how many people can run 100 meters in ten seconds?

re: “Perhaps we need to stop asking how much money we need to retire. After all, all it takes to retire is to stop working. The real question we need to ask is how much money it takes to maintain a given spending level…”

An excellently concise statement.

99% of people live and die — and retire — on less than a million dollars.

Just means they (perhaps) have less disposable income than during employment, doesn’t mean they can’t or don’t retire.

It’s true that it takes a lot of money to fund even a modest income such as $50,000 (in 2014 dollars) per year for 30+ years of retirement. It’s also true that most people will not succeed at saving the money needed for this income. That just means that most people will have lower incomes than this in retirement.

Saving enough to become a millionaire is not complicated, even for those with median incomes; just save a high percentage of your income for 40+ years and invest it well (and with low costs). Losing weight isn’t complicated either, but maintaining the discipline to lose weight or become a millionaire can be hard.

Perhaps we need to stop asking how much money we need to retire. After all, all it takes to retire is to stop working. The real question we need to ask is how much money it takes to maintain a given spending level (which is what FT has done in this article). And if the answer you get seems unreachable, you may need to set your sights lower on your retirement spending.

SST,

Can I ask you again – why are you here blocking intelligent conversation? The topic of this thread is “How much do you need to retire in Canada?” None of your posts have been relevant to the topic.

Have you noticed that once you start posting on a thread, nearly everyone else abandons it? MDJ is full of abandoned threads where interesting articles are followed by some interest exchange of ideas, and then discussion abruptly ends with SST posts to stop the conversation.

I guess I made the mistake of responding to your previous post, but I would like to express my frustration over your way of hijacking all threads to your same old topics and away from the topic in the thread.

I would respectfully request that you stop posting here and allow open conversation.

Ed