Financial Freedom Update (Q4) – December 2017 (+9.82%) – Year End Update

Welcome to the Million Dollar Journey December 2017 Financial Freedom Update – the final update of the year. For those of you new here, since achieving $1M in net worth in June 2014 (age 35), I have shifted my focus to achieving financial independence. How? I plan on building my passive income sources to the point where they are enough to cover our family expenses. All within the next 5 3 years.

If you would like to follow my latest financial journey, you can get my updates sent directly to your email, via Twitter (where I have been more active lately) and/or you can sign up for the monthly Million Dollar Journey Newsletter.

In my first few Financial Freedom updates, I talked about what life has been like since becoming a millionaire, why I like passive income, and our family financial goals going forward.

Here is a summary:

Financial Goals

Our current annual recurring expenses are in the $50-$52k range, but that’s without vacation costs. However, while travel is important to us, it is something that we consider discretionary (and frankly, a luxury). If money became tight, we could cut vacation for the year. In light of this, our ultimate goal for passive income to be have enough to cover recurring expenses, and for business (or other active) income to cover luxuries such as travel, savings for a new/used car, and simply extra cash flow.

Major Financial Goal: To generate $60,000/year in passive income by end of year 2020 (age 41).

Reaching this goal would mean that my family (2 adults and 2 children) could live comfortably without relying on full time salaries. I would have the choice to leave full time work and allow me to focus my efforts on other interests, hobbies, and entrepeneurial pursuits.

Previous Update

To give you context for this update, here are the numbers in my previous financial freedom update.

September 2017 Dividend Income Update

Account Dividends/year Yield on Cost SM Portfolio $6,400 4.35% TFSA 1 $2,400 4.90% TFSA 2 $2,750 4.87% Non-Registered $210 1.37% Corporate Portfolio $11,700 3.62% RRSP 1 $5,850 3.72% RRSP 2 $1,100 2.36%

- Total Invested: $795,071

- Total Yield on Cost: 3.82%

- Total Dividends: $30,410/year (+5.74%)

Current Update

In September, I wrote about being laid off for about 30 seconds from my government job after which I was given a temporary position for a few months. The quarter has passed and I was given an extension for another quarter.

Since that time, I’ve been in talks with a number of potential employers, mostly from my professional network which has resulted in a number of leads. Looking back through my career since graduating with my Engineering degree, my experience has shown that building a network is extremely important in career development. In fact, I’ve had 3 careers since that time, and all three have been a result of utilizing my network. Now I’m on my way to my fourth (maybe final?) chapter in my career – perhaps I’ll have some news on this in the next quarterly update.

Now, let’s talk a bit about my passive income strategy – generating dividend income. As dividends are the main focus of my passive income pursuit, there is a large dependence on the market. While there are merits to this investment strategy, there are also substantial risks – particularly dividend cuts. For example, look at what happened to Home Capital Group (HCG) earlier this year.

HCG is a secondary lender who had a very strong track record of dividend increases (18 years in a row). HCG funded their mortgages through client deposits into GICs and high-interest savings accounts. With the company under investigation, client essentially made a run at the bank and essentially wiped out HCG’s high-interest savings balance. To help stop the bleeding, HCG obtained a very expensive line of credit. The deal was so expensive that it could end up wiping out a full year of earnings. In light of this, the company suspended their dividends in May.

The goal of the dividend growth strategy is to pick strong companies with a long track record of dividend increases. In terms of dividend increases, 2017 did not disappoint. There have been dividend increases throughout the year in my portfolio. I have received raises from (there may be more that didn’t make this list):

- TD Bank (TD); Scotiabank (BNS); Magna (MG); Royal Bank (RY); CIBC (CM); Bank of Montreal (BMO); National Bank (NA); TransCanada (TRP); Great-West Life (GWO); Thomson Reuters (TRI); Manulife (MFC); BCE (BCE); Telus (T); Enbridge (ENB); Enbridge Income Fund (ENF); Canadian Utilities (CU); Canadian National Railway (CNR); Canadian Pacific Railway (CP); Exco Technologies (XTC); Suncor (SU); Thompson Reuters (TRI); Leons Furniture (LNF); First National Financial (FN); Power Financial (PWF); Transcontinental (TCL.A); Imperial Oil (IMO); George Weston (WN); Loblaws (L); Sun Life (SLF); CAE (CAE); Canadian Western Bank (CWB); Fortis (FTS); Empire (EMP.A); Emera (EMA); Finning (FTT); and, Metro (MRU).

In addition to the dividend raises, I’ve continued to deploy cash into dividend stocks. What has really impacted this update is the creation of a non-registered dividend portfolio for my spouse (opened another account with MDJ reader favorite Questrade). There was some cash savings in her account that needed to be deployed, and I was able to get it invested in short order. As one of the goals of this particular account is to generate a high and reliable yield (spouse is in lower tax bracket), I am experimenting with the Dogs of the TSX strategy.

In our overall portfolio, here are the current top 10 largest holdings (besides cash):

- Enbridge (ENB);

- Bell Canada (BCE);

- Bank of Nova Scotia (BNS);

- TransCanada Corp (TRP);

- Fortis (FTS);

- Canadian Utilities (CU);

- Emera (EMA);

- CIBC (CM);

- iShares Core MSCI All Country World ex Canada Index ETF (XAW) (mostly from my wife’s RRSP);

- Royal Bank of Canada (RY).

Here is an update on the dividend totals per account. Some readers were questioning the value of “Yield on Cost”, so this update has the current yield on each portfolio. This also means that a more relevant “total invested” number is shown below. Before it was just my cost base, now it’s total portfolio value (ie. including capital gain).

December 2017 Dividend Income Update

| Account | Dividends/year | Yield |

| SM Portfolio | $6,493 | 3.47% |

| TFSA 1 | $2,539 | 4.54% |

| TFSA 2 | $2,821 | 4.72% |

| Non-Registered | $1,301 | 4.57% |

| Corporate Portfolio | $12,659 | 3.38% |

| RRSP 1 | $6,355 | 2.70% |

| RRSP 2 | $1,229 | 2.00% |

- Total Invested: $1,002,325

- Total Yield: 3.33%

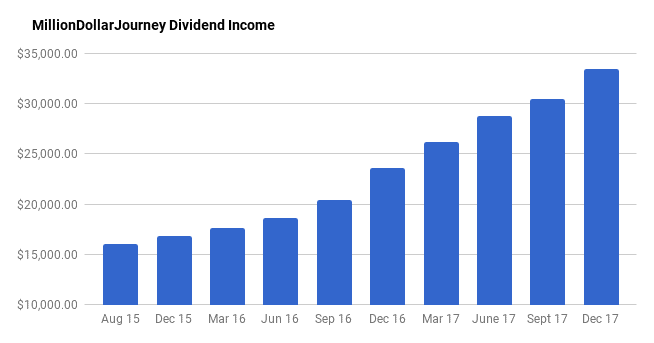

- Total Dividends: $33,397/year (+9.82%)

Through a combination of deploying cash, starting a new non-registered portfolio with savings, and collecting those juicy dividend increases, this quarter has been productive with a 9.82% bump in dividend income. I really do enjoy watching those dividends flow into the accounts.

I ended 2016 with around $23,636/year in dividends, and I’m pleased finishing 2017 with dividends of $33,397 – almost a $10k increase year over year. Although I didn’t quite meet the lofty goal of $35k this year (although there still is a bit of time left), it was pretty darn close! My plan is to keep the same pace and hit $45k in dividend income by the end of 2018.

We still have a long way to go to hit $60k, but for the most part, we are moving in the right direction in surpassing the midway point of my long-term goal. There is still cash available to deploy in most of our accounts. In particular, the lump sum of cash from the commuted values of the pensions has started to be invested but still has a significant amount left to deploy.

If you are also interested in the dividend growth strategy, here is a recent post on how to build a dividend portfolio. With this list, you’ll get a general idea of the names that I’ve been adding to my portfolios. If you want a simpler investing strategy that outperforms most mutual funds out there, check out my top ways to index a portfolio.

I hope that you also had a great financial year in 2017, and here’s to health, wealth and happiness in 2018!

Honestly just plowing it into VXC. It’s such a perfect ETF for Canadian investors. I think it might be abit too exposed to US (50%) so i’m buying exposure to euro and asia markets via ETF’s as well to boost that up. Occasionally I will buy individual stocks if I see awesome value or potential.

Hey Mike, I have the same feeling as you. It’s challenging to add a lot to US assets right now since they seem to be fully valued (or even overvalued). What is your strategy for deploying your cash?

Oh no worries :-). I’m in the sameboat actually. Are you trying to get to that balanced position over a certain amount of time – say 12 months? I was tempted to correct my imbalance all in one shot however i’d be worried of buying into overpriced US markets while selling underpriced Canada. I think Europe and Asia are fairly or slightly underpriced. Oh well in both our cases we have about the same amount of dividends rolling into console us. My yield on capital is around 3.05% but that includes 35% allocation to cash, bonds and prefs.

Your top ten tells me you are way too heavy on Canadian equities. They have severley under-performed a more globally diversified portfolio and you likely have lost 100-200K in total returns. Those interest rate sensitive holdings will get murdered this year.

Thanks for the upbeat report Mike! :) My RRSP is almost 100% outside Canada, RESPs 75% outside Canada, Wife’s RRSP 100% outside Canada. But you are right, despite this, my largest account (corporate account) is invested in Canadian dividend stocks, which overweights Canada. Right now, we are about 35% outside Canada. Working on getting this number up to at least 50%.

Been a silent reader of your blog for a couple years now. It’s very useful, informative and intriguing! I’m a few years older than you, 41, but we have very similar situations. Gov’t worker…avid investor…have wife and kids. I’m very interested in your Smith Manouevre technique. I have a few questions I was hoping you could answer (if you know the answers that is!)

My background:

– I’m the main income earner in the family.

– Our mortgage is completely paid off (due to a successful sale of a business a few years ago)

– We have available a $440,000 mortgage line of credit (or heloc)

What I’m wondering:

– Can I still use the S.M. if we are mortgage free? I would open an unregistered account, borrow say $150,000 initially to get my feet wet….could the interest I pay against that heloc loan be written off, even if I have no active mortgage?

– My wife and I co-own our home. Could I open an unregistered investment account in her name, borrow the 150k against the home, have her “trade/invest” it, and she could claim the income and write off the interest charges…is that ok?

– Does the full amount of the heloc have to be invested at any given time, or can the investment account hold cash?

– Are there special forms at tax time to fill out to indicate you have borrowed against your home to invest so that you can write off said interest charges on the heloc?

Really appreciate your time on this! I’d love to get this started for my wife (if it’s allowed) as she currently earns zero income…I don’t see why it shouldn’t be considering both our names are on the home title (I’m more wondering if I might have to split the tax burden with her considering we both own the home, or if she can claim it all if the investment account is in her name).

Cheers,

Dave.

HI Dave, SM is simply borrowing against real estate to invest in the stock market. So yes, you could borrow against your house, invest in the market and your interest would be tax deductible. About the trading account, although tax-wise it would be ideal to have it under her name, but I think CRA would look at where the funds came from. IF you both own the house, it may be best to both be on the account. While you will both pay tax on the trading profits/dividends, you will also split the tax deduction. With regards to cash in your account, only withdraw as much from your HELOC as you wish to invest. So if it’s $2k/month then only withdraw that much at a time. In terms of income tax, line 221 is where you put your interest expenses.

Just found your site … very cool … we have similar journeys but different paths to the same end goal. I like the idea of index funds namely Vanguard S and P 500 … however I am invested in overseas real estate and the local overseas stock market …. seeing my non resident status … I also will receive no government or provincial / state pension seeing I have worked overseas too long etc etc …. but I have still reached FI on my own initiative of overseas investments … :) My context is from the far side of the planet however … :) Michael CPO

Thanks for stopping by Michael. Great thing about index investing is that no matter where we are globally, we’ll likely have a similar indexed portfolio.

This is really a good year as your chart is progressive all through. I totally support your plan or the need to generate passive income. That is what makes retirement age to be sweet and not just the money stacked in savings account.

First of Thanks for sharing your journey with us.

Can you please point me to

1. Your current holdings

2. Your suggestions to anyone starting 2018 with lets say $25000

Merry X Mas

Hey Louking,

In terms of holdings, my top holdings are in this post. If you are looking at starting a portfolio with $25k, I would look at index ETFs. Here’s a post on various ways to index:

https://milliondollarjourney.com/top-6-indexing-options-for-your-portfolio.htm

Wow, I am amazed how you continue to strive further after having accomplished your net worth goal. Kaizen approach at its best!

On another note, your dividend increase graph at the moment, seems like my Net Worth graph, lol. Hope to see the other side some day (its a long journey, but one that I will make).

Thanks!

PAI

Thanks for the kind feedback. Here’s to Health, Wealth and Happiness in the New Year!

Congratulations on your investment success. Keep it up.

I see you have investments in your RRSP, TFSA and Non Registered accounts. What order would you recommend investing in these? I am debating whether or not I should focus on investing in my RRSP or TFSA. I am 53 yrs old and plan on retiring in the next 10 years and plan on living off approx. 70% of my current income. Logically I would continue to invest in RRSP since I will be in a lower tax bracket when I withdraw funds but concerned about OAS clawback.

Hi Nick,

Your personal situation would depend on a variety of factors. If you have a large defined benefit pension when you retire in 10 years, I would max out the TFSA first then contribute excess savings into RRSP. This article may help:

https://milliondollarjourney.com/portfolio-allocation-rrsps-tfsas-and-taxable-accounts.htm

Thanks for the Link. It reinforces what I already thought.

I don’t have a defined benefit pension. My plan is to continue to contribute to my RRSP since I am in a higher tax bracket now than when I plan on retiring. Any tax refunds/found money will go into my TFSA.

Cheers

Sounds like you have it figured out Nick! All the best and Happy New Year!